⚠️ Disclaimer: This article is for educational purposes only and does not constitute legal, tax, or financial advice. Tax laws change annually. Always consult a qualified CPA, Enrolled Agent, or cross-border tax attorney before filing. Verify all current thresholds at IRS.gov.

🔍 About This Guide: Written by the MoneyAbroadGuide editorial team and reviewed for accuracy as of June 2026. Sources include IRS Publication 54, FinCEN official guidance, U.S. Treasury FATCA rules, and the Internal Revenue Code.

Approximately 9 million US citizens live outside the United States — and fewer than one-third fully understand what they owe the IRS every year. That is not a failure of effort. It is a failure of information.

The United States operates on citizenship-based taxation — one of only two countries in the world to do this, alongside Eritrea. Unlike nearly every other nation, the US taxes its citizens on worldwide income regardless of where they live, where they work, or what taxes they already pay to a foreign government. A teacher in Seoul, a retiree in Lisbon, a freelance designer in Bangkok, and an oil engineer in Dubai all share the same IRS filing obligation as someone who has never left Ohio.

The good news is real: with the right strategy, most American expats owe zero US federal income tax after properly applying the Foreign Earned Income Exclusion, Foreign Tax Credits, and applicable treaty provisions. The system is designed to prevent double taxation — but only for those who understand how to use it.

The risk is also real: penalties for non-compliance are among the harshest in US tax law. A single missed FBAR filing can trigger a $10,000 penalty. Willful violations can cost 50% of your account balance per year. The IRS uses FATCA data shared by thousands of foreign banks to identify non-filers.

This guide gives you the complete picture — what you must file, what you can exclude, which strategy saves more, and how to avoid the mistakes that cost Americans abroad thousands of dollars every year.

✅ Quick Answer: Your 2026 US Expat Tax Obligations at a Glance

- US citizens and green card holders must file Form 1040 annually — regardless of residence or local taxes paid.

- FEIE (Form 2555): Exclude up to $126,500 (2024) / ~$130,000 (2025) of foreign earned income.

- FTC (Form 1116): Dollar-for-dollar credit for foreign income taxes paid — no income cap.

- FBAR (FinCEN Form 114): Required if foreign accounts exceeded $10,000 aggregate at any point during the year.

- FATCA (Form 8938): Required for expats with $200,000+ in foreign assets at year-end ($300,000 at any point).

- Filing deadline: June 15 automatic extension; October 15 with Form 4868.

- Most expats owe $0 in US taxes with proper planning.

Key Takeaways

- The US is one of two countries that taxes based on citizenship, not residency. Filing is mandatory regardless of where you live.

- The FEIE (Form 2555) and FTC (Form 1116) are your two primary tools. Choosing the wrong one can cost thousands annually.

- FBAR and FATCA are separate from your tax return, have separate deadlines, and carry separate — often more severe — penalties.

- State taxes do not automatically end when you move abroad. Formal domicile severance is required for high-risk states like California, Virginia, and New York.

- The IRS Streamlined Foreign Offshore Procedures offer penalty-free catch-up for non-willful non-filers.

- Self-employment income carries 15.3% SE tax even when fully excluded under the FEIE — the most common expensive surprise for freelancers abroad.

Table of Contents

- Who Must File US Taxes While Living Abroad?

- US Expat Tax Rules Explained

- Foreign Earned Income Exclusion (FEIE)

- Foreign Tax Credit (FTC)

- FEIE vs FTC: Which Strategy Saves More?

- FBAR Requirements

- FATCA Requirements

- State Taxes for Expats

- Tax Deadlines for Americans Abroad

- Common Tax Mistakes to Avoid

- Step-by-Step Filing Process

- Real Case Studies

- Tax Software vs CPA: What Should You Use?

- Frequently Asked Questions

- Final Thoughts

1. Who Must File US Taxes While Living Abroad?

The IRS filing obligation is based on citizenship and residency status, not on where you earn your income or where you pay taxes locally. Under IRC § 61 and the principle of citizenship-based taxation upheld since the Revenue Act of 1913, all US citizens and lawful permanent residents must report worldwide income annually.

Filing Requirement Table by Status (2024)

| Taxpayer Category | Must File? | Form Used | Worldwide Income? | FEIE Available? |

|---|---|---|---|---|

| US Citizen living abroad | ✅ Yes | Form 1040 | Yes | Yes |

| Green Card Holder abroad | ✅ Yes (until I-407) | Form 1040 | Yes | Yes |

| H-1B (Substantial Presence met) | ✅ Yes | Form 1040 | Yes | Yes (if tax home abroad) |

| F-1 Student (years 1–5) | ✅ Yes (limited) | Form 1040-NR + Form 8843 | US-source only | No |

| F-1 Student (year 6+) | ✅ Yes | Form 1040 | Yes | Yes |

| J-1 Exchange Visitor (years 1–2) | ✅ Yes (limited) | Form 1040-NR + Form 8843 | US-source only | No |

| ITIN Holder with US rental income | ✅ Yes | Form 1040-NR | US-source only | No |

Income thresholds for 2024: Single: $13,850 | Married Filing Jointly: $27,700 | Head of Household: $20,800 | Married Filing Separately: $5 (if spouse is US citizen or resident).

Green card holders: You remain a US tax resident until you formally abandon your green card via Form I-407. Living abroad for years does not terminate this obligation. USCIS and IRS requirements can conflict: maintaining a green card requires demonstrating intent to return to the US, while qualifying for the FEIE requires establishing genuine foreign residency. Work with both an immigration attorney and a tax professional if you face this tension.

The Substantial Presence Test (for H-1B and non-immigrant visa holders): You are a US tax resident if you were physically present in the US for at least 31 days in the current year AND at least 183 days over three years, counting: all days this year + ⅓ of days last year + ⅙ of days two years ago.

2. US Expat Tax Rules: The Three Compliance Layers

US expat tax compliance is not one obligation — it is three distinct layers. Understanding each layer prevents the costly omissions that generate most expat tax penalties.

Layer 1 — Federal Income Tax Return (Form 1040). Your annual tax return, due April 15 (automatically extended to June 15 for expats; further to October 15 with Form 4868). You report worldwide income here and claim your exclusions and credits. The IRS requires all foreign amounts converted to US dollars using the IRS annual average exchange rate for recurring income items, or the spot rate on the transaction date for specific events.

Layer 2 — International Information Returns. Separate forms with separate deadlines and separate penalties. These include the FBAR (FinCEN Form 114), Form 8938 (FATCA), Form 5471 (foreign corporation ownership), Form 8865 (foreign partnership), Form 3520/3520-A (foreign trusts and gifts over $100,000), and Form 8621 (Passive Foreign Investment Companies). Penalties for missing these forms are often $10,000 per form per year — completely independent of whether you owe any tax.

Layer 3 — State Income Tax Returns. Depending on your former US state of domicile, you may continue to owe state income taxes even while living abroad. Nine states have no income tax: Alaska, Florida, Nevada, South Dakota, Texas, Washington, Wyoming, plus New Hampshire and Tennessee (investment income only). States like California, New York, Virginia, and South Carolina aggressively pursue former residents living abroad.

3. Foreign Earned Income Exclusion (FEIE)

The FEIE, governed by IRC § 911 and claimed on Form 2555, allows qualifying US expats to exclude a set dollar amount of foreign earned income from US gross income — meaning it is never subject to US income tax.

