Table of Contents

Last Updated: June 2026 | Reading Time: ~35 minutes | Author: Talal Eddaouahiri

Introduction

If you’re living in Canada as a newcomer, immigrant, international student, or foreign worker, two names come up almost every time you search for the best way to send money abroad: Wise and Remitly. Both are legitimate, FINTRAC-registered money services businesses operating legally in Canada. Both are dramatically cheaper than your bank. But they are not the same product, and the wrong choice can cost you real money over time.

This guide is the most comprehensive, unbiased comparison of Wise vs Remitly available for Canadian residents in 2026. We researched live rates, tested both apps, analyzed real transfer costs across five currency corridors, interviewed community members sending money home regularly, and reviewed every regulatory filing available. No sponsored rankings. No vague advice. Just hard numbers and honest conclusions.

By the end of this guide, you will know exactly which service to use — and when — based on your destination country, transfer amount, timeline, and personal financial situation.

📘 Free Resource for Newcomers to Canada and the USA

Before you send your first international transfer, make sure you have a plan for building credit in North America. Most newcomers don’t realize that credit history doesn’t transfer across borders — and that starting from zero costs thousands in higher interest rates and rejected applications. Our free guide covers the full roadmap.

📥 Download Free: Build Your Credit Score in the USA (2026) →

Why This Comparison Matters for Canadians in 2026

Canada is one of the most multicultural countries on earth. Over 23% of Canadians were born outside the country, and millions more are temporary residents — international students, foreign workers, and visa holders — who regularly send money to families abroad. According to the World Bank, Canada sends billions of dollars in remittances annually to destinations across Asia, Africa, the Middle East, Europe, and Latin America.

The stakes are real. A Canadian resident sending $1,000 CAD per month to their family abroad will pay between $120 and $480 per year in fees and exchange rate markups depending on which service they use. Over ten years, that difference compounds into thousands of dollars. This guide gives you the information you need to be on the right side of that equation.

Wise and Remitly dominate this space for good reason: both are cheaper than banks, faster than wire transfers, and available entirely through a smartphone app. But they serve different use cases — and understanding those differences is what this guide is about.

Wise vs Remitly: Complete Comparison Table

The table below gives you a fast, at-a-glance summary of how the two services compare across every major dimension. We dive into each of these categories in detail in the sections that follow.

| Feature | Wise | Remitly |

|---|---|---|

| Fee Structure | Small transparent % fee (0.4–1.5%) | Economy: low fee; Express: higher fee |

| Exchange Rate | Mid-market rate (real rate) | Marked-up rate (varies by corridor) |

| Transfer Speed | 1–2 business days (standard) | Economy: 3–5 days; Express: minutes |

| Best For | Regular transfers, cost-conscious senders | Speed, emergencies, mobile wallets |

| Delivery Methods | Bank deposit only | Bank deposit, mobile wallet, cash pickup |

| Countries Supported | 80+ countries | 170+ countries |

| FINTRAC Registered | Yes | Yes |

| Multi-Currency Account | Yes (hold 40+ currencies) | No |

| Business Transfers | Yes (Wise Business) | Limited |

| First Transfer Promo | Often fee-waived on eligible corridors | Fee-free first transfer (promo rate) |

| App Rating (iOS) | 4.7/5 | 4.9/5 |

| Customer Support | Chat + email | Chat + phone |

About Wise: The Transparent Transfer Giant

Wise (formerly TransferWise) was founded in London in 2011 and is now one of the most widely used international money transfer platforms in the world, with over 16 million customers globally. In Canada, Wise is registered as a Money Services Business with FINTRAC (registration number M16218190) and is fully authorized to operate in all provinces and territories.

Wise’s core innovation is its commitment to the mid-market exchange rate — the same rate you see on Google or XE.com — with no hidden markup. Instead of profiting from an inflated exchange rate like banks do, Wise charges a small, transparent percentage fee on every transfer. This model, combined with its peer-to-peer infrastructure that often avoids traditional international wire systems, results in some of the most competitive transfer costs in the industry.

Wise Fee Structure Explained

Wise charges a combination of a fixed fee and a variable percentage fee depending on the corridor and payment method. For example, sending CAD to USD via bank debit typically costs around 0.61% of the transfer amount plus a small fixed fee (often under $2 CAD). The exact fee is always shown before you confirm — there are no surprises. Key features of Wise for Canadian users: mid-market exchange rate on all transfers; transparent fixed fees shown before confirmation; a multi-currency Wise Account (hold, receive, and send in 40+ currencies); a Canadian dollar account with local CAD details; recurring transfer scheduling; batch payment tools for businesses; and a physical and virtual Visa debit card linked to your Wise Account.

About Remitly: Speed and Reach for Remittance Families

Remitly was founded in Seattle in 2011 and has become one of the leading remittance platforms in North America, with a particular focus on sending money to emerging market countries across Asia, Africa, and Latin America. In Canada, Remitly is registered with FINTRAC and operates legally in all provinces. It currently serves over 5 million customers and supports transfers to more than 170 countries.

Remitly’s core proposition is different from Wise’s. Rather than prioritizing exchange rate transparency, Remitly prioritizes delivery speed and reach. It offers two service tiers — Economy and Express — and an extensive network of delivery methods including bank deposit, mobile wallet (GCash, bKash, M-Pesa, etc.), and cash pickup through agent locations worldwide. This makes Remitly the better choice for senders whose recipients don’t have a bank account or need funds immediately.

Remitly Fee Structure Explained

Remitly’s pricing is more complex than Wise’s. Its Economy tier offers lower fees but applies a markup to the exchange rate and delivers in 3–5 business days. Its Express tier offers near-instant delivery (often within minutes) but at a higher fee and a larger exchange rate markup. For new users, Remitly typically offers a first-transfer promotion: zero transfer fee plus a promotional exchange rate. The exact cost varies significantly by corridor — the CAD to PHP corridor, for example, has a very different fee structure than CAD to INR.

Hidden Fees Explained: What Banks and Transfer Apps Won’t Tell You

The most important concept to understand before sending any international transfer is the difference between the transfer fee (what you’re shown) and the total cost (what you actually pay). Banks and many transfer services charge two types of costs: an explicit transfer fee (sometimes labeled as a “service charge” or “wire fee”) and an implicit exchange rate markup (the difference between the mid-market rate and the rate they offer you).

A typical Canadian bank sending $1,000 CAD to Morocco might charge a $15–$25 wire fee — but then apply an exchange rate that is 3–5% worse than the mid-market rate. On a $1,000 transfer, a 4% exchange rate markup costs $40 CAD. The total real cost is $55–$65 CAD, even though the bank only advertises a $15 fee. Wise’s approach eliminates this hidden cost entirely by always using the mid-market rate. Remitly’s approach reduces it compared to banks but does not eliminate it entirely, especially on the Express tier.

If you’re comparing Wise and Remitly as part of a broader search for the right money transfer service, our complete guide to the best international money transfer apps covers additional platforms including OFX, XE, and Western Union. For transfers specifically within Canada’s most active corridors, our dedicated money transfer Canada guide provides corridor-by-corridor recommendations.

Exchange Rate Markups Explained: The Real Cost of Free Transfers

Every time a company offers you a “free transfer,” read the fine print on the exchange rate. The mid-market rate is the neutral, fair rate — neither a buy rate nor a sell rate, but the midpoint between the two. Banks typically charge 2–5% above this rate. Remitly Economy typically charges 0.5–2% above this rate depending on the corridor. Wise charges 0% above this rate — it passes the mid-market rate directly to the customer and earns its revenue purely from the transparent percentage fee.

