⚠️ Disclaimer: This article is for educational purposes only and is not financial, tax, or legal advice. Exchange rates, fees, processing times, and tax thresholds change frequently and vary by provider, payment method, and individual circumstances. Always verify current rates and terms directly with the provider, and consult a licensed financial advisor, accountant, or cross-border tax professional before making decisions based on this information.

📋 Table of Contents

- Introduction

- Why This Matters for USA Residents

- Top Services Compared

- Quick Comparison: Which Service Is Best For You?

- Detailed Review: Wise

- Detailed Review: Remitly

- Detailed Review: OFX vs Western Union

- Understanding Fees and Exchange Rates

- Complete Fee Breakdown

- Transfer Speed

- Real-World Case Studies

- Regulations and Legal Requirements

- Safety, Security and Fraud Protection

- Special Situations

- Step-by-Step Guide: How to Make Your First Transfer

- Expert Money-Saving Tips

- Common Mistakes to Avoid

- Our Top Picks

- Pre-Transfer Checklist

- Build Your Financial Foundation

- Frequently Asked Questions (FAQ)

- Conclusion

- Sources

Introduction

Sending money across international borders has never been more important — or more complex — than it is in 2026. For millions of Americans who regularly transfer funds to Canada, whether to support family members, pay for property, cover tuition fees, or manage business expenses, finding an efficient, affordable, and reliable method is a financial priority that can genuinely make a difference to a monthly budget. The volume of money flowing between the United States and Canada each year runs into the tens of billions of dollars, making this one of the most active cross-border financial corridors in the world. Yet despite the geographic proximity and close economic ties between these two nations, many Americans still overpay on fees and receive weaker exchange rates simply because they haven’t compared their options.

The landscape of international money transfers has evolved quickly over the past several years, and 2026 represents a dynamic moment in that evolution. Digital-first fintech companies have matured into regulated, trusted platforms that now compete head-to-head with — and in many cases outperform — traditional banks on cost and convenience. At the same time, regulatory frameworks in both the United States and Canada have adapted to these new players, giving consumers stronger protections and more transparency than before. Navigating this landscape effectively means knowing not just which services exist, but how they compare on the metrics that matter most: exchange rate margins, fees, transfer speed, security, and customer support.

This article is written for residents of the United States who need to send money to Canada. Whether you are a first-generation immigrant sending remittances back to family in Toronto or Vancouver, an American entrepreneur paying Canadian contractors or suppliers, a student covering tuition at a Canadian university, a retiree managing a cross-border investment property, or simply someone helping a loved one through a financial emergency, the guidance in this piece is meant for your situation. We’ll walk through several of the leading services available today, compare them on the dimensions that matter most, and give you a framework for choosing the right option for your specific transfer.

Not all transfers are created equal. A $200 emergency payment to a family member in Montreal has very different requirements than a $50,000 real estate deposit being sent to a notary in Calgary. Speed, cost, and convenience trade off against each other depending on your circumstances. In 2026, Americans have more solid options than ever — the challenge is knowing how to choose between them. By the end of this article, you should have a clear framework for comparing providers, understanding the true cost of a transfer, and avoiding the most common and costly mistakes.

📘 FREE RESOURCE FOR NEWCOMERS

How to Build Your Credit Score in the USA (2026 Guide)

New to the USA? Your credit score is the foundation of your financial life here — it affects renting, car loans, credit cards, and more. This step-by-step guide explains exactly how the US credit system works and how to build a strong score fast.

Why This Matters for USA Residents

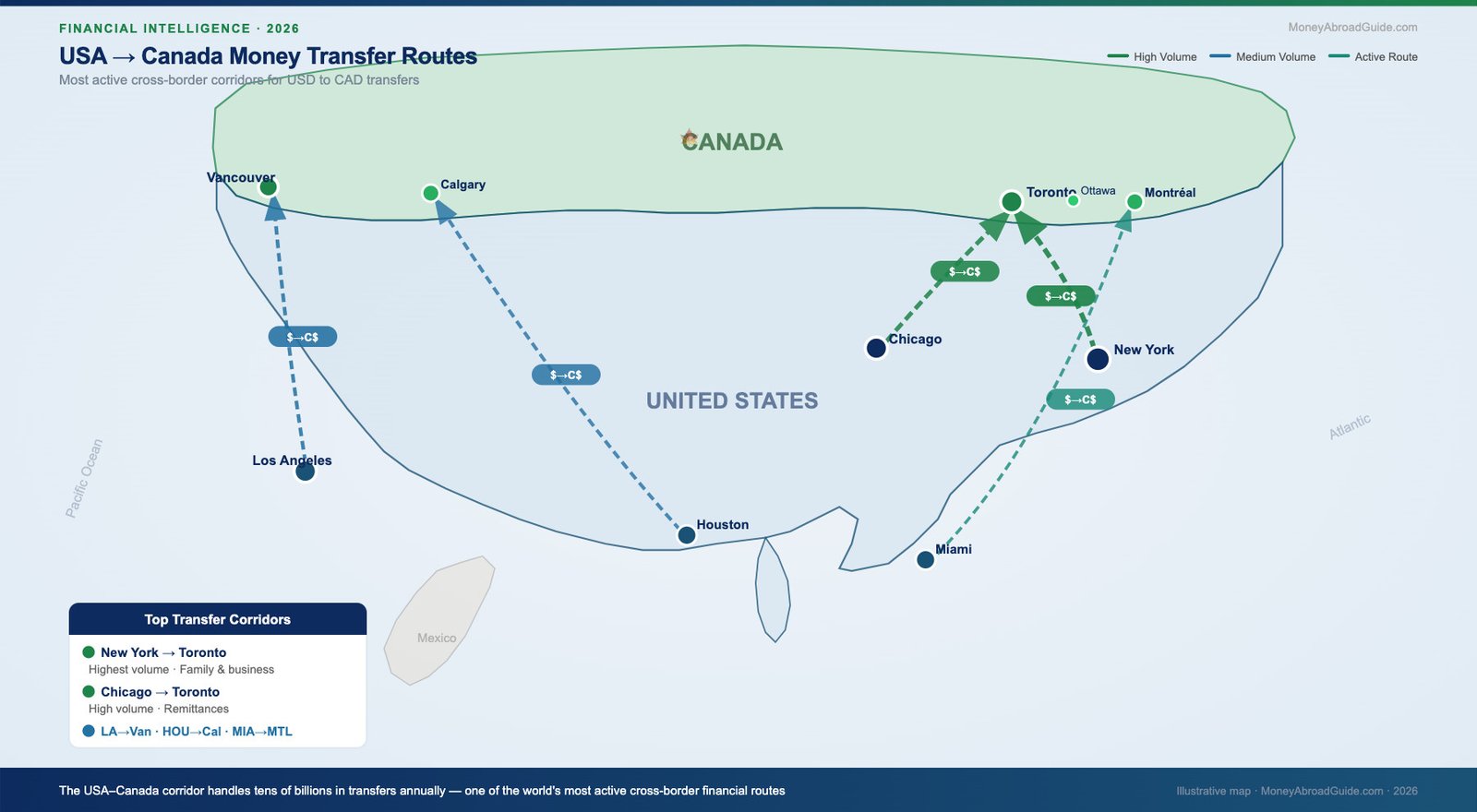

The United States and Canada share the longest undefended border in the world, and the financial ties between the two countries are just as extensive as the geographic ones. There are roughly a million Americans living in Canada and an even larger number of Canadians living in the United States, creating an ongoing need for cross-border money transfers in both directions. For American expats living in Canada, transferring money from U.S. accounts to Canadian ones is often a recurring necessity — covering rent, mortgage payments, utility bills, and everyday living expenses. For Americans still living stateside who have family members, dependents, or financial obligations in Canada, the same need exists with equal urgency. Every dollar lost to avoidable fees or a weak exchange rate is a dollar that could have gone toward something more meaningful. If you’re newly settling in the USA and still setting up your banking, our guide to the best banks for newcomers to the USA can help you choose an account that makes cross-border transfers easier and cheaper from day one. You may also find our Newcomers to USA Hub helpful as a starting point.