- 2024 FEIE Limit: $126,500

- 2025 FEIE Limit: $130,000 (indexed annually for inflation per IRC § 911(b)(2)(D))

What qualifies as “foreign earned income”: Wages, salaries, professional fees, self-employment income, and tips — for services physically performed in a foreign country.

What does NOT qualify: Dividends, interest, capital gains, rental income, pension distributions, Social Security benefits, IRA distributions, alimony, and unemployment compensation. None of these are “earned” under the FEIE definition.

Two Qualification Pathways

Physical Presence Test: Be physically present in one or more foreign countries for at least 330 full days during any consecutive 12-month period. A “full day” is midnight to midnight in a foreign country. Any day you set foot on US soil does not count. This test is purely mechanical and objective.

Bona Fide Residence Test: Be a bona fide resident of a foreign country for an uninterrupted period that includes at least one full calendar year (January 1 – December 31). The IRS evaluates the nature of your stay, your intent to remain, the permanence of your housing, your ties to the foreign community, and whether you filed as a resident in that country. This test is subjective and can be challenged; workers on fixed-term contracts with clear return dates often fail it.

Foreign Housing Exclusion

Expats who qualify for the FEIE may also exclude reasonable foreign housing costs above a base amount of $19,200 (16% of the FEIE maximum for 2024). IRS Notice 2024-77 sets country-specific maximum exclusion amounts. Examples: London $38,600 | Paris $33,700 | Tokyo $47,200 | Singapore $69,200 | Hong Kong $114,300 | Abu Dhabi $68,400 | Dubai $53,800. Only employees may use the exclusion form. Self-employed qualifying expats claim the Foreign Housing Deduction instead (same calculation, different tax impact).

4. Foreign Tax Credit (FTC)

The FTC, claimed on Form 1116, provides a dollar-for-dollar credit against your US income tax liability for qualifying income taxes paid or accrued to foreign governments. Unlike the FEIE, the FTC has no income ceiling and applies to all income types — earned and unearned.

How it works: If you paid $30,000 in UK income taxes on salary and investment income, and your US tax on the same income would have been $25,000, your FTC eliminates your entire US tax liability. The unused $5,000 excess credit carries back one year or forward ten years.

The limitation rule (IRC § 904): The FTC cannot exceed the US tax that would apply to your foreign-source income. The formula: FTC Limit = (Foreign Source Income ÷ Total Income) × US Tax Before Credits.

Separate income baskets: Form 1116 requires separate calculations for general category income (wages, business income), passive category income (dividends, interest, capital gains), foreign branch income, and certain other categories. Excess credits in one basket cannot offset tax in another — they carry within their own basket only.

Qualifying vs. non-qualifying foreign taxes: Only compulsory payments under a foreign law imposed on income qualify. VAT, customs duties, property taxes, wealth taxes, inheritance taxes, and most social contribution levies do not qualify under Treasury Regulations § 1.901-2.

Totalization Agreements: The US has social security totalization agreements with 30 countries including the UK, Germany, France, Canada, Australia, Japan, and South Korea. These prevent double social security taxation. Under the relevant agreement, you pay into only one country’s social security system — the country where you work. Obtain a Certificate of Coverage from your foreign employer or social authority to document this.

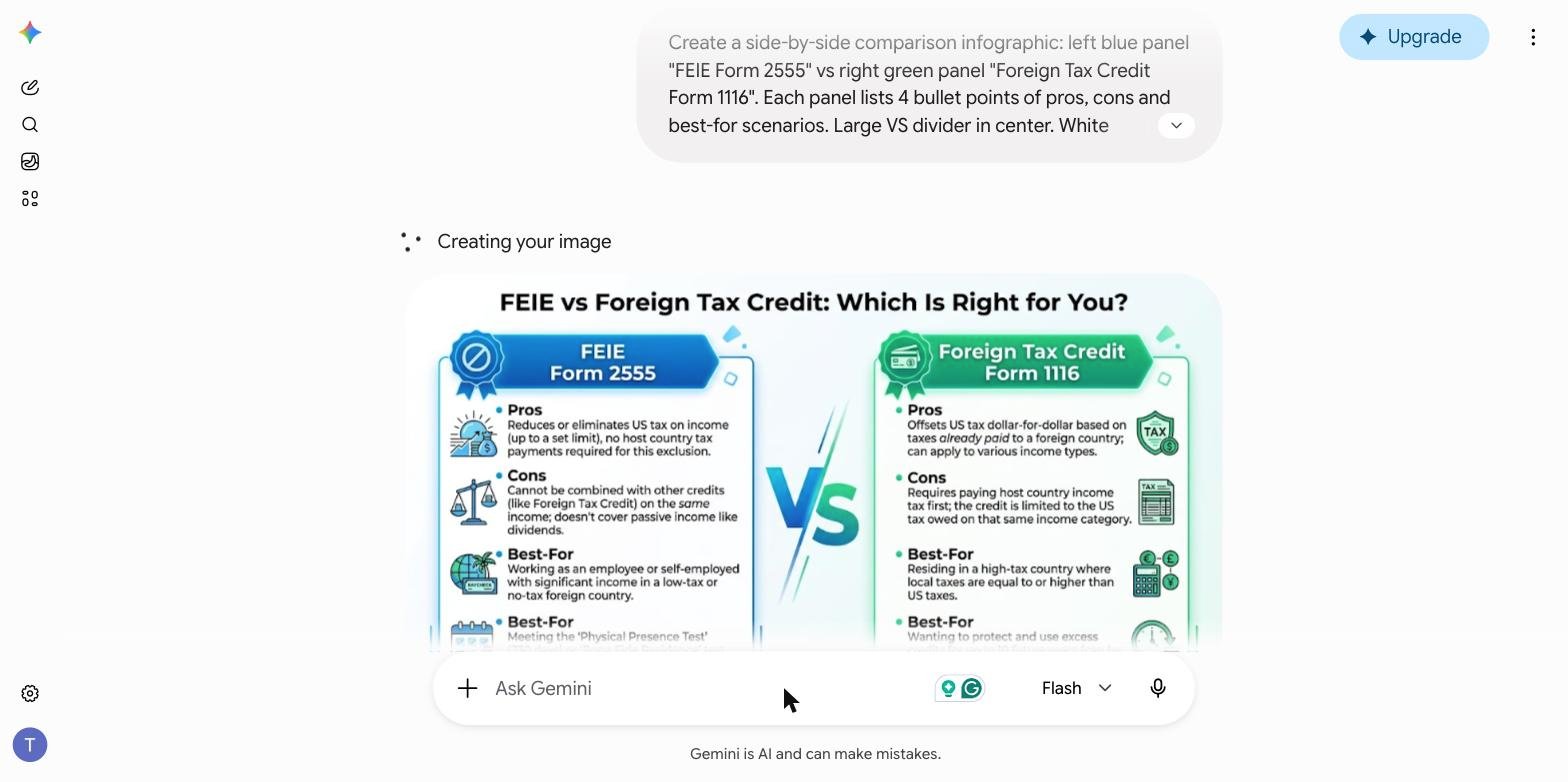

5. FEIE vs FTC: Which Strategy Saves More?

Choosing between the FEIE and FTC is the single most consequential tax decision most expats make. The wrong choice can cost thousands of dollars annually. The right choice depends on your income level, your country’s tax rate, and the nature of your income.