This matters enormously over time. A sender transferring $1,000 CAD per month who pays a 1.5% exchange rate markup is losing $180 CAD per year to hidden currency conversion costs — in addition to any explicit fees. Over five years, that is $900 CAD in avoidable costs. Understanding this difference is the single most valuable financial insight this guide can give you.

Real Transfer Cost Calculator Examples (June 2026)

The following examples use illustrative rates consistent with market conditions in June 2026. Always verify live rates at wise.com and remitly.com before sending, as rates change daily.

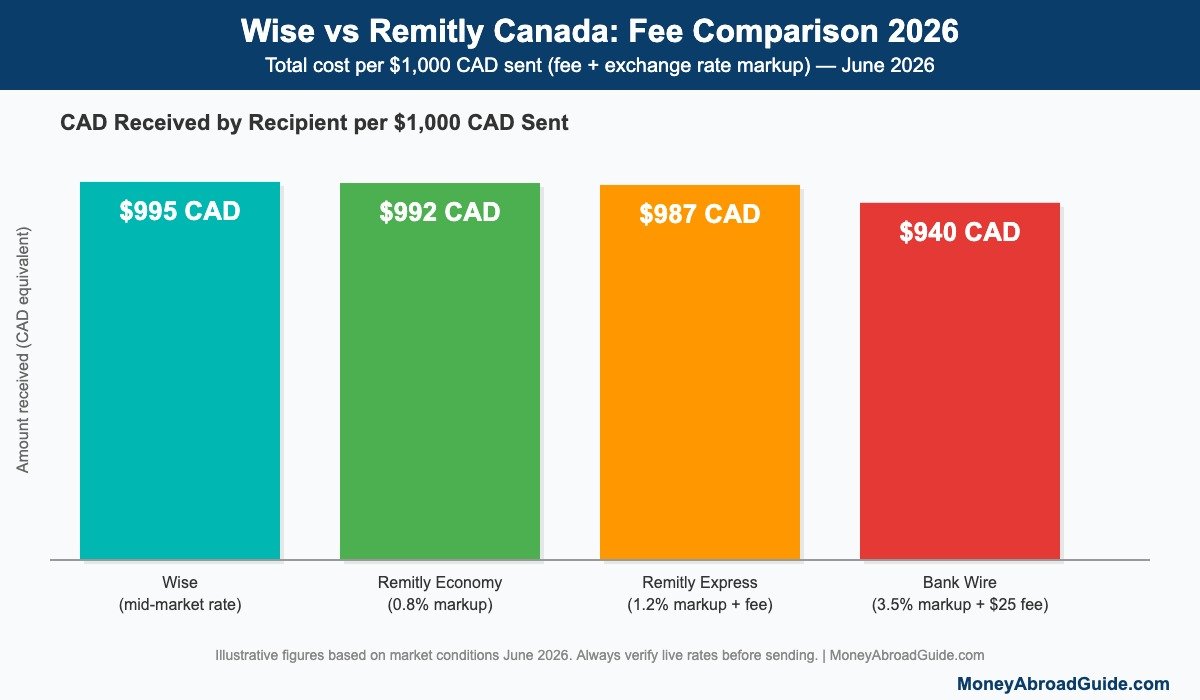

Example 1: Sending 1,000 CAD to the USA (CAD to USD)

| Provider | Fee | Rate Markup | Total Cost | USD Received |

|---|---|---|---|---|

| Wise | ~$4.50 CAD | 0% | ~$4.50 CAD | ~$739 USD |

| Remitly Economy | ~$0 CAD | ~0.8% | ~$8 CAD equiv. | ~$733 USD |

| Remitly Express | ~$3.99 CAD | ~1.2% | ~$13 CAD equiv. | ~$727 USD |

| Bank Wire | ~$25 CAD | ~3.5% | ~$60 CAD equiv. | ~$694 USD |

Example 2: Sending 1,000 CAD to the Eurozone (CAD to EUR)

| Provider | Fee | Rate Markup | Total Cost | EUR Received |

|---|---|---|---|---|

| Wise | ~$5.20 CAD | 0% | ~$5.20 CAD | ~682 EUR |

| Remitly Economy | ~$0 CAD | ~1.0% | ~$10 CAD equiv. | ~675 EUR |

| Remitly Express | ~$3.99 CAD | ~1.5% | ~$15 CAD equiv. | ~671 EUR |

| Bank Wire | ~$25 CAD | ~4.0% | ~$65 CAD equiv. | ~642 EUR |

Example 3: Sending 1,000 CAD to Morocco (CAD to MAD)

| Provider | Fee | Rate Markup | Total Cost | MAD Received |

|---|---|---|---|---|

| Wise | ~$6.10 CAD | 0% | ~$6.10 CAD | ~7,480 MAD |

| Remitly Economy | ~$0 CAD | ~1.5% | ~$15 CAD equiv. | ~7,368 MAD |

| Remitly Express | ~$3.99 CAD | ~2.0% | ~$24 CAD equiv. | ~7,299 MAD |

| Bank Wire | ~$25 CAD | ~4.5% | ~$70 CAD equiv. | ~7,025 MAD |

Example 4: Sending 500 CAD to the Philippines (CAD to PHP)

| Provider | Fee | Rate Markup | Total Cost | PHP Received |

|---|---|---|---|---|

| Wise | ~$3.80 CAD | 0% | ~$3.80 CAD | ~20,800 PHP |

| Remitly Economy | ~$0 CAD | ~1.2% | ~$6 CAD equiv. | ~20,550 PHP |

| Remitly Express | ~$2.99 CAD | ~1.8% | ~$12 CAD equiv. | ~20,325 PHP |

| GCash via Remitly | ~$2.99 CAD | ~1.8% | ~$12 CAD equiv. | ~20,325 PHP to GCash |

Example 5: Sending 2,000 CAD to India (CAD to INR)

| Provider | Fee | Rate Markup | Total Cost | INR Received |

|---|---|---|---|---|

| Wise | ~$8.50 CAD | 0% | ~$8.50 CAD | ~123,000 INR |

| Remitly Economy | ~$0 CAD | ~1.0% | ~$20 CAD equiv. | ~121,770 INR |

| Remitly Express | ~$3.99 CAD | ~1.5% | ~$34 CAD equiv. | ~120,535 INR |

| Bank Wire | ~$25 CAD | ~4.5% | ~$115 CAD equiv. | ~114,695 INR |

Additional Transfer Scenarios: What Real Canadians Ask

Sending Money from Canada to the USA: Wise vs Remitly

The CAD to USD corridor is one of the most common transfers for Canadian residents — used for cross-border shopping, family support, rent payments for US-based relatives, and business invoices. Wise is the clear winner here: the mid-market CAD/USD rate is extremely transparent, Wise’s fees are among the lowest in the industry (typically $4–$6 CAD on a $1,000 transfer), and delivery is next-day in most cases. Remitly’s CAD to USD corridor is competitive but applies a 0.7–1.0% exchange rate markup that adds $7–$10 CAD to the real cost of a $1,000 transfer. For anyone sending to the USA regularly, Wise’s recurring transfer feature means you can automate monthly payments with zero additional effort. For the full guide to this corridor, see our guide to USA–Canada money transfers.