Beyond personal remittances, the business dimension of USA-to-Canada money transfers is significant and growing. The two countries are major trading partners, and small and medium-sized businesses on both sides of the border routinely pay vendors, contractors, employees, and service providers in the neighboring country. For an American business owner paying a Canadian marketing agency, software developer, or manufacturing partner, the cumulative cost of inefficient transfers can add up to a meaningful sum over a year. With remote work having reshaped the employment landscape, more Americans than ever are working with Canadian talent or for Canadian companies, creating diverse financial flows that benefit from cost-effective transfer solutions. Switching from a traditional bank wire to a modern transfer platform can often represent a noticeable percentage-point savings per transaction — a difference that compounds at scale.

There is also an emotional and social dimension to international money transfers that is easy to overlook when focusing purely on the financial mechanics. For immigrant communities and families spread across borders, money transfers are not just financial transactions — they are expressions of care, responsibility, and connection. When a parent in Chicago sends money to help their adult child through a difficult month in Toronto, the speed and reliability of that transfer matters enormously. When a grandparent in Texas wants to contribute to a grandchild’s registered education savings plan in British Columbia, the ease of that process reflects on the relationship itself. Understanding the best tools available for sending money from the USA to Canada is therefore not just a matter of financial literacy — it’s about being able to show up for the people and obligations that matter most in your life.

Top Services Compared

The table below offers a side-by-side comparison of several leading money transfer services available to Americans sending funds to Canada. Each service is compared on its general fee structure, typical transfer speed, exchange rate approach, and an overall rating based on a combination of user experience, regulatory standing, customer support quality, and value for money. All figures below are approximate, point-in-time estimates based on a benchmark transfer of $1,000 USD to CAD for a standard bank deposit — exchange rates and fees change continuously, so always confirm the live quote on the provider’s site or app before sending. For a deeper dive into fees across services, see our guide to best international money transfer apps.

| Service | Typical Fees (Estimate) | Typical Speed | Exchange Rate Approach | Rating |

|---|---|---|---|---|

| Wise | Low flat fee + ~0.4% conversion fee | Instant to 1 business day | Mid-market rate (no markup) | ⭐⭐⭐⭐⭐ (5/5) |

| Remitly | ~$0–$4 (Economy); ~$3–$5 (Express) | Minutes (Express) or 3–5 days (Economy) | Small markup (~0.5–1.5% over mid-market) | ⭐⭐⭐⭐½ (4.5/5) |

| OFX | No transfer fee on most transfers | 1–2 business days | Competitive margin (~0.5–1%); strong for large amounts | ⭐⭐⭐⭐½ (4.5/5) |

| XE Money Transfer | No flat fee; built into exchange rate | 1–3 business days | Small markup (~0.5–2%, varies by amount) | ⭐⭐⭐⭐ (4/5) |

| Western Union | ~$0–$10 depending on method and speed | Minutes to 1–3 business days | Below mid-market (often 1.5–3% markup) | ⭐⭐⭐½ (3.5/5) |

| MoneyGram | ~$2–$9 depending on method | Minutes to 3 business days | Below mid-market (often 1.5–2.5% markup) | ⭐⭐⭐½ (3.5/5) |

| WorldRemit | ~$2–$4 flat fee | Minutes to 1 business day | Moderate markup (~1–2% over mid-market) | ⭐⭐⭐⭐ (4/5) |

| TransferGo | Low fees; free on select plans | Same day to 1–2 business days | Competitive; small markup (~0.5–1.5%) | ⭐⭐⭐⭐ (4/5) |

Note: Fees, exchange rates, and ratings shift in real time and vary by payment method, transfer amount, destination province, and ongoing promotions. Treat the figures above as approximate guidance, not guaranteed pricing — always check the provider’s live quote before confirming a transfer.

Which Service Is Best For You? Quick Comparison

If you only have a minute, this table gives you a quick recommendation based on what matters most for your transfer. Use it as a starting point, then read the detailed reviews below for the full picture.

| If your priority is… | Best Choice | Why |

|---|---|---|

| Best overall exchange rate for everyday transfers | Wise | Uses the mid-market rate with a low, transparent fee — generally the strongest value for most senders. |

| Urgent transfer, money needed within minutes | Remitly (Express) | Express delivery can land funds in a Canadian bank account quickly, at a modest premium over Economy. |

| Large transfers (~$5,000+) | OFX | No flat transfer fee on most transactions, competitive margins on bigger amounts, and access to a currency specialist. |

| Recipient needs cash pickup, no bank account | Western Union | Large agent network across Canada for cash pickup, useful when the recipient is unbanked or needs cash quickly. |

| Specific situations (certain business wires) | Bank Wire | Convenient if already integrated with your existing accounts, but usually the most expensive option — generally a last resort. |

Looking at the data in these comparison tables, a general pattern emerges — though the “best” choice will always depend on your individual priorities. Wise tends to lead the rankings for most everyday users because it offers the mid-market exchange rate with no hidden markup, which has the greatest long-term financial impact. When you transfer $1,000 USD to Canada using a service that applies a 2% exchange rate margin versus one close to the mid-market rate, you are effectively losing around $20 on a single transaction — and that adds up quickly if you transfer regularly. OFX is a particularly strong competitor for larger transfers, where its no-flat-fee structure and dedicated support can provide a compelling alternative, especially for transfers above roughly $5,000. For a full head-to-head, see our Wise vs Remitly comparison and Wise vs OFX comparison.

Detailed Review: Wise

Wise (formerly TransferWise) has built a strong reputation as one of the more transparent and cost-effective ways to send money from the USA to Canada, and heading into 2026, it remains a top choice for Americans who prioritize fair exchange rates and clear pricing. What sets Wise apart from traditional banks and many competitors is its use of the mid-market exchange rate — the real rate you’d see on Google — with no hidden markup baked into the conversion. The rate you’re quoted is genuinely close to the market rate, and the fees are itemized before you confirm your transfer.

Wise — Key Benefits

- Mid-market exchange rate: No hidden markup — you see exactly what you pay and what your recipient gets.

- Fast delivery: Many USD-to-CAD transfers arrive within hours to one business day when funded by debit card or ACH.

- Multi-currency account: Hold and convert CAD and USD in one account — useful for frequent cross-border senders.

- Transparent fees: Fees are itemized before confirmation; no surprises.

- Regulated and licensed: Registered with FinCEN as a Money Services Business across the US.

- Highly rated app: Available on iOS and Android with real-time tracking.

Wise — Limitations

- No cash pickup option — recipient must have a Canadian bank account.

- Credit card funding carries higher fees and isn’t recommended for regular transfers.

- For very large transfers ($50,000+), specialist brokers like OFX may offer more personalized service.

Wise — Best Use Case

Wise is the ideal choice for everyday senders who want the best possible exchange rate and don’t need cash pickup. Whether you’re sending $500 to help a family member or $10,000 for a property-related expense, Wise delivers strong value across most amounts.

💱 Ready to Send with Wise?

Check the live USD→CAD rate right now — no obligation, no signup required to see the quote.

Check Today’s Wise Exchange Rate →See our full Wise vs Remitly comparison and Wise vs OFX comparison for a head-to-head breakdown.

Detailed Review: Remitly

Remitly is another major player in the international money transfer space, and it has built a loyal user base among Americans sending money to family members in Canada. While Remitly originally gained prominence for remittances to developing markets, its USA-to-Canada corridor has become increasingly competitive. The platform’s core appeal is its two-tier pricing model — Economy and Express — which gives senders direct control over the trade-off between speed and cost.

Remitly — Key Benefits

- First-transfer promotions: New users frequently receive reduced fees or improved exchange rates on their first transfer — ideal for larger initial sends.