FEIE vs FTC Comparison Table

| Factor | FEIE (Form 2555) | FTC (Form 1116) |

|---|---|---|

| Income covered | Foreign earned income only | All income types (earned + passive) |

| Annual cap | $126,500 (2024) | No cap — limited to US tax on foreign income |

| Best for | Low-tax countries (UAE, Singapore, Thailand, Bahrain) | High-tax countries (France 45%, Germany 45%, UK 45%, Denmark 56%) |

| Self-employment tax | Does NOT eliminate SE tax (15.3%) | Does NOT eliminate SE tax |

| Carryover | No carryover | 10-year carry forward, 1-year carry back |

| Social Security credits | Excluded income does NOT earn SS work credits | Income remains in SS wage base |

| Election revocation | 5-year bar on re-election without IRS consent | No waiting period |

| Passive income coverage | Does NOT cover dividends/interest/capital gains | Covers all foreign-source income |

| Complexity | Moderate (Form 2555) | Higher (Form 1116, separate baskets) |

Pros and Cons Summary Table

| Strategy | Pros | Cons |

|---|---|---|

| FEIE only | Simple; fully excludes up to $126,500; no complex calculations | Cannot use FTC on same income; wastes high foreign taxes; no SS credits; does not cover passive income |

| FTC only | Covers all income types; no cap; protects SS credits; 10-year carryforward | Complex calculations; less effective in low-tax countries; separate income baskets required |

| FEIE + FTC (dual) | Maximizes benefit in many situations; FEIE covers earned income, FTC covers passive and excess earned income | Requires careful coordination; software often handles incorrectly; professional guidance strongly recommended |

Rule of thumb: If you are in a country where local income tax rates are lower than comparable US rates at your income level, the FEIE typically produces a better outcome. If you pay more in foreign taxes than you would in US taxes, the FTC often eliminates your US liability entirely and generates carryforward credits. For incomes between $100,000–$180,000, the crossover point varies — model both scenarios or consult a specialist.

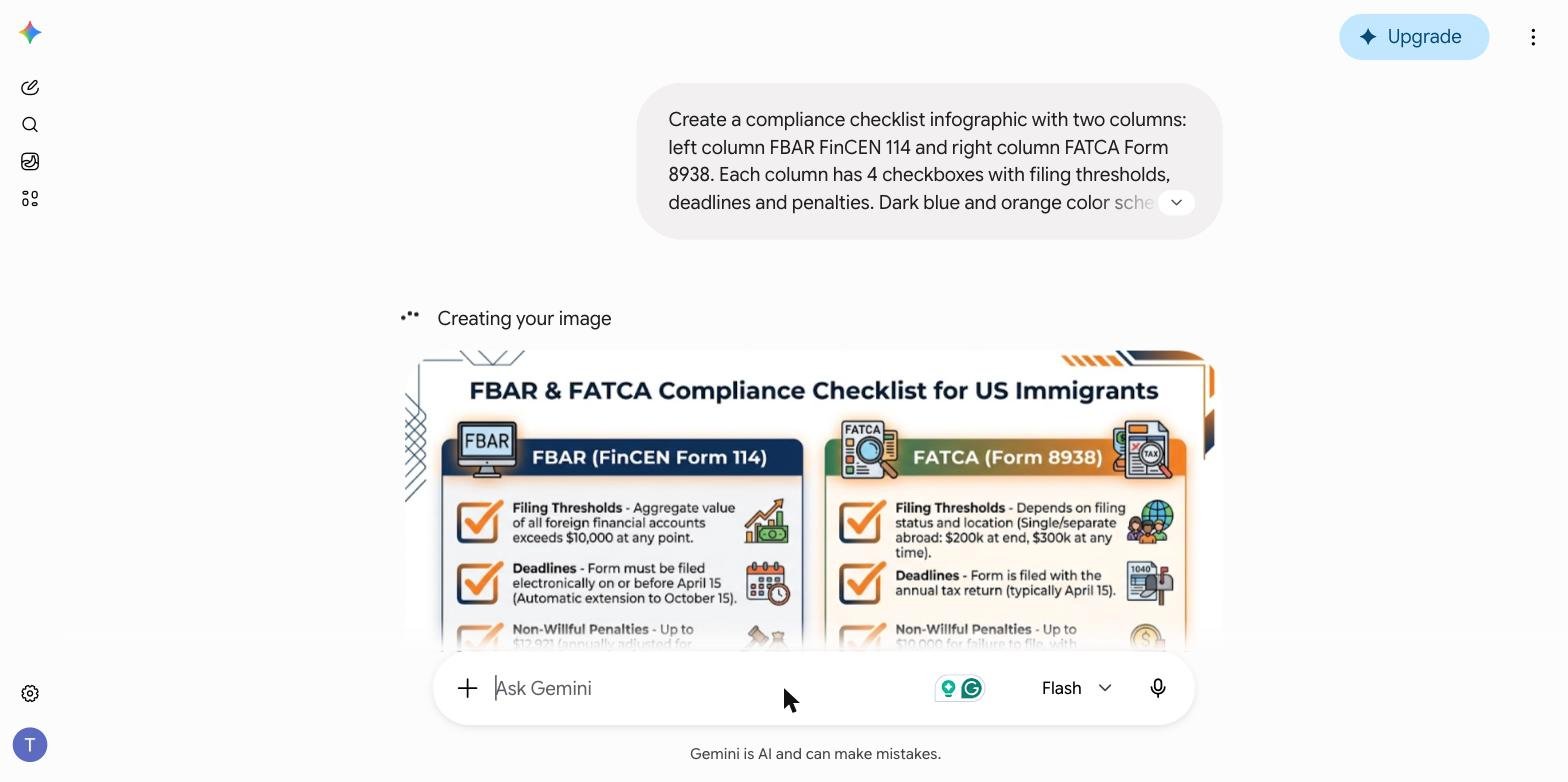

6. FBAR Requirements

The Foreign Bank Account Report (FBAR), formally FinCEN Form 114, is required of any US person who had a financial interest in, or signature authority over, foreign financial accounts whose aggregate maximum value exceeded $10,000 at any point during the calendar year. This is governed by the Bank Secrecy Act (31 USC § 5314) and administered by FinCEN — NOT the IRS.

The $10,000 threshold applies to the aggregate of all foreign accounts combined, not each account individually. Three accounts with maximums of $4,000 + $5,000 + $2,500 = $11,500 aggregate → FBAR required.

FBAR Threshold and Coverage Table

| Account Type | Included in FBAR? |

|---|---|

| Foreign checking / savings accounts | ✅ Yes |

| Foreign brokerage / investment accounts | ✅ Yes |

| Foreign mutual funds | ✅ Yes |

| Foreign pension plans (if classified as financial account) | ✅ Yes (case-by-case) |

| Foreign life insurance with cash value | ✅ Yes |

| Accounts with signature authority only (even if not owner) | ✅ Yes (exceptions for employer accounts) |

| Foreign real estate held directly (no account) | ❌ No |

| US accounts held at foreign branches of US banks | ❌ No |

FBAR Penalty Table

| Violation Type | Maximum Penalty Per Violation Per Year | Notes |

|---|---|---|

| Non-willful failure to file | Up to $10,000 | Reasonable cause exception available |

| Willful failure to file | Greater of $100,000 or 50% of account balance | Per account, per year — catastrophic potential |

| Criminal willful violation | Up to $250,000 and/or 5 years imprisonment | Requires DOJ referral; rare but real |

Source: 31 USC § 5321; FinCEN penalty guidance.

Filing deadline: October 15 (automatic — no extension request needed). Filed exclusively through the BSA E-Filing System at bsaefiling.fincen.treas.gov — NOT with the IRS or attached to Form 1040.