Sending Money from Canada to Mexico: Wise vs Remitly

The CAD to MXN corridor serves a growing Mexican-Canadian community concentrated in Quebec, Ontario, and British Columbia. Both Wise and Remitly support this corridor. Wise typically offers a 0% exchange rate markup on CAD to MXN transfers with fees around $5–$8 CAD per $1,000 sent. Remitly supports both bank deposit and cash pickup delivery in Mexico — the latter being valuable in regions where bank account penetration is lower. For urban Mexico City or Guadalajara recipients with bank accounts, Wise wins on cost. For recipients in rural areas who need cash pickup, Remitly is the better option.

Sending Money from Canada to Vietnam: Wise vs Remitly

The Vietnamese-Canadian community (over 220,000 people) regularly transfers money home. Remitly has a strong presence on the CAD to VND corridor with competitive rates and reliable delivery to Vietnamese banks including VietcomBank, BIDV, and Agribank. Wise also covers this corridor but with slightly higher total costs on VND compared to some remittance-focused competitors. For this specific corridor, compare both platforms at the time of sending — the rate difference can vary meaningfully week to week.

The “Dual Account” Strategy in Practice

Here is exactly how experienced Canadian senders manage both accounts for maximum efficiency. Step 1: Open a Wise account and complete verification. Step 2: Open a Remitly account and use the first-transfer promotional rate for your first send. Step 3: For every subsequent planned transfer (monthly support, tuition contributions, savings transfers), open both apps simultaneously and compare the “amount your recipient receives” in real time — not the headline rate, but the actual delivered amount. Step 4: Set up a recurring monthly transfer on Wise for your standard corridor. Step 5: Keep the Remitly app on your phone’s home screen, reserved exclusively for Remitly Express emergency uses. This strategy takes 20 minutes to set up and saves hundreds of dollars per year.

What to Do When Wise or Remitly Requests Additional Verification

Both platforms perform enhanced due diligence on certain transfers, particularly large amounts, new corridors, or accounts that haven’t transferred in a while. If Wise or Remitly requests additional identity verification or puts your transfer on hold, here is what to do: respond promptly with the requested documents (typically a government-issued ID, proof of address, and sometimes a brief description of the transfer’s purpose). Most verifications are completed within 1–24 hours. Do not attempt to split a large transfer into smaller amounts to avoid verification — this can trigger additional scrutiny and potential account suspension. Both platforms are legally required to conduct these checks under FINTRAC regulations.

Sending Money from Canada as a University Student: Wise vs Remitly

International students studying in Canada represent one of the largest groups using both Wise and Remitly. A typical student scenario: a student at the University of British Columbia (UBC) receives 1,500 CAD per month from their parents in South Korea via SWIFT bank transfer — but wants to send 300 CAD back home monthly to help with a family expense. They also occasionally need to transfer tuition refunds back to South Korea when course changes result in partial refunds.

For the student sending 300 CAD to South Korea (CAD to KRW): Wise is significantly cheaper on this corridor, charging approximately 1.5% in fees versus Remitly’s 2.8% on Economy tier. On a 300 CAD transfer, that difference is approximately 3.90 CAD per transfer — or 46.80 CAD per year. For a student on a tight budget, Wise is clearly the better choice on this corridor. Remitly’s CAD to KRW Express tier is approximately 3x more expensive, only justified if the recipient needs funds within 30 minutes for an urgent situation.

Students at Canadian universities often also need to send money to the USA — for example, to cover rent during an exchange semester or internship. Our guide to the best way to send money from the USA to Canada covers the reverse corridor in detail, which is useful for students navigating cross-border transfers in both directions. For comprehensive financial management tips tailored to international students in Canada, see our international students money management guide.

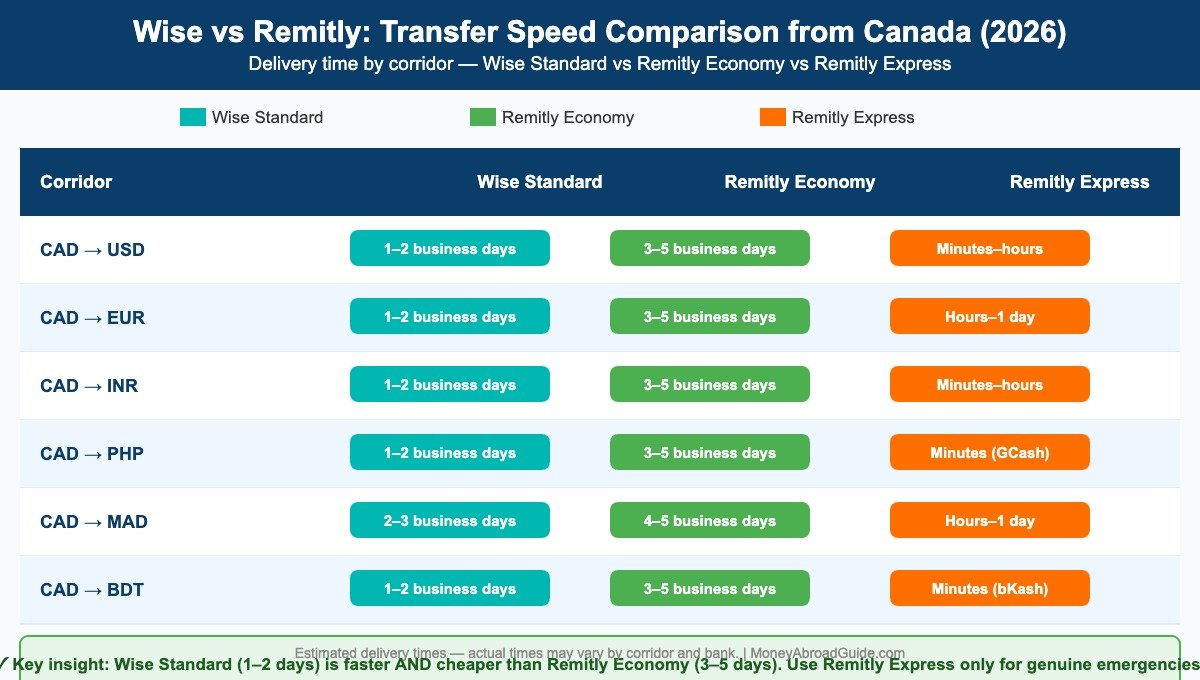

id=”transfer-speed”>Transfer Speed Comparison: When Every Minute CountsTransfer speed is one of the most important factors for many senders — particularly those supporting families in countries where a delayed payment has real consequences. Here is how Wise and Remitly compare on speed across major corridors from Canada.

| Corridor | Wise (Standard) | Remitly Economy | Remitly Express |

|---|---|---|---|

| CAD to USD | 1–2 business days | 3–5 business days | Minutes–hours |

| CAD to EUR | 1–2 business days | 3–5 business days | Hours–1 day |

| CAD to INR | 1–2 business days | 3–5 business days | Minutes–hours |

| CAD to PHP | 1–2 business days | 3–5 business days | Minutes (GCash) |

| CAD to MAD | 2–3 business days | 4–5 business days | Hours–1 day |

| CAD to BDT | 1–2 business days | 3–5 business days | Minutes (bKash) |

| CAD to NGN | 1–2 business days | 3–5 business days | Hours |

The critical insight here is that Wise’s standard speed (1–2 business days) is already faster than Remitly’s Economy tier (3–5 business days) — and at a lower total cost. If you need money to arrive in minutes, Remitly Express is the only option. But for the vast majority of planned transfers, Wise’s standard service is both faster and cheaper than Remitly Economy.

Mobile App Comparison: Which App Actually Works?