- Two-speed delivery: Economy (3–5 business days, lower cost) and Express (minutes to hours, higher cost) — you choose your priority.

- 24/7 customer support: Available via chat and phone around the clock.

- Highly rated mobile app: Consistently praised for its design and ease of use.

- Bank deposits and debit card delivery: Flexible delivery options to Canadian bank accounts.

Remitly — Limitations

- Exchange rate markup (~0.5–1.5%) is slightly wider than Wise, making it a little less competitive on pure rate.

- Transfer limits for new, unverified accounts can be restrictive until additional identity verification is completed.

- Economy tier can experience occasional delays during high-volume periods.

Remitly — Best Use Case

Remitly shines for families who send money regularly and value speed, customer support accessibility, and a smooth mobile experience. Its Express option is a top pick for urgent transfers where funds need to arrive in minutes.

Remitly — Fees and Overall Cost

Remitly’s pricing is competitive but varies by amount, payment method, and Economy vs Express. For a $1,000 transfer, Economy tier fees might range roughly from $0 to $4, plus a modest exchange rate margin. Express transfers carry higher fees but deliver faster. For families who can plan ahead, Economy generally offers solid value. For urgent transfers, Express is still typically far cheaper than a traditional bank wire ($25–$45 flat plus a weaker rate).

🚀 New to Remitly?

First-time users often qualify for a promotional rate or reduced fee. Check what offer is available right now.

Get Remitly’s First Transfer Offer →For a full rate comparison, see our Wise vs Remitly guide.

Detailed Review: OFX vs Western Union

OFX and Western Union serve fundamentally different types of senders. OFX is a specialist currency exchange platform built for larger transfers, typically starting around $1,000 USD, and it tends to shine for significant sums — think property purchases, business payments, or large personal transfers. OFX charges no transfer fee on most transactions and provides access to currency specialists who can help with rate alerts or timing. For Americans transferring roughly $5,000 or more to Canada, OFX’s combination of competitive rates and personalized service is often compelling.

OFX — Key Benefits

- No transfer fee on most transactions — OFX makes its margin on the exchange rate spread, keeping the process simple.

- Currency specialists: Dedicated support for large or complex transfers, including rate alerts and forward contracts.

- Competitive for large amounts: The larger the transfer, the more OFX’s margin advantage over banks stands out.

- Regulated and trusted: Holds licenses across the US and operates in all major markets.

- Business accounts: OFX Business offers multi-currency wallets, batch payments, and compliance tooling.

OFX — Best Use Case

OFX is the go-to for anyone moving $5,000 or more — whether for property, business payroll, large personal transfers, or repatriating income. The combination of no flat fees and currency specialist access provides real value at scale.

💼 Moving a Large Amount to Canada?

OFX charges no transfer fee on most transactions and offers access to currency specialists. Open a free account in minutes.

Open a Free OFX Account →Western Union, by contrast, is the go-to option when speed, accessibility, and cash pickup are the priorities. With thousands of agent locations across both the USA and Canada, Western Union remains a strong choice for situations where the recipient doesn’t have a bank account or needs cash in hand quickly. Transfers can be completed in minutes, and the platform supports a wide range of payment and delivery methods. This convenience comes at a cost — Western Union’s exchange rates are typically less favorable than OFX or Wise, and fees can be higher for smaller amounts. For emergencies or one-off situations where cash delivery is essential, Western Union is hard to replace, but for regular transfers where value matters, it’s rarely the most economical choice.

For a closer side-by-side on the mid-market leader versus the large-transfer specialist, see our Wise vs OFX comparison, where we break down fees, exchange rates, and ideal use cases in more depth.

Understanding Fees and Exchange Rates

When sending money from the USA to Canada, the difference between a smart transfer and a costly one often comes down to two interconnected factors: the fee charged upfront and the exchange rate applied behind the scenes. Many people focus exclusively on the visible transfer fee — the flat charge or percentage shown on the confirmation screen — while overlooking the cost buried in the exchange rate margin. This spread, sometimes called the “markup” or “FX margin,” is the gap between the mid-market rate (the reference rate you’d find on Google or Reuters) and the rate the provider actually offers you. The USD/CAD exchange rate moves throughout each trading day and over time depending on economic conditions and central bank policy, so even a 1% markup on a $5,000 transfer can mean quietly losing roughly $50 before the money reaches your recipient — the exact amount depends on the live rate at the time of transfer.

To put this in concrete terms: if the mid-market USD/CAD rate were around 1.385, a bank might offer a noticeably weaker rate — a spread that could easily be in the 2–4% range. On a $2,500 transfer, a spread like that could cost on the order of $50–$100 in hidden cost, even if the bank advertises “no transfer fee” on international wires. A dedicated transfer service like Wise typically offers a rate much closer to the mid-market rate with a small, transparent fee, which can mean meaningful savings on the same transaction. This is why reading the fine print on exchange rates is just as important — often more important — than comparing headline transfer fees. Always treat any specific dollar figures in this article as illustrative estimates, not guarantees, since live rates change continuously. For more, see our full guide to best international money transfer apps.

Competitive pressure has pushed many providers to reduce or eliminate flat transfer fees, especially on high-volume corridors like USD-to-CAD. Services such as Remitly, OFX, and XE Money Transfer have all responded by tightening their margins on popular routes. However, “no fee” rarely means “no cost” — providers that waive transfer fees often compensate with a wider exchange rate spread. For example, a “zero-fee” promotion from a provider with a weaker exchange rate could still cost more overall than a fee-charging competitor offering a tighter spread. Always compare the total cost: fee plus the rate you’re actually getting.

Exchange rates are not static — they shift throughout the trading day, and the rate you’re quoted in the morning may differ from what you see later. Some providers allow you to lock in a rate for a set period, which can be valuable when the Canadian dollar is experiencing volatility tied to oil prices or Bank of Canada policy announcements. For regular senders — Americans who have family in Canada, pay Canadian contractors, or manage cross-border business expenses — understanding how to time transfers and compare the all-in cost (fee plus exchange rate impact) can realistically add up to meaningful savings over a year.