Streamlined relief: The Streamlined Foreign Offshore Procedures allow eligible expats to file six years of delinquent FBARs without penalties if non-compliance was non-willful. Eligibility requires residing outside the US for at least one of the three prior years and certifying non-willful conduct on Form 14653.

7. FATCA Requirements

The Foreign Account Tax Compliance Act (FATCA), enacted under the HIRE Act of 2010, requires US taxpayers to file Form 8938 (Statement of Specified Foreign Financial Assets) with their annual Form 1040. FATCA also requires thousands of foreign financial institutions to report US account holders directly to the IRS — meaning the IRS often already has your account data before you file.

FATCA Threshold Table (Expats Living Abroad)

| Filing Status | Year-End Value Threshold | At-Any-Time-During-Year Threshold |

|---|---|---|

| Single / Married Filing Separately (living abroad) | $200,000 | $300,000 |

| Married Filing Jointly (living abroad) | $400,000 | $600,000 |

Note: Domestic (US-resident) filers have lower thresholds: $50,000/$75,000 single; $100,000/$150,000 MFJ. Source: IRS FATCA guidance.

What Form 8938 covers beyond FBAR: Foreign stocks, foreign bonds, interests in foreign partnerships, beneficial interests in foreign trusts, foreign insurance contracts with cash value, and foreign hedge funds. It is common to owe both FBAR and Form 8938 for the same underlying accounts.

Penalties for Form 8938 non-compliance: A $10,000 penalty for failure to disclose, increasing by $10,000 per month after IRS notification (maximum $60,000 per form per year). Additionally, the statute of limitations on your entire tax return remains open indefinitely if Form 8938 was required but not filed — per IRC § 6501(e)(1).

8. State Taxes for Expats

Moving abroad does not automatically terminate your US state tax residency. States tax based on domicile — your permanent home, the place you intend to return to. Several states are significantly more aggressive than others.

High-risk states for expats: California’s Franchise Tax Board presumes California domicile continues until you prove otherwise. The FTB applies a “closest connections” analysis examining where your spouse/dependents live, where your principal business is conducted, where you maintain professional and social ties, and where your real property is. New York’s 548-day rule, Virginia’s domicile maintenance standards, and South Carolina’s residency definitions similarly catch unwary expats.

Documenting domicile severance: Sell or formally lease your property, obtain a driver’s license in another state or foreign country, register vehicles elsewhere, close local bank accounts (or transfer them), update voter registration, resign from local clubs and professional associations, and file a final part-year resident return for the year of departure.

Income that remains state-taxable regardless of residence: Rental income from property located in the state, S-corporation or partnership income from entities operating in the state, and wages earned while physically working in the state during visits home.

9. Tax Deadlines for Americans Abroad

Filing Deadline Table

| Deadline | What It Covers | How to Qualify / Action Needed |

|---|---|---|

| April 15 | Standard federal return due date; Q1 estimated taxes | Automatic; pay estimated taxes here to stop interest |

| June 15 | Automatic 2-month extension for expats; Q2 estimated taxes | Must be living/working outside US on April 15 — attach brief statement |

| September 15 | Q3 estimated taxes (self-employed) | Form 1040-ES; IRS Direct Pay |

| October 15 | Further extension for tax return; FBAR automatic deadline | File Form 4868 by June 15; FBAR auto-extended — no request needed |

| January 15 (next year) | Q4 estimated taxes (self-employed) | Form 1040-ES |

Passport revocation: Under the FAST Act, the IRS may request State Department passport revocation or denial for taxpayers with “seriously delinquent tax debt” exceeding $62,000 in 2024 (adjusted annually for inflation). This threshold includes penalties and interest. Expats at risk should immediately establish an IRS installment agreement or submit an Offer in Compromise.

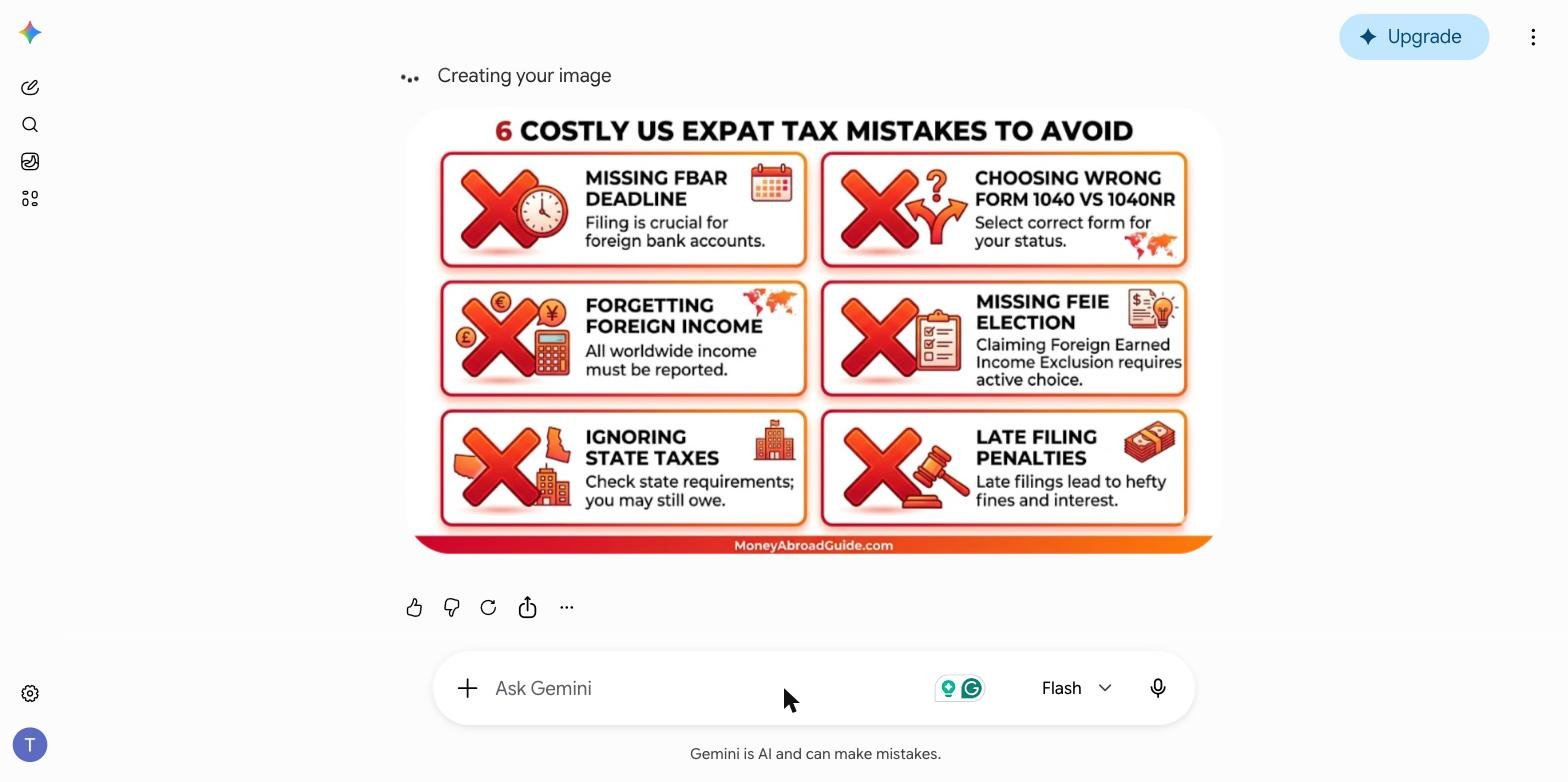

10. Common Tax Mistakes to Avoid

Top Expat Tax Mistakes and How to Avoid Them

| Mistake | Consequence | Prevention |

|---|---|---|

| Not filing because you paid foreign taxes | Failure-to-file penalty (5%/month, max 25%) + FBAR penalties stack separately | File every year regardless of local taxes paid |