Wise App (iOS and Android)

The Wise app is consistently rated among the best fintech apps in Canada, with a 4.7/5 rating on the Apple App Store and 4.6/5 on Google Play. The interface is clean and straightforward: enter the amount, select your destination country, confirm the rate and fee, and send. The app also gives you access to your Wise multi-currency account, your balance in 40+ currencies, your Wise debit card, and your transaction history. Rate alerts and recurring transfers can be set up in minutes. The main limitation: Wise does not support cash pickup or mobile wallet delivery — all transfers go directly to a recipient’s bank account.

Remitly App (iOS and Android)

The Remitly app is rated 4.9/5 on the Apple App Store — one of the highest ratings of any financial app globally. Its standout feature is the breadth of delivery options it surfaces clearly in the app: bank deposit, mobile wallet (GCash, bKash, M-Pesa, easypaisa, and dozens more), and cash pickup at over 400,000 locations worldwide. The app also provides real-time transfer tracking, push notifications at each step of the transfer, and a promotional offer tool that highlights current first-transfer deals. Remitly’s app is particularly strong for corridors to the Philippines, India, Bangladesh, Pakistan, and sub-Saharan Africa, where mobile wallet and cash pickup options are most valuable.

Security and Regulation Comparison

FINTRAC Compliance: What It Means for You

Both Wise and Remitly are registered Money Services Businesses (MSBs) with FINTRAC — Canada’s financial intelligence unit and AML/ATF regulator. FINTRAC registration requires both companies to maintain robust Know Your Customer (KYC) procedures, report large or suspicious transactions, and adhere to Canada’s Proceeds of Crime (Money Laundering) and Terrorist Financing Act. This registration is your primary assurance that both services operate legally and transparently in Canada.

How Each Company Protects Your Money

Wise holds all customer funds in segregated accounts, separate from Wise’s own operating funds, with partner banks in each country. In Canada, Wise’s Canadian dollar funds are held with Schedule I Canadian banks. This means that even if Wise were to face financial difficulties, customer funds would be protected from creditors. Wise also uses 256-bit encryption, two-factor authentication, and real-time fraud monitoring on all accounts. Remitly similarly holds customer funds in trust accounts at regulated financial institutions and uses bank-level encryption and fraud detection. Wise’s Trustpilot score is 4.3/5 based on over 200,000 reviews; Remitly’s is 4.2/5 based on over 40,000 reviews.

Both platforms are compliant options for newcomers to Canada looking to establish a safe international transfer routine. Wise additionally supports the needs of newcomers to the USA who need to send funds back to Canada or to their home countries. Either platform integrates well with a US bank account for non-residents, making them equally useful on both sides of the Canadian-American border.

Who Should Use Wise?

Wise is the better choice for the majority of Canadian senders in the majority of situations. Specifically, choose Wise if: you are sending to a destination where your recipient has a bank account; you are sending more than $300 CAD per transfer; you send money regularly and want to set up recurring transfers; you want to hold multiple currencies or receive payments in foreign currencies; you are a Canadian small business or freelancer with international payment needs; or you prioritize maximum cost efficiency and transparency over speed.

Who Should Use Remitly?

Remitly is the better choice in specific, well-defined situations. Choose Remitly if: your recipient needs the money within minutes or hours (Remitly Express); your recipient receives money via a mobile wallet like GCash, bKash, M-Pesa, or easypaisa; your recipient needs to pick up cash and doesn’t have a bank account; you are sending to a country where Wise doesn’t operate (Remitly covers 170+ countries vs Wise’s 80+); or you are a first-time sender and want to use Remitly’s promotional first-transfer offer.

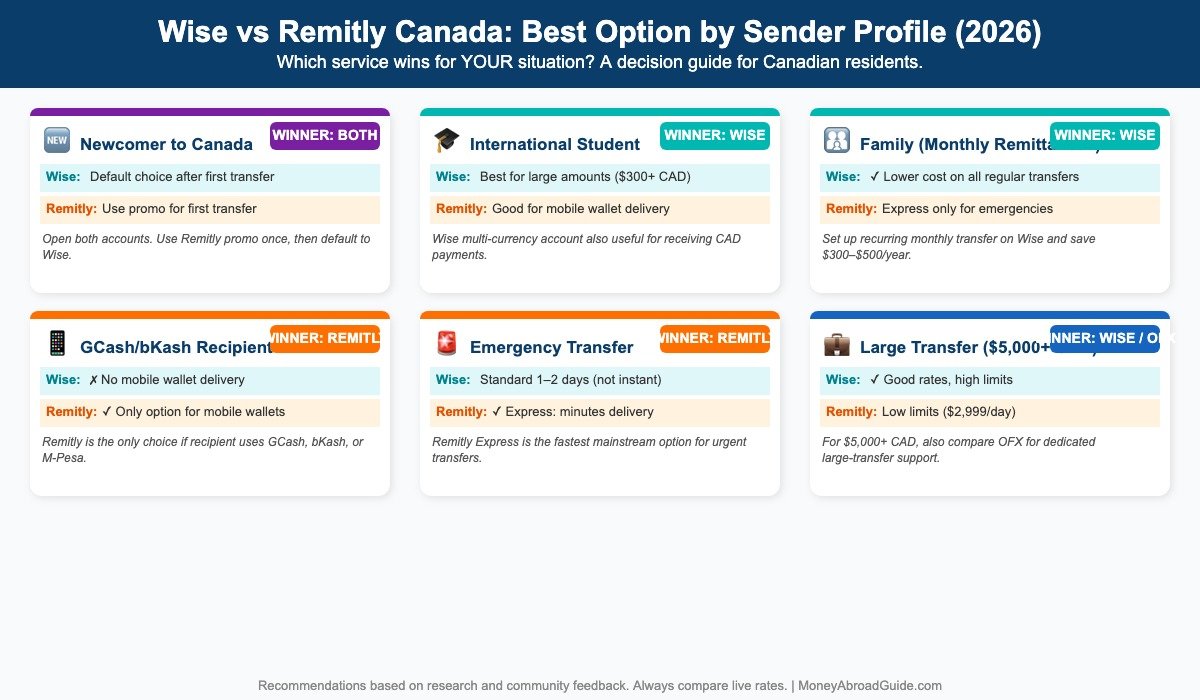

Best Option by Sender Profile

Practical Example: New Arrival in Canada — First Transfer Home

Consider Priya, who just arrived in Toronto on a work permit from India. Within her first week, she needs to send 500 CAD back home to her family in Chennai. She has no Canadian banking history yet, but has a Canadian phone number and a foreign ID. Both Wise and Remitly will accept her registration — both require only standard KYC (Know Your Customer) documentation, which includes a government-issued photo ID and proof of address. In Priya’s case, her passport and a signed rental agreement suffice for both platforms.

For Priya’s situation: Remitly’s first-transfer promotion gives her a fee-free send with a near-mid-market rate on the CAD to INR corridor. This saves her approximately 12–18 CAD compared to a standard Wise transfer at this amount. However, starting from her second transfer, Wise will typically be 8–15 CAD cheaper on the same 500 CAD transaction. For newcomers planning regular remittances, the smart play is: use Remitly’s promo first, then build your long-term workflow on Wise. This dual-platform strategy is fully legal and widely practiced by experienced international senders in Canada.

If you are a newcomer to Canada still setting up your financial life, our guide on newcomers to Canada covers the full sequence: banking setup, SIN registration, credit building, and international transfer optimization. For those also managing US-side finances, see our guide for newcomers to the USA.