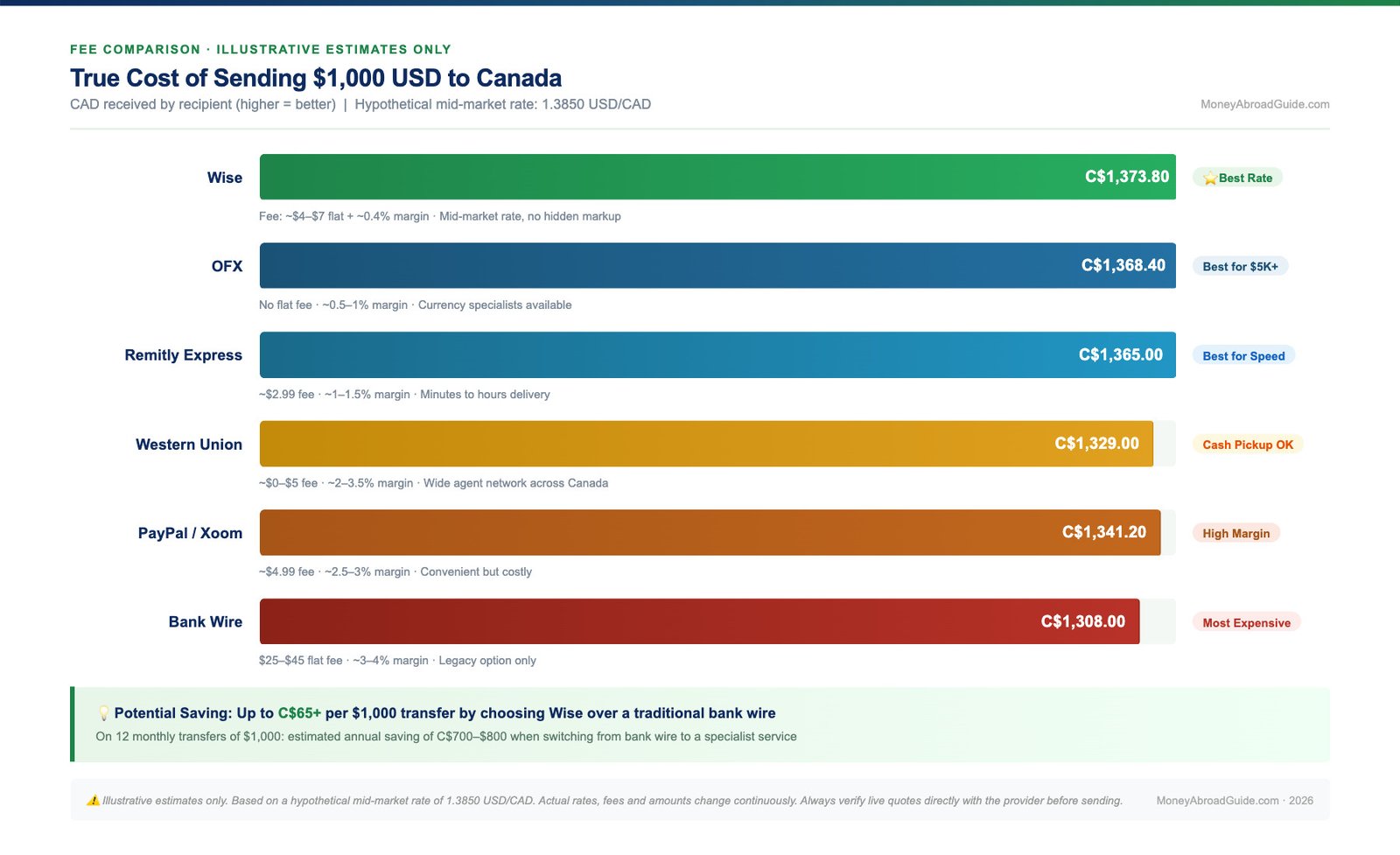

Complete Fee Breakdown: Illustrative Transfer Examples

The table below is an illustrative example of how different providers might compare on a hypothetical mid-market USD/CAD rate of 1.3850. These numbers are for illustration only — the live rate and fees on the day you transfer will differ, so always check the provider’s real-time quote before sending.

| Provider | $500 USD | $1,000 USD | $2,500 USD | $5,000 USD | $10,000 USD | Est. Total Cost* |

|---|---|---|---|---|---|---|

| Wise ⭐ Best | C$685.20 | C$1,373.80 | C$3,444.10 | C$6,893.50 | C$13,801.00 | ~0.4%–0.7% + flat fee (~$4–$12) |

| OFX | C$679.50 | C$1,368.40 | C$3,436.20 | C$6,885.00 | C$13,812.00 | No flat fee; ~0.5%–1% margin |

| Remitly (Express) | C$681.10 | C$1,365.00 | C$3,421.50 | C$6,867.00 | C$13,754.00 | ~$2.99 fee + ~1%–1.5% margin |

| PayPal / Xoom | C$668.40 | C$1,341.20 | C$3,356.00 | C$6,715.00 | C$13,440.00 | ~$4.99 fee + ~2.5%–3% margin |

| Bank Wire (e.g., Chase) | C$651.00 | C$1,308.00 | C$3,272.00 | C$6,548.00 | C$13,100.00 | ~$25–$45 flat fee + ~3%–4% margin |

| Western Union | C$662.50 | C$1,329.00 | C$3,325.00 | C$6,654.00 | C$13,318.00 | ~$0–$5 fee (promo) + ~2%–3.5% margin |

*Illustrative estimates only, based on a hypothetical mid-market rate of 1.3850 USD/CAD. Actual rates and fees vary continuously. Always verify the live rate and fee before confirming any transfer.

Transfer Speed

Transfer speed is one of the more competitive areas among providers serving the USA-to-Canada corridor, and the options available today are considerably faster than what existed just a few years ago. The expansion of real-time payment infrastructure on both sides of the border — including faster payment rails in the US and Interac e-Transfer’s continued use in Canada — has made near-instant transfers increasingly common for many providers. Wise, for example, completes many USD-to-CAD transfers within minutes when funded by debit card, with funds often arriving in the recipient’s Canadian bank account quickly. Remitly’s Express service similarly aims for delivery within minutes for card-funded transfers, making it a strong choice when speed is the primary concern — such as emergency family transfers or time-sensitive bill payments.

Speed almost always comes at a cost, and understanding the speed-cost tradeoff is useful for choosing the right option. Instant or same-day transfers funded by credit or debit card typically carry higher fees or slightly wider exchange rate margins compared with transfers funded by ACH bank transfer (also called e-check or direct debit). For example, Remitly’s Express service generally costs more than its Economy option, which delivers funds in roughly 3 to 5 business days but can offer a somewhat better exchange rate. Wise similarly tends to charge more for card-funded transfers, while ACH-funded transfers take roughly 1 to 3 business days but typically come with lower costs. For senders who can plan ahead, the slower, bank-funded option is often the better financial choice.

For those weighing speed versus savings, a practical approach is: if the transfer is not time-sensitive, fund via ACH bank transfer and allow a few business days for delivery — this tends to produce the best exchange rates and lowest total costs across most providers. If speed is essential, Wise and Remitly Express tend to offer some of the fastest card-funded options. OFX, while not offering instant transfers, has built a reputation for reliable delivery on USD-to-CAD transfers with good rate transparency — useful for regular senders who value consistency over raw speed.

💡 BUILDING YOUR USA FINANCIAL PROFILE?

Saving on money transfers is just one piece of the puzzle. Your US credit score determines your rates on everything from car insurance to mortgages.

Our free 2026 guide covers: how US credit scoring works, the fastest ways to build credit from scratch, secured cards vs. credit-builder loans, and common mistakes newcomers make.

Real-World Case Studies (Illustrative Examples)

Note: The case studies below are illustrative examples based on realistic sender profiles and publicly available provider pricing as of 2026. Names and details are fictional and used for educational purposes only. Individual results will vary based on live rates, payment method, and personal circumstances.

📋 Case Study #1 — Ahmed, Chicago, Illinois

Profile: Ahmed is a software engineer who moved from Morocco to Chicago four years ago. His parents live in Toronto, Ontario, and he sends approximately $1,000/month to help cover their living expenses. He had been using a Chase international wire for the past two years — primarily out of habit and convenience.

Previous method — Bank Wire (Chase): Ahmed was paying approximately $35 per wire fee, plus the bank’s exchange rate markup of roughly 3–3.5% over the mid-market rate. On a $1,000 transfer, this meant his parents were receiving approximately C$1,300–C$1,308 instead of the roughly C$1,374 they’d receive at the mid-market rate. His estimated monthly “overpay” was in the range of $60–$80 per transfer when both the fee and the rate margin were included.

Switch to Wise: After comparing providers, Ahmed switched to Wise. Using Wise’s ACH bank transfer option, he pays a small fee (approximately $4–$7 on a $1,000 transfer) and receives a rate close to the mid-market rate. His parents now receive approximately C$1,365–C$1,374 per transfer.

Illustrative annual savings: At roughly $65 saved per month (fee savings + rate improvement combined), Ahmed’s estimated annual saving from switching is in the range of $700–$800 per year — money his parents receive in full rather than going to bank revenue. Actual savings will depend on live rates at time of transfer.

Ahmed’s takeaway: “I had no idea the exchange rate margin was costing me so much. The fee was visible, but the rate difference was invisible until I compared side by side.”

📋 Case Study #2 — Maria, International Student, Texas → Ontario

Profile: Maria is a 22-year-old international student from Mexico attending the University of Waterloo in Ontario. Her family sends her tuition and living expenses from their US bank account in Austin, Texas — approximately $8,500 per semester for tuition, plus $600–$800/month for living costs.