| Missing FBAR deadline | $10,000 per violation (non-willful); up to 50% of account balance (willful) | Calendar reminder for October 15; file at bsaefiling.fincen.treas.gov |

| Using FEIE and FTC on the same income | IRS disallows the duplicate benefit; 20% accuracy-related penalty | Apply FEIE to earned income; FTC to remaining and passive income only |

| Claiming FEIE without meeting the qualifying test | Full exclusion disallowed; back taxes + interest | Track every travel day; document foreign residence thoroughly |

| Ignoring SE tax on FEIE-excluded income | Unexpected SE tax bill + underpayment penalties | FEIE excludes income tax, not SE tax. Budget for 15.3% SECA; make quarterly payments |

| Not severing state domicile before departing | Years of state back taxes + interest | Document domicile change formally; file part-year return |

| Holding foreign mutual funds without PFIC election | Punitive excess distribution regime; effective rate can exceed 50% | Avoid non-US mutual funds; use US-domiciled ETFs or elect QEF on Form 8621 |

| Revoking FEIE election without planning | 5-year bar on re-election without IRS consent | Model multi-year projections before making or revoking the election |

| Waiting for IRS contact before catching up | Streamlined Procedures unavailable once IRS initiates contact | Use Streamlined Procedures proactively — available only before IRS contact |

⚠️ The Most Expensive Expat Tax Mistake

The costliest error is not the missed deadline alone — it is the cascade. A missed FBAR generates a $10,000 penalty. The same missed Form 8938 generates another $10,000. The IRS then discovers the unfiled Form 1040 and adds failure-to-file penalties. Three unfiled years with multiple accounts can produce six-figure penalty exposure — on income that, if properly filed, would have generated zero US tax owed. The cost is never the tax. The cost is always the penalties.

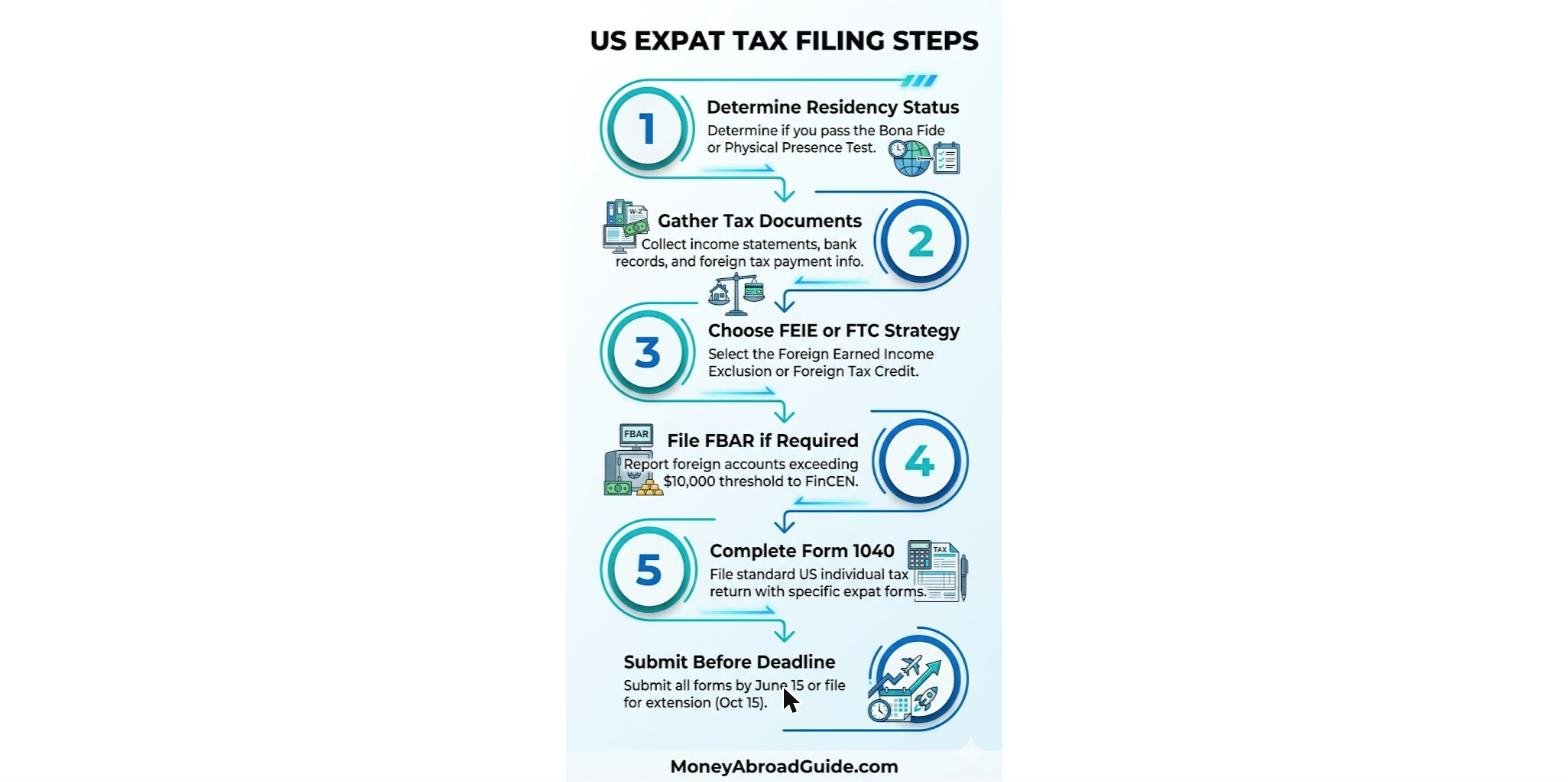

11. Step-by-Step Filing Process

Expat Tax Filing Checklist

| Step | Action | Forms / Resources |

|---|---|---|

| 1 | Determine filing status and income threshold | IRS Pub 519; IRS Interactive Tax Assistant |

| 2 | Gather all income documentation (domestic + foreign) | W-2, 1099, foreign payslips, foreign tax certificates |

| 3 | Identify all foreign financial accounts and maximum balances | Bank statements (all months); year-end statements |

| 4 | Calculate qualifying days abroad (Physical Presence Test) | Passport stamps; travel records; calendar log |

| 5 | Model FEIE vs FTC to determine optimal strategy | Specialized expat tax software or CPA consultation |

| 6 | Complete Form 1040 with applicable schedules | Schedules 1, 2, 3 as needed; Schedule C if self-employed |

| 7 | Attach Form 2555 (FEIE) or Form 1116 (FTC) | Based on strategy chosen in Step 5 |

| 8 | File FBAR if aggregate accounts exceeded $10,000 | FinCEN Form 114 at bsaefiling.fincen.treas.gov by October 15 |

| 9 | Determine Form 8938 obligation | Attach to Form 1040 if assets exceed $200,000/$400,000 |

| 10 | File additional information returns if applicable | Forms 5471, 8865, 3520, 8621 depending on situation |

| 11 | File state return if maintaining state domicile | State-specific forms; verify nexus first |

| 12 | Make estimated tax payments if self-employed | Form 1040-ES; IRS Direct Pay (free) |

| 13 | Retain all records for minimum 7 years | Encrypted cloud storage + physical backup |

12. Real Case Studies: US Expats in 2026

Case Study 1 — American Teacher in Spain

Profile: Emma Rodriguez, 34, high school English teacher in Seville. Single. Annual salary: €48,000 ($51,840 at 2024 average EUR/USD rate of 1.08). Spanish income taxes paid: €7,200 ($7,776). Spanish bank account: peak balance €18,500 ($19,980). No US income. No other foreign accounts.