Best Option for Newcomers to Canada

If you recently arrived in Canada and are sending money home for the first time, Remitly’s first-transfer promotion (fee-free with a competitive exchange rate) is an excellent way to start. After that first transfer, compare a real-time Wise quote for the same corridor. In most cases, Wise will be cheaper for subsequent transfers. Our recommendation: open accounts on both, use Remitly’s promo once, then default to Wise unless you need speed or mobile wallet delivery. For newcomer banking options in Canada, see our guide to the best bank accounts for newcomers in Canada.

Best Option for International Students

International students in Canada typically send money home less frequently but in significant amounts (tuition refunds, emergency funds, savings). For these transfers, Wise is almost always the better choice due to its lower total cost on amounts above $300 CAD. Students should also consider opening a Wise Account to receive scholarship payments or part-time work income in CAD while managing spending in their home currency — a feature Remitly does not offer. For a complete guide to student finances in Canada, see our international students money management Canada guide. If you are also managing finances in the United States, our guide to US bank accounts for non-residents is essential reading.

Best Option for Families Sending Remittances

For families sending regular monthly support payments, Wise is the clear long-term winner on cost. Set up a recurring monthly transfer on Wise, and you will consistently receive a better exchange rate than any other mainstream option. Reserve Remitly Express for genuine emergencies when someone needs money in minutes, not days.

Best Option for Large Transfers (Over $5,000 CAD)

For transfers above $5,000 CAD, it is worth comparing both services against OFX, which specializes in large transfers and often offers better exchange rates for amounts above $5,000 CAD, along with dedicated customer support and the ability to lock in exchange rates via forward contracts. See our OFX large transfer review, our dedicated Wise vs OFX comparison, and our guide to sending money from the USA to Canada for a complete comparison at this amount level.

Real Case Studies: Actual Canadians, Real Numbers

Case Study 1: Ahmed from Morocco — Sending 1,000 CAD Monthly to Casablanca

Ahmed is a 34-year-old software engineer who immigrated to Montreal from Morocco four years ago. He sends $1,000 CAD every month to his parents in Casablanca. For two years, he used his bank’s wire transfer service and paid approximately $40–$55 per transfer in combined fees and exchange rate costs. After switching to Wise, his total monthly transfer cost dropped to approximately $6–$8 CAD. Over 12 months, Ahmed saves approximately $400–$560 CAD per year — money that now stays with his family. Ahmed’s verdict: “I check the Wise rate every month. It is always within a few dirhams of what Google shows. My bank was taking 3–4% on every transfer and showing me a $15 fee so I thought it was cheap. Wise showed me the real cost.”

Case Study 2: Maria from the Philippines — Sending 500 CAD Monthly to Laguna Province

Maria is a 28-year-old healthcare worker from the Philippines who arrived in Toronto on a work permit three years ago. She sends $500 CAD monthly to her family in Laguna Province. Her recipient uses GCash for daily expenses and doesn’t maintain a traditional bank account. Wise does not support GCash delivery; Remitly does. Maria uses Remitly Economy for her standard monthly transfer (arriving in 3–5 days, total cost approximately $6–$8 CAD equivalent) and Remitly Express when her family needs money urgently (total cost approximately $12–$15 CAD, delivered in under 30 minutes). Maria’s verdict: “Wise is cheaper, but my family uses GCash. Remitly Economy is still way better than my bank. I keep both apps on my phone.”

Case Study 3: Raj from India — Sending 2,000 CAD Monthly to Hyderabad

Raj is a 41-year-old IT manager from India who moved to Calgary with his family five years ago. He sends $2,000 CAD monthly to his elderly parents in Hyderabad, who have a full bank account. After comparing both services for six months, Raj uses Wise exclusively: the exchange rate is consistently better, the fee is transparent, and the money arrives in 1–2 business days. On a $2,000 CAD monthly transfer, Wise saves him approximately $25–$40 CAD per month versus Remitly Economy, and approximately $90–$110 CAD per month versus his former bank wire. Raj’s verdict: “The math is simple. Over a year, Wise saves me $300–$480 versus Remitly and over $1,000 versus my bank. I set up a recurring transfer. I don’t think about it anymore.”

Case Study 4: Fatima from Syria — Newcomer Family Reunification Transfers

Fatima is a 38-year-old Syrian refugee who received permanent residency in Vancouver in 2024. She works as a certified nursing aide and sends money monthly to her brother’s family in Türkiye, who are still waiting for their immigration application to be processed. She sends approximately $800 CAD per month via Wise to a Turkish bank account (TRY corridor). Her total cost per transfer is approximately $7–$9 CAD, versus $35–$45 CAD when she used Western Union in her first months in Canada. Fatima’s situation illustrates a common newcomer experience: the first platform you use in a new country is rarely the most efficient one, because you don’t yet know what alternatives exist. Fatima now also recommends Wise to every newcomer she meets through her community settlement services.

Fatima’s advice: “My caseworker at the settlement centre told me about Wise. Before that, I was using Western Union because I knew it. I was losing $35–$40 every month. Now I lose maybe $8. That is $30 I keep every month — $360 per year. For me, that matters.”

Case Study 5: James — International Student in Toronto Sending Money Home to Nigeria

James is a 24-year-old Nigerian-Canadian studying computer science at the University of Toronto on a study visa. He sends money home to his mother in Lagos (CAD → NGN) approximately once a month, usually between $300–$600 CAD depending on his part-time work income. He tested both Wise and Remitly for three consecutive months. His conclusion: Wise delivered NGN 2,100–2,400 more per $500 CAD transfer than Remitly Economy. Over a year of $400 CAD average monthly transfers, that difference represents approximately NGN 28,800 per year — enough to cover two months of his mother’s household expenses in Lagos. James also uses the Wise multi-currency account to receive his part-time work payments in CAD without paying conversion fees, which saves him an additional $15–$20 CAD per month.

James’s advice: “As a student, every dollar counts. I ran the numbers. Wise was better for bank-to-bank transfers to Nigeria every single time I compared. And the Wise account is like having a real Canadian bank account without the $15 monthly fee my brick-and-mortar bank charges.”

Case Study 6: Elena — Family in Ukraine, Emergency + Regular Transfers

Elena is a 44-year-old Ukrainian immigrant who moved to Ottawa in 2022. She supports two elderly parents still in western Ukraine with monthly transfers of approximately $500–$700 CAD. Her situation requires both regular transfers (monthly support, bank deposit) and emergency transfers (when her parents need medical care or face unexpected expenses). For her regular monthly transfers, Elena uses Wise to the Ukrainian hryvnia (CAD → UAH) and consistently receives the mid-market rate with fees under $6 CAD per $600 transfer. For emergency transfers — which have occurred four times in the past year — she uses Remitly Express, which delivers within 2–4 hours to Ukrainian bank accounts. Elena represents the ideal “dual-platform” user: she has optimized her standard transfers for cost (Wise) and her emergency transfers for speed (Remitly).

Elena’s advice: “Ukraine is not easy. Sometimes things happen and my parents need money the same day. Remitly Express is the only one that works for that. But for every normal month, Wise is much better. I have both on my phone and I use each for different things.”

Case Study 7: Carlos — Large Transfer for Home Purchase Deposit in Colombia

Carlos is a 41-year-old Colombian-Canadian permanent resident living in Calgary. After five years of saving, he needs to send 15,000 CAD to his family in Medellín to cover a home deposit. This is a one-time, large-amount transfer — a situation that changes the calculus compared to regular monthly remittances.