Tuition payment challenge: Maria’s family initially tried to pay her university tuition via a US bank wire, which charged a $45 flat fee and a 3.2% FX margin. On an $8,500 tuition transfer, the all-in cost in exchange rate loss alone was approximately $272, plus the $45 wire fee — a total “transfer tax” of roughly $317 on a single payment.

Switch to OFX: After speaking with a friend who had done cross-border payments before, Maria’s family tried OFX. For their $8,500 tuition transfer, OFX charged no flat fee and offered an exchange rate margin of approximately 0.8% — totaling an estimated cost of roughly $68. Compared to the bank wire, the family saved approximately $249 on a single tuition payment.

For monthly living expenses: Maria uses Remitly’s Economy option for the smaller monthly transfers, where the lower fees and 3–5 day delivery work well since her family sends money at the start of each month. Promotional first-transfer rates reduced the effective cost even further on her initial setup.

Maria’s takeaway: “Switching services for tuition payments felt like a small hassle but saved my family hundreds of dollars per semester. Over a 4-year degree, that compounds significantly.”

Regulations and Legal Requirements

United States: FinCEN, FBAR, and the $10,000 Threshold

There is no federal law that caps how much money an individual can send abroad. The $10,000 figure that’s often mentioned in connection with international transfers actually refers to a few distinct rules, and it’s easy to conflate them. Banks and money transfer businesses are required under the Bank Secrecy Act to maintain anti-money-laundering programs and to file reports with the Financial Crimes Enforcement Network (FinCEN) for certain transactions — this is primarily a compliance obligation for the financial institution, not a separate filing you personally need to make just because you sent more than $10,000 in a single transfer.

The threshold that matters most directly to individual senders is the Foreign Bank Account Report (FBAR). If you are a U.S. person — including U.S. citizens and resident aliens — with a financial interest in, or signature authority over, one or more foreign financial accounts (including Canadian bank accounts) whose combined value exceeded $10,000 at any point during the calendar year, you are generally required to file FinCEN Form 114 (the FBAR) by April 15, with an automatic extension to October 15. This is based on your foreign account balances over the year, not on the size of any one transfer you make. Penalties for failing to file when required can be substantial, so if you maintain a bank account in Canada, it’s worth confirming your filing obligations with a cross-border tax professional. For newcomers to Canada managing finances in both countries, our Newcomers to Canada Hub has additional guidance.

Canada: CRA, FATCA, and Incoming Funds

On the Canadian side, the Canada Revenue Agency (CRA) has its own rules governing incoming international funds. Money received as a personal gift or family support is generally not considered taxable income in Canada, but if the transferred funds later generate investment income — such as interest or dividends — that income generally needs to be reported on a Canadian tax return. The CRA also has data-sharing arrangements with the IRS under the Foreign Account Tax Compliance Act (FATCA), meaning Canadian financial institutions report accounts held by U.S. persons to the CRA, which shares relevant information with the IRS. Both senders and recipients should keep accurate records of significant cross-border transfers.

FINTRAC and Cross-Border Electronic Transfers Into Canada

FINTRAC (the Financial Transactions and Reports Analysis Centre of Canada) is the agency responsible for receiving and analyzing reports related to money laundering and terrorist financing. For international electronic funds transfers, Canadian banks, money services businesses, and certain other reporting entities are required to submit an Electronic Funds Transfer Report (EFTR) to FINTRAC when they send or receive an international electronic funds transfer of CAD $10,000 or more in a single transaction on behalf of a client. This obligation falls on the bank or money services business handling the transfer, not on you as the sender or recipient. Reputable providers handle this automatically.

What This Means for Everyday Senders

For most people, compliance is simple: keep basic records of larger transfers (date, amount, recipient, and purpose), understand whether you need to file an FBAR based on your foreign account balances over the year (not based on individual transfer amounts), and consult a cross-border tax professional if you’re making large, frequent, or business-related transfers. See the Sources section at the end of this article for links to the official FinCEN, FBAR, and FINTRAC pages. If you’re also navigating banking as a newcomer to the USA, see our guide to US bank accounts for non-residents.

Safety, Security and Fraud Protection

Deposit Insurance and Fund Safety

When sending money internationally, the safety of your funds matters as much as the exchange rate or fee. In the United States, deposits held at federally insured banks are protected by the Federal Deposit Insurance Corporation (FDIC), generally up to $250,000 per depositor, per institution, per ownership category. In Canada, the Canada Deposit Insurance Corporation (CDIC) provides broadly similar protection for eligible deposits at member institutions. These protections apply to bank deposits — they generally do not extend to funds held briefly in transit with a money transfer operator. This is why choosing a provider that is properly licensed, regulated, and financially sound matters. Providers such as Wise and OFX are required to safeguard customer funds (for example, by holding them in segregated accounts, separate from the company’s own operating capital), which is a meaningful safeguard if a provider were ever to run into financial difficulty.

Account Security Best Practices

Two-factor authentication (2FA) is the baseline security standard for legitimate money transfer platforms. When logging in or authorizing a transfer, 2FA requires a second verification step — typically a one-time code sent to your phone or generated by an authentication app — which significantly reduces the risk of unauthorized access even if your password is compromised. Many platforms also use device recognition and behavioral monitoring to flag unusual login patterns. Senders should enable every available security feature, use unique and strong passwords, and avoid initiating transfers over public Wi-Fi, which remains a common vector for credential theft.

Common Scams to Watch For

Fraud targeting international money transfers is unfortunately common, and USA-to-Canada corridors are no exception. Frequent schemes include romance scams, where fraudsters build fake online relationships before requesting urgent transfers; emergency impersonation scams, where criminals pose as a relative in distress; and overpayment scams, where a fake buyer sends a fraudulent check and asks the victim to wire back the difference. International transfers are particularly difficult to reverse once sent. To protect yourself: never send money to someone you haven’t met in person, verify recipient details through a separate, trusted contact method, and be skeptical of any request that creates artificial urgency. Legitimate organizations will not demand payment exclusively via wire transfer or money transfer apps.

Special Situations: Large Transfers, Business, and Emergencies

Large Transfers

Transfers that are large relative to your typical activity — often informally thought of as amounts above roughly $10,000 USD — usually involve additional planning and documentation. Banks and transfer services may ask for documentation explaining the source of funds and the purpose of the transfer, particularly for larger amounts. Common documentation includes property sale records, inheritance letters, investment statements, or business contracts. For larger transfers, a specialist foreign exchange broker such as OFX can offer more competitive rates than a retail bank and assign a dedicated specialist to help with timing and compliance. A forward contract — which locks in today’s exchange rate for a transfer executed at a future date — can help protect larger sums from adverse currency movements while you prepare the transfer.

Business Transfers

Business transfers between the USA and Canada add complexity, including potential GST/HST implications, cross-border payroll considerations, and reporting requirements that can fall under both FATCA and FINTRAC frameworks. U.S. businesses paying Canadian contractors should also be aware of IRS Form 1042-S reporting requirements for payments to foreign persons, where applicable. Business-focused accounts from providers like Wise Business or OFX Business offer multi-currency wallets, batch payments, and compliance tooling built for cross-border commercial transactions. Engaging a cross-border accountant or tax attorney before setting up a regular international payment flow can help avoid costly surprises later.

Emergency Transfers

When money needs to reach Canada within hours rather than days, services offering real-time or same-day delivery — such as Remitly’s Express option, Western Union’s digital service, or certain bank wires — are usually the best fit, for a premium fee. If the recipient doesn’t have ready access to a bank account, Western Union’s agent network allows cash pickup at locations across Canada. In a genuine emergency, prioritize speed over cost, but stay alert — fraudsters often exploit urgency to pressure people into bypassing their own judgment. Always confirm an emergency directly with the recipient through a known, previously verified phone number before sending money, no matter how convincing the request seems.