Challenge: Emma moved to Spain in September 2022 and did not file US taxes for 2022 or 2023, believing her Spanish taxes covered her obligations. In early 2025, she learned she was non-compliant through an expat community forum. She feared large penalties and back taxes owed.

Solution: Emma qualified for the Streamlined Foreign Offshore Procedures — she had genuinely not known about the requirement and had resided outside the US continuously. She engaged a specialized expat tax firm ($695 for a three-year catch-up package) which: (1) Filed 2022 (partial-year FEIE of $38,260 prorated for 4 months), 2023 (full FEIE of $120,000), and 2024 (full FEIE of $126,500). In all three years, her income fell entirely within the FEIE cap. (2) Filed six years of FBARs. Years 2019–2021 had no FBAR obligation (she was in the US). Years 2022–2024 each required disclosure of her €18,500 peak balance. (3) Submitted Form 14653 certifying non-willful conduct, explaining she had relied on a Spanish colleague’s incorrect advice.

Result: Federal taxes owed across all three years: $0. FBAR penalties: $0 (waived under Streamlined Procedures). Professional preparation cost: $695. Potential penalties avoided: $30,000+ (three years × $10,000 FBAR minimum).

Lesson: Non-willful non-filers who act before IRS contact can use the Streamlined Procedures to achieve a clean slate at zero penalty cost. Every month of additional delay increases risk without reducing the compliance burden.

Case Study 2 — American Engineer in UAE

Profile: Michael Okafor, 43, petroleum engineer in Abu Dhabi. Married, two children. Annual compensation: salary $185,000 + employer housing allowance $42,000 = $227,000 total. UAE income tax: $0 (UAE has no personal income tax). Peak foreign account balance: $148,000.

Challenge: Michael’s income significantly exceeded the FEIE cap of $126,500. With zero foreign taxes available for the FTC, his initial exposure was approximately $44,000 in US federal income tax. His first tax preparer — a general US CPA without expat specialization — proposed he simply pay the full amount.

Solution: A specialized expat CPA restructured his position using the authorized dual-exclusion strategy under IRC § 911:

Step 1: FEIE of $126,500 (Form 2555).

Step 2: Foreign Housing Exclusion per IRS Notice 2024-77. Abu Dhabi housing cap: $68,400. Michael’s qualifying housing costs: $42,000. Housing exclusion: $42,000 − $19,200 (base amount) = $22,800.

Step 3: Total excluded: $149,300. Taxable income: $227,000 − $149,300 = $77,700. Less standard deduction ($29,200 MFJ) = $48,500. Child Tax Credit ($4,000 for two children).

Step 4: Final US tax liability: approximately $3,040.

Result: Reduced annual US tax from ~$44,000 to $3,040. Annual savings: $40,960. CPA fee: $1,200. Net annual benefit from expert planning: $39,760.

Lesson: In zero-tax jurisdictions, the Foreign Housing Exclusion is not optional — it is essential. Every qualifying housing dollar above the $19,200 base eliminates an equivalent dollar from US taxable income. High earners in the UAE, Bahrain, Qatar, and Kuwait should never file without maximizing this layered strategy.

Case Study 3 — American Freelancer in Thailand

Profile: Jasmine Park, 27, freelance UX designer working remotely from Chiang Mai. Single. Annual income: $74,000 (100% from US-based clients, paid in USD to a US bank account). Thai income tax: $0 (below Thai personal threshold after deductions). Thai bank account: peak balance ฿280,000 ($7,840). Qualified for Physical Presence Test: 341 days in Thailand.

Challenge: Jasmine assumed the FEIE would eliminate all her US tax, resulting in zero owed. Her first-year DIY filing omitted Schedule SE. She received an IRS bill 18 months later for $10,451 in self-employment tax plus $840 in underpayment penalties.

Tax reality:

FEIE exclusion: $74,000 (full amount, below cap) — income tax: $0.

Self-employment tax (SECA): 15.3% × ($74,000 × 92.35%) = $10,451. Thailand has no totalization agreement with the US, so no SE tax exemption is available.

FBAR: Not required (Thai account peak of $7,840 is below the $10,000 threshold).

Result after correction: US federal income tax: $0. SE tax owed: $10,451. Jasmine now makes quarterly estimated payments of approximately $2,613 (due April 15, June 15, September 15, January 15) to avoid underpayment penalties. Annual filing cost: $249 (specialized expat software).

Lesson: Self-employment tax is the most common and expensive surprise for freelancers and digital nomads using the FEIE. The exclusion covers income tax completely — but SECA tax applies to every dollar of net self-employment income regardless. Budget for it explicitly from Day One abroad.

Case Study 4 — American Retiree in Portugal

Profile: Robert and Linda Martinez, both 68, retired to Lisbon, Portugal in 2022. Income: Robert’s Social Security $54,000/year + 401(k) distributions $48,000/year + Linda’s pension $22,000/year = $124,000 combined. Portugal’s NHR regime exempts foreign pension income from Portuguese taxation for 10 years. Portuguese income tax paid on local investment income only: €2,100 ($2,268).

Challenge: Robert and Linda believed Portugal’s NHR exemption also eliminated their US tax obligations. In fact, none of their income qualifies for the FEIE (it is entirely passive — Social Security, pensions, and 401(k) distributions). The NHR regime affects their Portuguese tax, not their US tax.

Key calculations:

Social Security: Up to 85% of benefits are included in US gross income at their combined income level of $124,000. Taxable SS: $45,900.

401(k) distributions: Fully taxable as ordinary income ($48,000).

Pension: Fully taxable ($22,000).

Total taxable income: $115,900. Less standard deduction for MFJ over 65 ($30,700 for 2024): $85,200.

US income tax: approximately $12,800. Less FTC for Portuguese investment income taxes ($2,268).

Final tax owed: approximately $10,532.

FBAR: Required — Portuguese Millennium BCP account peak balance €38,000 ($41,040).

Result: US federal tax: $10,532. No FEIE available (all income is passive). FTC partially offsets. Professional preparation: $775. State tax: $0 (established Florida domicile before departing).

Lesson: Retirement abroad does not reduce US tax obligations. Retirees with primarily passive income cannot use the FEIE and have limited FTC offset if living in a low-tax country. Strategic 401(k) drawdown timing and Roth conversion planning before departing the US are the most powerful tools available — not expat exclusions applied after the fact.

13. Tax Software vs CPA: What Should You Use?

The decision between DIY tax software and a specialized CPA depends on income level, financial complexity, country of residence, and risk tolerance. Neither is universally superior — the optimal choice is proportional to your complexity.