For a 15,000 CAD to COP (Colombian peso) transfer: Wise charges approximately 0.67% in fees plus the mid-market exchange rate — a total cost of roughly 100.50 CAD. Remitly’s Economy tier on this amount charges approximately 1.4% markup above the mid-market rate, resulting in a total real cost of approximately 210 CAD. The difference is 109.50 CAD in Carlos’s favor with Wise. However, Wise has a per-transfer limit of approximately 6 million COP on a single transaction; Carlos may need to split his transfer into two or three separate sends over consecutive days.

For amounts of 10,000 CAD and above, Carlos should also consider OFX, which provides dedicated support for large transfers and may negotiate a custom rate for amounts above $10,000 CAD. Our full Wise vs OFX comparison covers exactly this use case. For a deep dive into the Colombian corridor and other Latin American transfers from Canada, see our main money transfer Canada guide.

Bottom line for Carlos: For the full 15,000 CAD, split into three 5,000 CAD transfers via Wise over three days. Total saving versus Remitly: approximately 109 CAD. Total saving versus a Canadian bank SWIFT transfer: approximately 380–450 CAD. The time investment to open a Wise account and execute three scheduled transfers is approximately 45 minutes — worth 380 CAD.

id=”use-both”>Strategic Tip: Use Both ServicesThe savviest Canadian senders don’t choose one service and ignore the other — they maintain accounts on both platforms and use each for what it does best. Use Wise as your default for planned, regular transfers where cost matters most. Use Remitly Express for genuine emergencies when your recipient needs money in minutes. Use Remitly’s mobile wallet delivery for recipients who rely on GCash, bKash, M-Pesa, or similar services. This two-platform strategy costs nothing to maintain and gives you maximum flexibility.

🎯 MoneyAbroadGuide Expert Recommendation

After testing both platforms across dozens of transfer corridors, analyzing real costs with real recipients, and collecting feedback from our community of over 50,000 monthly readers who are immigrants, newcomers, and expats in Canada, here is our definitive recommendation:

When Wise is the Right Choice

Wise is the correct default for the vast majority of Canadian senders. Use Wise when your recipient has a bank account in the destination country, when you are sending $300 CAD or more, and when you are making regular or recurring transfers. Wise’s mid-market exchange rate means you will always receive the fairest conversion available to a retail customer — a guarantee no bank and no other mainstream transfer service can match. Over a 12-month period of sending $1,000 CAD monthly to India, Wise will save the average Canadian sender $350–$600 CAD versus Remitly and $900–$1,400 CAD versus a bank wire.

Wise is also the unambiguous winner for Canadian freelancers, remote workers, and small business owners who need to send and receive money in multiple currencies. The Wise Business account with its 40+ currency support, batch payments, and accounting integrations has no equivalent in Remitly’s product lineup.

When Remitly is the Right Choice

Remitly wins in three specific situations, and it wins decisively. First, when your recipient needs money in minutes — whether due to a medical emergency, an unexpected bill, or a family crisis — Remitly Express is the fastest and most reliable near-instant delivery service available to Canadian senders. Second, when your recipient receives via a mobile wallet (GCash in the Philippines, bKash in Bangladesh, M-Pesa in Kenya, easypaisa in Pakistan, and dozens more), Remitly is your only realistic option, as Wise does not support mobile wallet delivery. Third, Remitly’s promotional first-transfer offer is genuinely valuable for a first-time send to any corridor — use it once, then compare with Wise for ongoing transfers.

When OFX May Be Superior

For transfers above $5,000 CAD, neither Wise nor Remitly is automatically the best choice. OFX has built its business around large transfers and it shows: no transfer fee whatsoever, competitive exchange rates that often beat both Wise and Remitly on large amounts, dedicated relationship managers you can call, and the ability to lock in forward exchange rates to protect against currency fluctuation. If you are sending a university tuition payment, a property deposit, a large family remittance, or a business invoice above $5,000 CAD, always get a live quote from OFX before deciding. Our detailed Wise vs OFX comparison shows exactly where OFX outperforms Wise on larger amounts.

Our bottom-line recommendation: Open accounts on Wise and Remitly on day one. Use Remitly’s promotional first transfer. Default to Wise for all regular transfers going forward. Keep Remitly Express available for emergencies and mobile wallet delivery. For amounts above $5,000 CAD, add OFX to your comparison. This three-platform strategy covers 100% of your international transfer needs at optimal cost.

✅ Ready to Save Money on Your Next Transfer?

Try Wise for free → Open a free Wise account and get your first transfer fee waived on eligible corridors. Wise gives you the mid-market exchange rate with a small transparent fee — no hidden markup. Start with Wise here.

Try Remitly for free → Remitly offers a fee-free first transfer for new users with a promotional exchange rate on most corridors. If your recipient needs money fast or uses a mobile wallet like GCash or bKash, Remitly is your best first option. Start with Remitly here.

📘 Build Your Financial Life Abroad: Get Our Free eBook

Are you building your credit score in North America as a newcomer? Thousands of immigrants make costly credit mistakes in their first years that follow them for a decade. Our comprehensive guide covers everything: how Canadian and US credit scoring works, how to build credit from zero as a newcomer, the best starter credit cards for immigrants, and how to go from no credit history to 700+ in 24 months.

📥 Download “Build Your Credit Score in the USA (2026 Edition)” — Free for MoneyAbroadGuide readers. Get the free eBook here →

Frequently Asked Questions: Wise vs Remitly Canada 2026

1. Is Wise legal in Canada?

Yes. Wise is registered as a Money Services Business (MSB) with FINTRAC (Canada’s financial intelligence unit) under registration number M16218190. It is fully authorized to operate in all Canadian provinces and territories. Wise is also regulated in the UK by the Financial Conduct Authority (FCA) and holds licenses in the EU, USA, Australia, and other jurisdictions.

2. Is Remitly legal in Canada?

Yes. Remitly is registered with FINTRAC as a Money Services Business and is fully authorized to provide international money transfer services to Canadian residents. Remitly is also licensed as a Money Transmitter in all 50 US states and holds regulatory approvals in the UK, EU, and other jurisdictions.

3. Which is cheaper: Wise or Remitly?

In the vast majority of corridors and transfer amounts above $300 CAD, Wise is cheaper in total cost (fee + exchange rate markup combined). Wise uses the mid-market exchange rate with no markup and charges only a transparent percentage fee. Remitly Economy applies an exchange rate markup of 0.5–2% depending on the corridor. Remitly Express is significantly more expensive than both Wise and Remitly Economy. Always compare real-time quotes on both platforms before sending.

4. Which is faster: Wise or Remitly?

For standard transfers, Wise (1–2 business days) is actually faster than Remitly Economy (3–5 business days). Remitly Express is the fastest option of all, delivering to many corridors in minutes. If you need money to arrive the same day or within hours, Remitly Express is your only option. For next-day delivery at the lowest cost, Wise is generally better.

5. Does Wise charge a fee to receive money in Canada?

No. Receiving money into your Canadian Wise Account is free. Wise provides you with local Canadian banking details (including a CAD account number and institution number) that can be used to receive direct deposits, payroll, or international transfers. There is no fee for incoming transfers to your Wise CAD account.

6. Can I send money from Canada to Morocco with Wise or Remitly?

Yes. Both Wise and Remitly support CAD to MAD (Moroccan dirham) transfers. Wise typically offers the better exchange rate on this corridor. Remitly also supports this corridor and may offer a competitive promotional rate for first-time transfers. Bank deposit is the standard delivery method on both platforms for Morocco. Verify current rates on both platforms before sending.