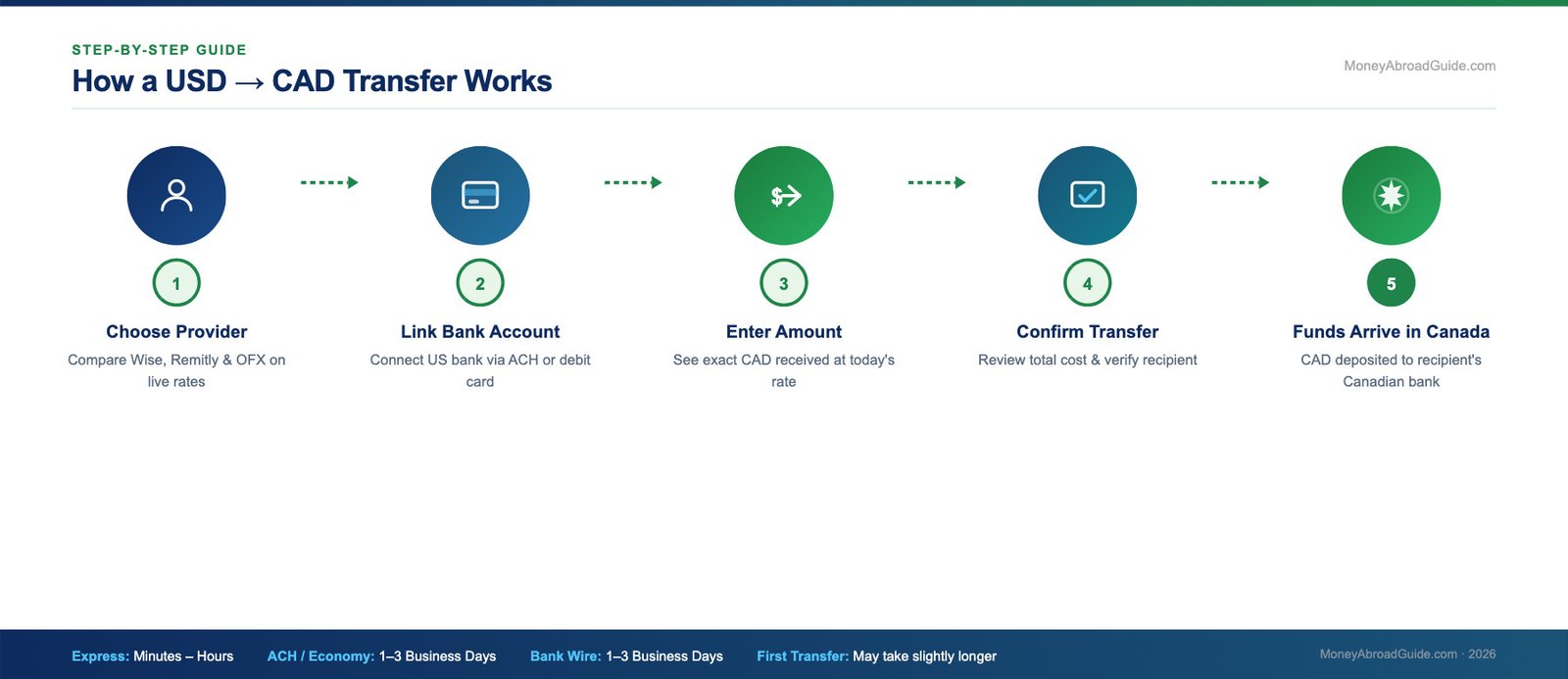

Step-by-Step Guide: How to Make Your First Transfer

Ready to send money from the USA to Canada for the first time? Follow these steps to help your transfer go smoothly, securely, and at a competitive rate.

- Determine how much you need to send. Calculate the amount in USD or CAD. Factor in any fees the recipient might face on their end, and decide whether you care more about sending a round number in USD or ensuring a specific CAD amount arrives. A currency calculator can help you set realistic expectations.

- Compare transfer services. Don’t settle for the first option you find. Compare at least a few providers — Wise, Remitly, OFX, and your bank — and look beyond the advertised exchange rate to the total fees, transfer speed, and reviews. Use our comparison tables above as a starting point, then verify with live quotes. See our best international money transfer apps guide for a broader comparison.

- Create and verify your account. Once you’ve chosen a provider, sign up. Most platforms require your full legal name, address, date of birth, email address, and a government-issued ID such as a passport or driver’s license. Verification can take anywhere from a few minutes to a few hours; larger transfers may require additional documentation.

- Link your payment method. Connect your funding source — a U.S. bank account, debit card, or credit card. Bank transfers (ACH) generally have the lowest fees, while debit and credit cards may process faster but cost more. Double-check that your account details are entered correctly to avoid delays.

- Enter your recipient’s details. Input your recipient’s full name, Canadian bank account number, and the bank’s institution number and transit number. Double-check every digit — incorrect banking details are one of the most common causes of failed or delayed transfers.

- Review the transfer details. Before confirming, check the exchange rate being offered, the total fees, the estimated delivery time, and the CAD amount your recipient will receive. Some providers lock in the exchange rate at this stage, so make sure you’re comfortable with the terms shown.

- Confirm and initiate the transfer. Once satisfied, confirm the transfer. Save your transaction reference number and a screenshot or copy of the confirmation page — you should also receive a confirmation email shortly afterward.

- Track your transfer and notify your recipient. Most providers offer real-time tracking through their app or website. Let your recipient know the money is on its way and roughly when to expect it. First-time transfers can take a little longer due to additional security checks, and subsequent transfers to the same recipient often process faster.

Expert Money-Saving Tips

Sending money internationally doesn’t have to be expensive. With the right habits, you can keep more of your money working for you and your recipient. Here are some practical tips for USD-to-CAD transfers.

- Use a specialist transfer service rather than your bank. Traditional U.S. banks often charge $25–$50 in wire transfer fees on top of exchange rate markups in the range of 2–4%. Specialist services like Wise or OFX can save a meaningful amount over a year, especially for regular senders.

- Monitor exchange rates before you transfer. The USD/CAD exchange rate fluctuates daily, and even small differences can matter on larger transfers. Free tools like Google Finance or XE.com, or your provider’s rate alerts, can help you track movements.

- Set up rate alerts. Instead of checking rates manually, set automatic alerts through your provider or a currency tracking app so you’re notified when the rate hits your target.

- Send larger amounts less frequently when it makes sense. Many providers charge a flat fee per transaction. Consolidating several smaller transfers into one larger transfer can reduce your total fee burden — just balance this against your recipient’s cash-flow needs.

- Use bank transfers instead of cards when possible. Funding via ACH bank transfer is typically cheaper than using a credit or debit card, which can add roughly 1–3% in processing fees.

- Look for promotional offers and first-transfer deals. Many services offer reduced fees or improved exchange rates for new customers, and some have referral bonuses if you’re recommending a service to family members.

- Consider a forward contract for large transfers. If you’re planning a major transfer — for example, a property purchase — a forward contract can let you lock in today’s exchange rate for a transfer that happens later, protecting you from unfavorable rate movements in the meantime.

- Avoid weekend and holiday transfers when timing matters. Some providers process transfers more slowly over weekends and public holidays. Scheduling during regular business days can sometimes result in faster processing.

- Ask about loyalty programs and volume discounts. If you send money regularly, ask your provider whether loyalty discounts or volume-based pricing are available — some specialist providers offer better rates to frequent senders.

- Review your provider periodically. The international money transfer market evolves quickly. A provider that offered the best rates a couple of years ago may not be the most competitive today, so it’s worth comparing providers at least once a year.

Common Mistakes to Avoid

Even experienced senders make costly errors when transferring money internationally. Being aware of these pitfalls in advance can save time, money, and frustration.

- Relying solely on your bank without comparing alternatives. Defaulting to your bank out of habit is one of the more expensive choices, since banks often have some of the weaker exchange rates and higher fees in the market. Compare at least two or three specialist providers before a transfer, regardless of amount.