CPA vs DIY Software Comparison Table

| Factor | DIY Expat Software | Expat-Specialized CPA |

|---|---|---|

| Best for income level | Under $90,000 with simple situation | $90,000+ or any complex situation |

| Typical annual cost | $149 – $399 | $395 – $2,500+ |

| Handles FEIE / FTC optimization | Yes (basic modeling) | Yes, with multi-year projection |

| Handles FBAR / Form 8938 | Yes (most expat software) | Yes, included in most packages |

| Handles Form 5471 (foreign corporation) | Limited or no | Yes (specialty fee $500–$1,500) |

| Handles PFIC (Form 8621) | No | Yes (specialty fee $300–$1,000/fund) |

| Handles Streamlined Procedures | No | Yes (essential for this process) |

| Audit defense | None or limited | Full representation included (most firms) |

| Tax treaty optimization | Limited | Yes, country-specific expertise |

| Multi-year planning | Not typically included | Yes — critical for FEIE election decisions |

Tax Software Cost Comparison Table (2026)

| Provider | Best For | Cost Range (2026) | FBAR Included? | Audit Support? |

|---|---|---|---|---|

| Greenback Expat Tax | All expat levels; first-timers | $399 – $1,200+ | ✅ Yes | ✅ Full audit defense |

| Bright!Tax | Complex situations; multi-country | $475 – $1,500+ | ✅ Yes | ✅ Comprehensive |

| MyExpatTaxes | Budget-conscious; simple W-2 | $199 – $399 | ✅ Yes | ❌ Limited email only |

| H&R Block Expat | Mid-complexity; brand familiarity | $275 – $800 | ✅ Yes | ⚠️ Fee-based |

| Boutique Expat CPA Firm | High net worth; foreign corporations | $1,500 – $5,000+ | ✅ Yes | ✅ Full representation |

Decision framework: If you are a W-2 employee earning under $90,000 in a single country with no foreign investments or entities, quality DIY expat software handles your situation competently for $149–$399. If you are self-employed, own foreign business interests, have investment accounts holding non-US funds, are running late on multiple years, or are in a complex family or property situation — professional guidance pays for itself through legitimate tax savings that software misses, plus the audit defense value.

📘 Free Resource: Complete Expat Financial Guide

Managing taxes abroad is just one piece of expat financial planning. Our free guide covers banking for expats, international money transfers, building and maintaining US credit while abroad, and structuring your finances across borders.

14. Frequently Asked Questions

Do US citizens living abroad have to file taxes every year?

Yes. Under the US citizenship-based taxation system (IRC § 61), all US citizens and green card holders must file a federal tax return annually if their gross income exceeds the applicable threshold ($13,850 for single filers in 2024), regardless of where they live or what taxes they pay to a foreign government. This obligation persists until you formally renounce citizenship or abandon your green card.

What is the Foreign Earned Income Exclusion limit for 2024 and 2025?

The FEIE limit is $126,500 for tax year 2024, and approximately $130,000 for tax year 2025 (indexed annually for inflation per IRC § 911(b)(2)(D)). This exclusion applies only to foreign earned income — wages, salary, and self-employment income for services performed in a foreign country. It does not apply to passive income such as dividends, interest, rental income, pensions, or Social Security benefits.

What is FBAR and who needs to file it?

FBAR (FinCEN Form 114) is required of any US person who had a financial interest in or signature authority over foreign financial accounts whose aggregate maximum value exceeded $10,000 at any single point during the calendar year. It is filed electronically through the BSA E-Filing System at bsaefiling.fincen.treas.gov by October 15, and is separate from your tax return. Non-willful violations carry penalties up to $10,000 per account per year; willful violations can reach 50% of the account balance.

What is the difference between FBAR and FATCA (Form 8938)?

FBAR (FinCEN Form 114) is filed separately with FinCEN and has a lower threshold ($10,000 aggregate). Form 8938 (FATCA) is filed with your Form 1040 and has higher thresholds for expats ($200,000 at year-end or $300,000 at any point for single filers living abroad). Form 8938 covers a broader universe of assets including foreign stocks, partnership interests, and trust interests — not just bank accounts. Having both filing obligations for the same accounts is common.

When is the US tax filing deadline for Americans living abroad?

Americans living and working outside the US and Puerto Rico receive an automatic two-month extension to June 15 (no application needed — attach a brief statement to your return). A further extension to October 15 is available by filing Form 4868 by June 15. Important: these are filing extensions only. Any taxes owed still accrue interest from April 15 at the current IRS underpayment rate (8% annually as of 2024). The FBAR (FinCEN Form 114) has its own separate automatic deadline of October 15.

Can I use both the FEIE and Foreign Tax Credit at the same time?

Yes, but not on the same income. You can use the FEIE (Form 2555) to exclude up to $126,500 of foreign earned income, and separately use the Foreign Tax Credit (Form 1116) on passive income (dividends, interest, capital gains) and any earned income above the FEIE cap. Applying both to the identical dollar of income is prohibited and generates an accuracy-related penalty of 20% on the underpayment.

Does the FEIE eliminate self-employment tax for freelancers abroad?

No. The Foreign Earned Income Exclusion eliminates federal income tax on excluded foreign earned income, but it does not affect self-employment (SECA) tax. A freelancer who excludes $74,000 under the FEIE still owes 15.3% SE tax on net self-employment income (approximately $10,451 on $74,000). The only way to reduce SE tax is through a totalization agreement with your country of residence (available in 30 countries) or by restructuring employment through a foreign corporation (which introduces its own complexity).

What is the Streamlined Foreign Offshore Procedure?

The Streamlined Foreign Offshore Procedures (SFOP) allow US taxpayers who are non-willfully non-compliant to file three years of delinquent tax returns and six years of FBARs without penalties. To qualify, you must have resided outside the US for at least one of the three years in question and certify on Form 14653 that your failure to file was non-willful (due to ignorance or misunderstanding, not intentional tax evasion). This program is available only before the IRS initiates contact about your non-compliance. Details at IRS.gov.

Do I owe state taxes if I move abroad?

It depends on your former state. Moving abroad does not automatically terminate state tax residency. States like California, New York, Virginia, and South Carolina have aggressive domicile rules and may continue to assert tax jurisdiction until you formally demonstrate that you have established domicile elsewhere. No-income-tax states (Florida, Texas, Nevada, Wyoming, South Dakota, Alaska, Washington) are the most favorable for expats. To sever domicile: sell or formally lease your property, obtain a foreign or out-of-state driver’s license, update voter registration, close local accounts, and file a final part-year resident return.

What happens if I never file US taxes while living abroad?

The IRS statute of limitations for audit never begins running until you file. For unreported foreign financial accounts, FBAR penalties of $10,000–$100,000+ per account per year can accumulate. FATCA means foreign banks report US account holders to the IRS directly — meaning non-filing is increasingly detectable. Under the FAST Act, seriously delinquent tax debt over $62,000 (2024) can trigger passport revocation or denial. Proactive compliance through the Streamlined Procedures while it is still available is far less costly than waiting for IRS enforcement.

Is the FEIE or Foreign Tax Credit better for expats in France or Germany?

For expats in high-tax countries like France (top marginal rate ~45%) or Germany (~45%), the Foreign Tax Credit (Form 1116) is typically superior to the FEIE. Since local income tax rates exceed comparable US rates on most income levels, the FTC often eliminates US tax liability entirely while generating carryforward credits for future years. The FEIE, by contrast, simply excludes income — it does not capture the value of high foreign taxes already paid. The optimal strategy requires modeling both scenarios for your specific income level, filing status, and income types.

Do green card holders living abroad have to pay US taxes?