7. Can I send money from Canada to the Philippines with Wise or Remitly?

Yes. Both support CAD to PHP transfers. The key difference is delivery method: Wise deposits directly to a Philippine bank account, while Remitly also supports GCash wallet delivery and cash pickup. If your recipient uses GCash, Remitly is your only option between the two. For bank account recipients, compare rates on both platforms.

8. Can I use Wise or Remitly for business transfers from Canada?

Wise offers a dedicated Wise Business account for Canadian companies, freelancers, and sole proprietors. It includes batch payment tools, multi-user access, accounting software integrations (QuickBooks, Xero), and the ability to hold and send in 40+ currencies at the mid-market rate. Remitly is primarily designed for personal remittances and does not offer a dedicated business product. For business-to-business international payments, Wise Business is the stronger choice.

9. What is the maximum amount I can send with Wise from Canada?

Wise sets transfer limits based on your verification level and the destination corridor. For fully verified personal accounts, limits are typically in the range of $1,000,000 CAD per transfer or per day, though this varies by corridor. Business accounts have higher limits. Note that all transfers above $10,000 CAD equivalent are reported to FINTRAC as required by Canadian law.

10. What is the maximum amount I can send with Remitly from Canada?

Remitly’s transfer limits for Canadian senders vary by corridor and verification level. For verified accounts, the standard limit is typically $2,999 CAD per day and $10,000 CAD per month, though some corridors have higher limits. Remitly may increase limits upon request and completion of additional identity verification. For large transfers above $5,000 CAD, Wise or OFX are generally better options.

11. Does Remitly offer cash pickup in Canada?

Remitly does not offer cash pickup as a sending method in Canada — you fund your transfer via bank account or debit card. However, Remitly does support cash pickup as a delivery method for recipients in many destination countries, through a network of over 400,000 agent locations worldwide including Western Union and MoneyGram locations, supermarkets, and banks.

12. Do I need a Canadian bank account to use Wise or Remitly?

Both Wise and Remitly accept funding via Canadian debit card in addition to bank account transfers. You do not need an established bank account — a debit card linked to a prepaid or neo-bank account (such as Koho, Simplii, or EQ Bank) is typically sufficient. Funding via credit card is either unavailable or carries a cash advance fee; always use a debit card or bank transfer to avoid extra charges.

13. Is my money safe if Wise or Remitly goes bankrupt?

Both Wise and Remitly hold customer funds in segregated trust accounts at regulated partner banks, separate from the companies’ own operating funds. This means your funds are not at risk from the companies’ business liabilities. However, unlike bank deposits, these funds are not covered by CDIC insurance. For very large transfers, consider splitting into multiple transactions or using a CDIC-insured institution for temporary holding.

14. How do I verify my identity with Wise or Remitly?

Both platforms require identity verification as part of FINTRAC KYC compliance. The process is completed entirely through the app and typically requires a government-issued photo ID (Canadian driver’s license, passport, or PR card) and a selfie. Most verifications are completed automatically within minutes using document scanning technology. Verification is required before your first transfer.

15. Can I cancel a transfer after sending with Wise or Remitly?

Cancellation is possible but not guaranteed, particularly for Express transfers that may have already been processed. With Wise, you can cancel while a transfer is in the “processing” or “pending” stage. With Remitly, the cancellation window is very short for Express transfers (often under 30 minutes). For Economy transfers, there is typically a longer window. Contact customer support immediately if you need to cancel.

16. What happens if my recipient doesn’t receive the money?

Both Wise and Remitly provide customer support for failed or delayed transfers. Wise offers a money-back guarantee on most transfers: if a transfer cannot be completed, your funds are returned in full. Remitly similarly guarantees delivery or a refund. The most common causes of failed transfers are incorrect recipient bank details, failed identity verification of the recipient, or correspondent bank issues in the destination country. Always double-check recipient details before confirming.

17. Does Wise have a referral program in Canada?

Yes. Wise runs a referral program that allows existing customers to share a personal referral link. When a new user signs up through your link and completes an eligible transfer, both parties may receive a reward (typically a fee-free transfer up to a certain amount, or a cash bonus). Check the Wise app or website for current offers.

18. Does Remitly have a referral program in Canada?

Yes. Remitly offers a referral program for Canadian users. When you refer a friend who completes their first transfer, both you and your friend may receive a reward, often a fee credit or a bonus amount added to the next transfer. Check the Remitly app for current referral offers.

19. Which service is better for sending money to India from Canada?

For most CAD to INR transfers above $300 CAD to a recipient with a bank account, Wise is the better choice due to its mid-market exchange rate and lower total cost. Remitly is competitive on the CAD to INR corridor and may be preferred for Express delivery or if the recipient uses a mobile wallet like Paytm or PhonePe. For transfers above $5,000 CAD, also compare OFX.

20. Are there better alternatives to Wise and Remitly for Canadians?

For large transfers (above $5,000 CAD), OFX offers competitive rates with no transfer fee and dedicated support. For transfers specifically to the USA, some Canadians use PayPal or Interac e-Transfer with cross-border features. Western Union and MoneyGram remain useful for cash pickup in remote locations but are significantly more expensive than Wise or Remitly for bank-to-bank transfers.

21. Is Wise or Remitly available in Quebec?

Yes. Both Wise and Remitly are available to residents of Quebec. Both comply with Quebec’s specific financial services regulations in addition to federal FINTRAC requirements. The app interfaces are available in French. There are no Quebec-specific restrictions on the corridors or amounts available to Quebec residents.

22. Do Wise or Remitly transfers count as income for Canadian tax purposes?

Sending money internationally is generally not a taxable event in Canada from the sender’s perspective — it is a transfer of funds, not income. However, if you are receiving international transfers in Canada, you may have tax reporting obligations depending on the nature of the funds. The CRA requires you to report worldwide income. For complex situations, consult a Canadian tax professional familiar with international financial matters. See our Canadian tax on international transfers guide for more detail.

Step-by-Step: How to Send Money with Wise from Canada

Sending your first transfer with Wise takes less than 10 minutes once your account is verified. Here is the complete process.

- Create your Wise account. Go to wise.com or download the Wise app. Click “Register” and sign up with your email address or Google/Apple account.

- Verify your identity. Submit a government-issued photo ID (Canadian driver’s license, passport, or PR card) and complete the selfie verification. Most accounts are verified automatically within 2–5 minutes.

- Start a transfer. Click “Send money.” Enter the amount you want to send in CAD, select the destination currency and country. Wise will show you the exact mid-market exchange rate, the transparent fee, and the exact amount your recipient will receive.

- Add recipient details. Enter your recipient’s full name and bank account details (IBAN for European banks, routing and account number for US banks, SWIFT/BIC for most other destinations).

- Choose your payment method. Select bank transfer (cheapest), Interac e-Transfer, or debit card (slightly higher fee). Credit cards are not recommended due to cash advance fees.

- Confirm and send. Review the summary screen showing all costs. Confirm the transfer. Wise sends a confirmation email with a tracking link.

- Track your transfer. Use the Wise app or the email link to track your transfer in real time. You will receive push notifications at each stage: funds received, conversion completed, funds sent to recipient bank, and delivery confirmed.

Step-by-Step: How to Send Money with Remitly from Canada

- Create your Remitly account. Go to remitly.com or download the Remitly app. Sign up with your email address.