- Entering incorrect recipient banking details. A single wrong digit in an account or transit number can cause a transfer to fail, be delayed for days, or in rare cases be sent to the wrong account. Always verify recipient details directly with the person receiving the money and double-check every field before confirming.

- Ignoring the exchange rate markup. Many senders focus only on the transfer fee while overlooking the exchange rate margin. A provider advertising “zero fees” may still profit from offering a rate below the mid-market rate. Always calculate the total cost — fee plus exchange rate spread — to understand what you’re actually paying.

- Sending money urgently without planning. Emergency transfers almost always cost more, since express options carry premium fees and urgency can lead to rushed decisions. Plan ahead when possible to give yourself time to compare providers and timing.

- Overlooking potential Canadian tax implications for the recipient. Large transfers to Canada may have reporting implications on the Canadian side, particularly if the recipient needs to declare foreign income or gifts above certain thresholds. Encourage your recipient to consult a Canadian tax professional if they receive significant or recurring transfers.

Our Top Picks for Sending Money from the USA to Canada

After comparing the major providers serving the USA-to-Canada corridor, a few clear patterns emerge for most senders. Wise (formerly TransferWise) is our top overall pick for most senders, offering a rate close to the mid-market exchange rate with transparent, generally low fees that tend to beat traditional banks by a meaningful margin. Whether you’re sending $200 or $20,000, Wise generally combines speed, reliability, and pricing transparency that few competitors match. Its multi-currency account also makes it easy to hold Canadian dollars before sending, giving you flexibility to time transfers when exchange rates are favorable.

For those who prioritize speed above everything else, Remitly is a strong choice, particularly its Express delivery option, which can land funds in a Canadian bank account within minutes. Remitly’s promotional rates for first-time users can be attractive, and its customer support is available around the clock. If you’re a frequent sender who values a smooth mobile experience and fast turnaround, Remitly is worth having on your phone alongside Wise.

For business owners, freelancers, and senders moving larger amounts regularly, OFX offers dedicated support, competitive rates on transfers over roughly $5,000, and no transfer fee on many transactions. These platforms are built for senders who need more than a basic app — rate alerts and forward contracts that help manage currency risk. If you’re managing payroll, paying Canadian contractors, or repatriating business revenue, OFX is worth a closer look.

💼 Best for Large Amounts

OFX

No transfer fee, currency specialists, ideal for $5K+

Open Free OFX Account →Before You Send: Pre-Transfer Checklist

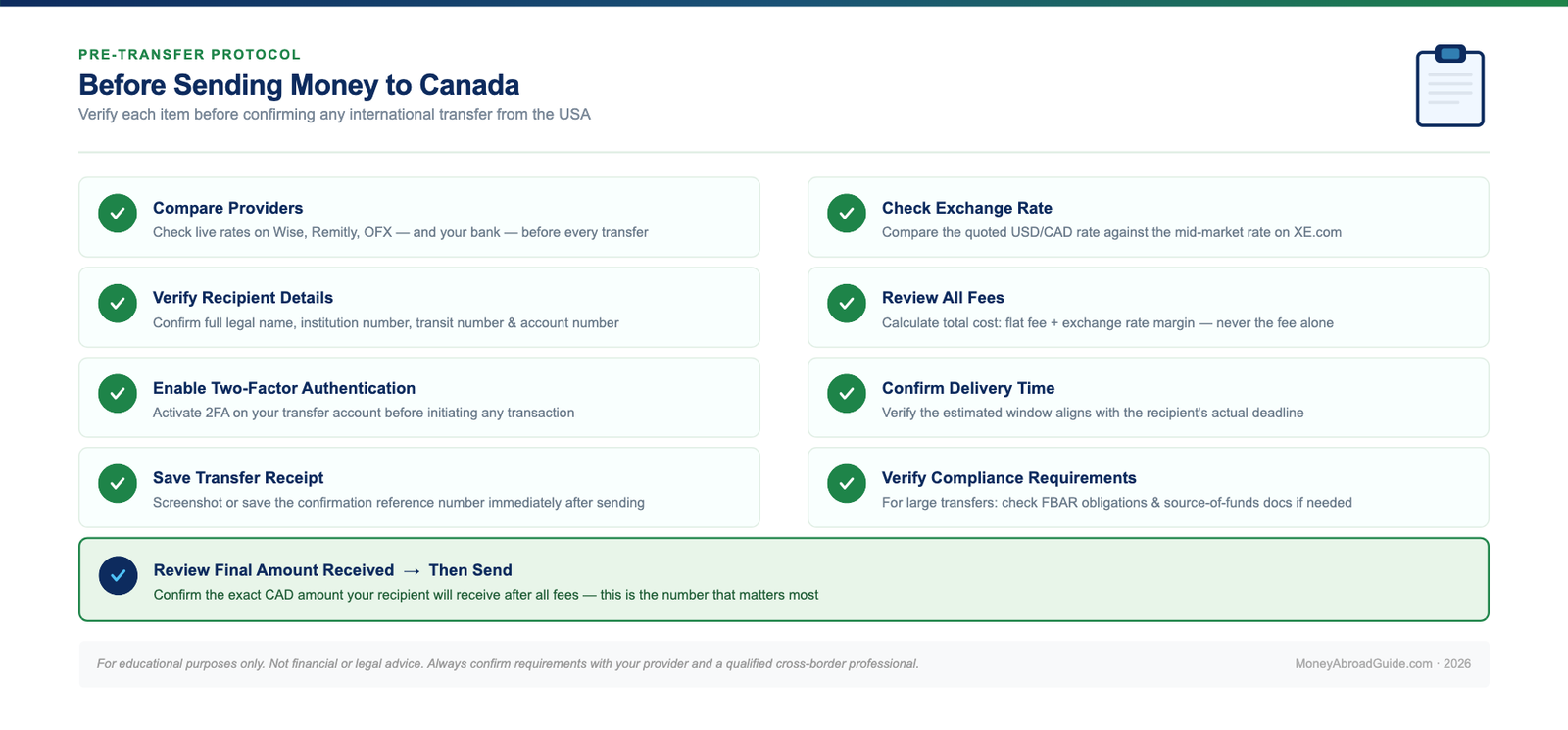

Use this checklist before sending money from the USA to Canada:

- ✅ Compared live rates and fees across at least 2–3 providers (e.g., Wise, Remitly, OFX)

- ✅ Calculated the total cost — flat fee plus exchange rate margin — not just the advertised fee

- ✅ Confirmed the exact CAD amount your recipient will receive at today’s rate

- ✅ Double-checked the recipient’s full legal name, bank name, institution number, and transit number

- ✅ Confirmed the provider is a registered Money Services Business (FinCEN) and works with FINTRAC-regulated partners in Canada

- ✅ Checked the estimated delivery time against your actual deadline

- ✅ Enabled two-factor authentication on your transfer account

- ✅ For larger or recurring transfers, checked whether you may have FBAR or other reporting obligations (see Sources below)

- ✅ Saved the confirmation/reference number for your records

Build Your Financial Foundation in the USA

If you’re a newcomer to the USA — whether you’re an immigrant, an international student, or a visa holder — sending money efficiently across the border is just one piece of building a stable financial life here. Another foundational piece is your US credit score, which affects everything from renting an apartment and getting a car loan to qualifying for a credit card with better rewards and lower interest rates. Many newcomers arrive with an excellent credit history in their home country, only to discover that it doesn’t transfer to the USA — meaning they effectively start from zero.

To help with exactly this, we created “How to Build Your Credit Score in the USA (2026)”, a practical, step-by-step guide written specifically for immigrants, expats, international students, and visa holders. It covers how U.S. credit scoring actually works, how to open your first accounts, practical strategies to build a strong score quickly, and common mistakes that hold newcomers back. You may also want to explore our guide to US bank accounts for non-residents and our full Newcomers to USA Hub for a complete picture of getting financially established in America.