Yes. Green card holders (Lawful Permanent Residents) are treated as US tax residents from the date they receive their green card until the date they formally abandon it via Form I-407 or a determination by a US immigration court. This means worldwide income must be reported on Form 1040 annually, FBAR must be filed for qualifying foreign accounts, and all other international reporting requirements apply — exactly as for US citizens. Green card holders who have held their status for 8 of the past 15 years and meet certain wealth thresholds may also face exit tax under IRC § 877A upon abandonment.

Can an American expat contribute to an IRA while living abroad?

Yes, but with a limitation: you can only contribute to an IRA from earned income that is NOT excluded under the FEIE. If you exclude your entire foreign salary using the FEIE, you have no “taxable compensation” remaining, and therefore cannot contribute to an IRA for that year. This is one reason some high earners prefer the Foreign Tax Credit over the FEIE — it preserves earned income in the taxable compensation base, allowing IRA contributions and Social Security work credits. If you have earned income above the FEIE cap, you can contribute up to $7,000 (2024) or $8,000 if age 50+ per year.

What is the Physical Presence Test for the FEIE?

The Physical Presence Test requires you to be physically present in one or more foreign countries for at least 330 full days during any consecutive 12-month period. A “full day” means the entire 24-hour period from midnight to midnight spent in a foreign country. Any day on which you set foot on US soil — even for a few hours in transit — does not count toward the 330 days. Days in international airspace or waters also do not count. Travel days departing or arriving in the US are counted as US days. This test is mechanical and objective; documenting it requires passport stamps, boarding passes, and a daily travel log.

How do I report foreign rental income on my US tax return?

Foreign rental income must be reported on Schedule E of Form 1040, just like US rental income. You report gross rents received, then deduct allowable expenses: mortgage interest, property taxes, insurance, repairs, depreciation (using the 30-year foreign property depreciation schedule under IRC § 168(g)), and management fees. Net rental income is taxed at ordinary income rates. If you paid foreign taxes on the rental income, you can claim Foreign Tax Credits via Form 1116 (passive basket) to offset US tax on that income. The FEIE does not apply to rental income — it applies only to earned income from personal services.

What forms are required for Americans who own a foreign business?

US persons who own 10% or more of a foreign corporation must file Form 5471 (Information Return of US Persons With Respect to Certain Foreign Corporations). The penalty for non-filing is $10,000 per form per year, increasing to $50,000 for continued failure after IRS notification — and the statute of limitations on the entire tax return remains open. Owners of foreign partnerships file Form 8865. Recipients of foreign gifts over $100,000 or distributions from foreign trusts file Form 3520 and/or Form 3520-A. These forms require professional preparation; errors are costly and common in DIY filings.

Are foreign mutual funds (UCITS) taxable for Americans abroad?

Yes — and punitively so. Foreign mutual funds, including European UCITS, are typically classified as Passive Foreign Investment Companies (PFICs) under IRC § 1297. Without making a special election (Qualified Electing Fund or mark-to-market), gains are taxed under the “excess distribution” regime: income is allocated across all holding years, taxed at the highest marginal rate for each year (even if you are now in a lower bracket), plus an interest charge. Effective rates can exceed 50%. Most expat tax advisors recommend avoiding non-US mutual funds entirely and holding US-domiciled ETFs instead. If you already hold PFICs, File Form 8621 for each fund and consider making an annual QEF election if the fund provides the required information.

How does currency fluctuation affect my US tax return?

All foreign income and expenses must be reported in US dollars. For recurring income items, the IRS allows use of the annual average exchange rate published at IRS.gov. For specific transactions like property sales or large one-time payments, you must use the spot rate on the actual transaction date. Currency gains (when the dollar value of a foreign payment is higher than its cost basis in dollars) are taxable as ordinary income under IRC § 988. Currency losses may be deductible. Consistent use of the correct rate for each category is important — inconsistency is a common audit trigger for international returns.

What is the exit tax when renouncing US citizenship?

The exit tax under IRC § 877A applies to “covered expatriates” — those who meet any of three tests: (1) average annual net income tax liability exceeded $190,000 (2024 threshold, inflation-adjusted) for the five preceding years; (2) net worth was $2 million or more on the expatriation date; or (3) failure to certify five years of tax compliance on Form 8854. Covered expatriates are treated as having sold all worldwide assets at fair market value the day before expatriation. Gains exceeding $866,000 (2024 exclusion) are taxed at capital gains rates. Deferred compensation and specified tax-deferred accounts face 30% withholding on future distributions. The State Department fee for renunciation is $2,350.

What should I do if I have not filed US taxes for several years?

If your non-filing was non-willful (you genuinely did not know about the requirement), the Streamlined Foreign Offshore Procedures are your best option. This IRS program allows you to file three years of delinquent returns and six years of FBARs without penalties, by certifying non-willful conduct on Form 14653. It is available only before the IRS initiates contact about your non-compliance. If your non-filing was willful, you may need to consider the Voluntary Disclosure Program (VDP), which involves negotiated penalty resolution. In either case, engage a specialized expat CPA or tax attorney — do not attempt catch-up filings for multiple years without professional guidance.

15. Final Thoughts

US expat tax compliance is genuinely complex — but it is manageable, and with the right knowledge, it does not have to be expensive. The system is built with robust protections against double taxation: the Foreign Earned Income Exclusion, Foreign Tax Credits, tax treaty provisions, and totalization agreements exist precisely to prevent Americans abroad from being taxed twice on the same income.

The five principles that protect every expat who applies them:

- File every year, regardless of what you owe. Non-filing is never the right answer. The penalties for non-filing are almost always more expensive than the taxes themselves.

- FBAR and FATCA are separate obligations with separate deadlines. Do not assume your tax return satisfies them.

- Choose your strategy — FEIE or FTC — deliberately. The wrong choice can cost thousands annually. Model both scenarios or ask a specialist before making the election.

- Sever state domicile formally. A Florida or Texas declaration before departing eliminates years of potential state tax liability.

- If you are behind, act now. The Streamlined Procedures are genuinely favorable — but they are available only before the IRS finds you first.

The peace of mind from being fully compliant — knowing you can renew your passport, travel freely, and plan your financial life across borders without IRS exposure — is worth the investment in getting this right.

🔍 Looking for the Best Banks and Financial Services for Expats?

Taxes are one piece of your expat financial picture. MoneyAbroadGuide also covers the best banks for Americans abroad, international money transfer services, credit building from overseas, and full expat financial planning.

Sources and References:

• IRS Publication 54 — Tax Guide for U.S. Citizens and Resident Aliens Abroad

• IRS: Foreign Earned Income Exclusion

• FinCEN: FBAR Filing System

• IRS: FATCA Overview

• IRS: Streamlined Foreign Offshore Procedures

• SSA: Totalization Agreements

• IRS Notice 2024-77: Foreign Housing Exclusion Amounts

• Internal Revenue Code §§ 61, 901, 904, 911, 1291, 6038D, 877A

About the Author: Talal Eddaouahiri is the Founder and Editor-in-Chief of MoneyAbroadGuide.com. A Moroccan immigrant to the USA with 15+ years of experience in international banking and cross-border financial services, he created MoneyAbroadGuide to help newcomers, immigrants, and expatriates navigate banking, taxes, credit, money transfers, and financial systems in the United States and Canada. This article was reviewed for accuracy as of June 2026 against official IRS, FinCEN, and US Treasury publications.

Written by Talal Eddaouahiri

Founder & Editor-in-Chief | Former International Banking Executive

Talal is a Moroccan immigrant to the USA with 15+ years of experience in international banking. He founded MoneyAbroadGuide to help newcomers navigate the financial complexities of moving abroad.