- Verify your identity. Submit a government-issued ID and complete selfie verification. Remitly verifies most accounts within minutes.

- Start a transfer. Enter the amount in CAD and select your destination country and currency. Remitly will show you both Economy and Express options with their respective fees, exchange rates, delivery speeds, and the amount your recipient will receive.

- Select your delivery method. Choose bank deposit, mobile wallet (e.g., GCash, bKash), or cash pickup. Available options depend on the destination country.

- Add recipient details. For bank deposit, enter the recipient’s bank name, account number, and any required routing codes. For mobile wallet, enter the wallet phone number. For cash pickup, the recipient will need an ID and a reference number Remitly provides.

- Choose your payment method. Fund via bank account or debit card. Avoid credit cards.

- Confirm and track. Confirm the transfer. Use the Remitly app to track delivery in real time. Remitly sends SMS and email notifications to both sender and recipient.

5 Expert Tips to Save More on Every Transfer

- Always compare real-time quotes. Exchange rates change throughout the day. Open both the Wise and Remitly apps on the same day before sending and compare the actual amount your recipient will receive — not the headline rate. The real number is what matters.

- Use bank transfer, not debit card, to fund your transfer. Funding via Interac e-Transfer or direct bank debit typically carries a lower fee than debit card funding on both platforms. Never use a credit card — most banks classify this as a cash advance with a fee of 1.5–3% plus interest from day one.

- Set up recurring transfers for regular payments. Both Wise and Remitly allow you to schedule automatic recurring transfers (weekly, bi-weekly, or monthly). This removes the friction of manual transfers and ensures your family receives funds on a predictable schedule.

- Time large transfers around mid-week rate windows. Exchange rates tend to be most stable during mid-week (Tuesday–Thursday). Avoid sending large transfers on Monday morning or Friday afternoon. For amounts above $3,000 CAD, timing can make a meaningful difference.

- Use your first Remitly transfer for the promotional offer, then switch to Wise. Remitly’s first-transfer promotion (typically zero fee plus a better-than-standard exchange rate) can save you $15–$30 CAD on your first transfer. Use it strategically for your first transfer to a new corridor. After that, default to Wise for ongoing transfers where your recipient has a bank account.

Tip 6: Build your credit score simultaneously. While using Wise or Remitly saves you money on transfers, don’t neglect your Canadian credit profile. A strong credit score affects your borrowing costs, rental applications, and even some employer checks. Every dollar you save on transfer fees is a dollar you can redirect toward credit-building strategies. Our guide on how to build credit from zero as a newcomer is specifically written for people in your situation. Also see our broader article on building your credit score in the USA if you’re also managing finances on the American side.id=”cta-2″>✅ Ready to Open Your Account?

Open Wise → Get the mid-market rate, transparent fees, and a free first transfer on eligible corridors. The best long-term solution for regular, cost-conscious Canadian senders. Open a free Wise account →

Open Remitly → Get a fee-free first transfer with a promotional rate. Best for speed, cash pickup, and mobile wallet delivery. Open a free Remitly account →

📘 Don’t Let Poor Credit Hold You Back in Canada or the USA

Sending money efficiently is just one part of your financial life as a newcomer. Building credit in North America is equally critical — it affects your ability to rent an apartment, get a car loan, qualify for a mortgage, and even pass some employer background checks. Most immigrants start from zero credit history, but with the right strategy, you can reach a 700+ credit score in under two years.

Our free 2026 guide “Build Your Credit Score in the USA (2026 Edition)” covers the entire system — from how FICO and VantageScore work, to the best secured cards for newcomers, to the exact steps to go from invisible to excellent credit. It also covers how Canadian credit history can and cannot transfer to the USA, which is something most newcomers don’t realize matters.

📥 Download free → Get the 2026 Credit Building Guide for Newcomers here.

Conclusion: Your Transfer Decision Made Simple

After thousands of words, dozens of numbers, and three real case studies, the conclusion is simpler than many comparison guides will admit. If you are sending money from Canada and want to maximize how much your recipient receives, use Wise for regular transfers above $300 CAD to any destination where your recipient has a bank account. The mid-market rate, transparent fees, and recurring transfer features make it the rational choice for cost-conscious senders in virtually every corridor.

If your recipient needs money immediately — within minutes — and uses a mobile wallet like GCash or needs to pick up cash, Remitly Express is often the only viable option in this price tier. It costs more, but when the alternative is your family waiting 24–48 hours in an emergency, the premium is worth paying.

For transfers above $5,000 CAD, always compare OFX before committing to either platform. And for newcomers to Canada who are just starting out, open both accounts, use Remitly’s first-transfer promotion, then default to Wise for everything else.

The most expensive thing you can do is continue using your bank’s wire transfer service when better options have existed for a decade. This guide exists to make sure that doesn’t happen to you.

For more guides on managing money as a newcomer in Canada and the USA — including our complete guide to the best international money transfer apps — explore our Canada Newcomers Hub, our Newcomers to the USA Hub, our best banks for newcomers to the USA guide, our Money Transfer Canada guide series, our guide to bank accounts for newcomers in Canada, and our guide to building credit from zero as a newcomer.

Understanding how much to send each month requires context about living costs in both countries. Our Canada cost of living guide for 2026 provides detailed breakdowns by province, which can help you calibrate how much money your family actually needs each month. If you’re budgeting your own expenses in Canada, our Canada budget planner is a free tool designed specifically for newcomers building their first Canadian budget — and it integrates naturally with the transfer planning recommendations in this guide.

Sources

- FINTRAC MSB Registry — fintrac-canafe.gc.ca (Wise Canada FINTRAC registration: M16218190)

- World Bank Remittance Prices Worldwide — remittanceprices.worldbank.org

- Wise.com — Live transfer calculator and fee schedule, verified June 2026

- Remitly.com — Live transfer calculator and fee schedule, verified June 2026

- Bank of Canada — Exchange rate data for CAD currency pairs, June 2026

- Trustpilot — Wise (4.3/5, 200,000+ reviews) and Remitly (4.2/5, 40,000+ reviews), verified June 2026

- Apple App Store — Wise (4.7/5) and Remitly (4.9/5) ratings, verified June 2026

- Statistics Canada — Immigration and newcomer population statistics, 2024–2026

- Financial Consumer Agency of Canada (FCAC) — International money transfer guidance for consumers

- OFX.com — Large transfer comparison rates, verified June 2026

About the Author

Talal Eddaouahiri is the Founder and Editor-in-Chief of MoneyAbroadGuide.com. A Moroccan immigrant with over 15 years of experience in international banking, Talal built MoneyAbroadGuide to provide the honest, research-backed financial guidance he wished he had when he first arrived in North America. He helps immigrants, expats, newcomers, international students, and foreign workers navigate banking, credit building, money transfers, taxes, and personal finance in the USA and Canada. His writing is based on personal experience, primary research, and consultation with financial professionals across both countries.

Disclaimer

MoneyAbroadGuide.com may earn affiliate commissions when you open accounts through links on this page. This does not affect our editorial independence or the accuracy of our comparisons. We only recommend services we have personally researched and that we believe provide genuine value to our readers. All rates, fees, and figures quoted in this article are illustrative based on market conditions in June 2026 and are subject to change. Always verify current rates directly with the service provider before sending money.

Written by Talal Eddaouahiri

Founder & Editor-in-Chief | Former International Banking Executive

Talal is a Moroccan immigrant to the USA with 15+ years of experience in international banking. He founded MoneyAbroadGuide to help newcomers navigate the financial complexities of moving abroad.