Frequently Asked Questions (FAQ)

How much does it cost to send money from the USA to Canada?

Costs vary widely by provider and change continuously. Traditional banks often charge roughly $25–$45 in wire transfer fees, plus a hidden markup on the exchange rate that can add another 2–4% to the total cost. Specialist transfer services like Wise typically charge a small, transparent fee (often in the 0.4–1.5% range depending on the amount) and use a rate close to the mid-market rate, which is usually significantly cheaper overall. Remitly’s cost depends on delivery speed — Economy is generally cheaper, while Express carries a higher fee. For a $1,000 transfer, the all-in cost could realistically range from a few dollars with a specialist service to $50 or more with a traditional bank — but always check the live quote, since these figures are estimates and change over time.

Is it safe to send money from the USA to Canada through online transfer services?

Reputable online money transfer services are generally considered safe and are regulated by financial authorities in both countries. In the United States, platforms like Wise, Remitly, OFX, and PayPal are registered as Money Services Businesses (MSBs) with FinCEN and hold the state licenses required to operate. They typically use strong encryption, two-factor authentication, and fraud detection systems, and often hold customer funds in segregated accounts, separate from the company’s own operating funds. The key is to stick with well-established, regulated platforms and avoid any service that isn’t transparent about its licensing and regulatory status — never send money through unofficial channels or platforms that can’t verify their credentials.

How long does an international transfer from the USA to Canada take?

Transfer times vary by platform and delivery method. Wise transfers often arrive within 1–2 business days, and sometimes within hours for smaller amounts funded by debit card. Remitly’s Express option can deliver funds within minutes to a Canadian bank account, while its Economy option typically takes 3–5 business days at a lower cost. OFX typically processes transfers within 1–2 business days. Traditional bank wires generally take 1–3 business days but can occasionally take longer due to intermediary bank delays. Weekends, Canadian public holidays, large amounts that trigger extra verification, and first-time transfers can all add time.

Are there limits on how much money I can send from the USA to Canada?

Transfer limits vary by platform and by your verification level — fully verified accounts generally have higher limits. Some platforms allow very large verified transfers (potentially into six figures or more), though daily and monthly limits also apply. Newer or unverified accounts often start with lower daily limits that increase as you complete identity verification. Specialists like OFX and Currencies Direct are built to handle large transfers with proper documentation. From a regulatory standpoint, there’s no legal cap on how much you personally can send internationally from the USA — but larger or unusual transactions can trigger additional verification or institutional reporting, which is routine and not a cause for concern for legitimate senders.

Do I need to pay taxes when sending money from the USA to Canada?

Whether you owe tax depends on the nature of the money, not the act of transferring it. Simply moving money you already own from a US account to a Canadian account is generally not a taxable event. If you’re sending a gift to an individual that exceeds the annual gift tax exclusion — $19,000 per recipient for 2026 — you may need to file IRS Form 709 (Gift Tax Return), though you likely won’t owe actual gift tax unless your lifetime exemption is exhausted. If you’re sending money that represents income, that income should already be reported on your US tax return regardless of where it’s sent. U.S. persons with foreign financial accounts exceeding $10,000 in aggregate at any point during the year generally need to file an FBAR (FinCEN Form 114). Always consult a cross-border tax professional for your specific situation.

What is the best exchange rate I can get when sending USD to CAD?

The best rate available to consumers is generally the mid-market rate — the midpoint between global buy and sell prices for USD/CAD, which is the rate you’d see on Google, XE.com, or Reuters. Banks often offer rates a few percentage points worse than this, while specialist services tend to offer rates much closer to mid-market. Wise is widely recognized for pricing close to the mid-market rate with a separate, disclosed fee. To get a better rate: compare live quotes across a few providers before sending, consider setting up rate alerts, and for large amounts, ask a specialist like OFX or Currencies Direct about a forward contract to lock in today’s rate for a future transfer.

Can I send money from the USA to Canada using my phone?

Yes — mobile transfers are the norm. Major transfer platforms offer iOS and Android apps that let you create an account, verify your identity, link a bank account or card, and send money entirely from your phone. Wise, Remitly, Western Union, MoneyGram, and PayPal all offer mobile apps, and many users find the mobile experience faster than desktop. You can track transfers in real time, get notifications when funds are delivered, set up recurring transfers, and manage multiple recipients from your phone. For security, use a strong PIN or biometric lock on your phone, enable two-factor authentication on your transfer app, and avoid initiating transfers over public Wi-Fi.

What happens if my transfer to Canada is delayed or something goes wrong?

Reputable transfer services have clear processes for delays and errors. First, check your transfer status in the app or online portal — most platforms provide real-time tracking. Common causes of delays include additional identity verification requests, processing delays on the recipient’s bank side, transfers initiated on weekends or holidays, and amounts that trigger compliance review. If a transfer is delayed well beyond the estimated timeframe, contact customer support directly — Wise, Remitly, and OFX all offer support via chat, email, and phone. If funds were sent to the wrong account due to an error on your part, contact the platform immediately; recovery is possible but not guaranteed. If a platform fails to deliver your money and becomes unresponsive, you may have recourse through your state’s financial regulator, and for card-funded transfers, through your card issuer’s dispute process.

🎓 NEXT STEP FOR NEWCOMERS TO THE USA

How to Build Your Credit Score in the USA (2026) — Free Guide

You’re now equipped to send money efficiently. The next step in your financial setup: building a strong US credit score. This free guide is written specifically for immigrants, expats, and visa holders starting from zero.

Conclusion

Sending money from the USA to Canada is more accessible, affordable, and fast today than it was even a few years ago — but only if you take a few minutes to compare your options. The days of walking into a bank, paying a flat wire fee, and accepting whatever exchange rate is offered without question are increasingly avoidable for informed consumers. Specialist platforms like Wise, Remitly, and OFX have changed the cross-border transfer landscape, putting more competitive rates and clearer pricing directly in the hands of everyday senders. Whether you’re sending a few hundred dollars to help a family member or moving a larger amount for a real estate purchase, there’s very likely a better-suited option than your bank’s default wire transfer.

The key takeaways from this guide: always compare the total cost, including the exchange rate margin, not just the stated fee; choose a provider that matches your specific needs in terms of speed, amount, and frequency; complete your account verification in advance so you’re ready to send when you need to; and stay aware of any reporting obligations — particularly FBAR for U.S. persons with foreign accounts — that may apply to your situation. Security should never be an afterthought: enable two-factor authentication, double-check recipient details every time, and stay alert to common scams described earlier in this guide.

The USA-Canada corridor is one of the world’s most active money transfer routes, and ongoing competition among providers continues to push fees down and service quality up. Bookmark this guide for future reference, use the FAQ section above for quick answers to common questions, and revisit the comparison tables periodically — pricing in this space changes often, and a few minutes of comparison before a larger transfer can make a meaningful difference to how much your recipient actually receives.

Ready to Make Your First Transfer?

Compare live rates from Wise, Remitly, and OFX — takes less than 2 minutes and costs nothing to check.

Sources

- Consumer Financial Protection Bureau — Remittance Transfer Rule (Regulation E, Subpart B)

- FinCEN — Report of Foreign Bank and Financial Accounts (FBAR)

- IRS — Frequently Asked Questions on Gift Taxes

- FINTRAC — Electronic Funds Transfer Reporting Guidance

- Wise — Pricing for sending money from the US

- Remitly — Send money to Canada

- OFX — Rates and Fees

Rates, fees, thresholds, and regulations referenced in this article are accurate to the best of our knowledge as of June 2026, but are subject to change. Always confirm current figures directly with the relevant provider or official source before making financial decisions.

Written by Talal Eddaouahiri

Founder & Editor-in-Chief | Former International Banking Executive

Talal is a Moroccan immigrant to the USA with 15+ years of experience in international banking. He founded MoneyAbroadGuide to help newcomers navigate the financial complexities of moving abroad.