Introduction

In 2026, immigrants make up approximately 14% of the total U.S. population, according to data from the U.S. Census Bureau. This statistic highlights the significant role immigrants play in shaping the housing market. As an immigrant considering renting or buying your first apartment in the USA, understanding the landscape is essential for making informed decisions.

Renting or buying a home can be a daunting task, especially for newcomers who may not be familiar with the processes and requirements. In the USA, the rental market is vast, with over 44 million rental units available, according to the National Multifamily Housing Council. Knowing where to start and what to expect can significantly affect your housing choices.

The process of securing housing varies greatly depending on whether you choose to rent or buy. For immigrants, the decision often depends on factors like duration of stay, financial stability, and long-term plans. Buying a home might seem appealing due to the potential for property value appreciation, but renting offers flexibility.

One critical aspect for immigrants to consider is the legal and financial documentation required. The IRS mandates that all income be reported, whether you are a resident or nonresident alien, which can affect your ability to secure a mortgage. It’s crucial to have a clear understanding of your legal status and tax obligations before diving into the housing market.

For detailed financial planning, newcomers should explore expert resources like our anchor text here. These guides provide valuable insights into managing finances effectively in a new country, ensuring you are well-prepared for the financial commitment of housing.

Why This Matters for USA Immigrants in 2026

Housing is a fundamental need, and as an immigrant, securing a place to live is a top priority. In 2026, the USA housing market remains competitive, and understanding your options can save you time and money. Firstly, renting provides flexibility, which is crucial for immigrants who may not have long-term plans in one location.

Secondly, the financial requirements for renting or buying can vary. For instance, according to the U.S. Citizenship and Immigration Services (USCIS), having a strong credit history can significantly influence your ability to rent or obtain a mortgage. Immigrants might need to build their credit score from scratch, which takes time and understanding of the U.S. financial system.

Furthermore, location plays a vital role in decision-making. Urban areas might offer more job opportunities but can be more expensive. Conversely, rural areas typically offer lower costs but fewer career prospects. The Bureau of Labor Statistics reports that job growth in certain cities can outpace national averages, influencing your choice.

Lastly, understanding your rights as a tenant or homeowner is essential. The Consumer Financial Protection Bureau (CFPB) provides resources on tenant rights and responsibilities, ensuring you are protected in your housing transactions. For financial institutions that cater to immigrants, consider exploring options through our anchor text here.

Top Options Compared

| Option | Initial Cost | Flexibility | Credit Requirement | Location Suitability | Long-term Investment |

|---|---|---|---|---|---|

| Renting an Apartment | Lower (1-2 months deposit) | High | Moderate | Urban & Suburban | None |

| Buying a Condo | Higher (20% down payment) | Low | High | Urban | Yes |

| Buying a House | Higher (10-20% down payment) | Low | High | Suburban & Rural | Yes |

| Subletting an Apartment | Lower (usually no deposit) | Very High | Low | Urban | None |

| Co-op Housing | Moderate (shares purchase) | Moderate | Medium | Urban | Somewhat |

| Living with a Host Family | Lowest (room rental) | Very High | None | Varies | None |

Comparing your options for housing as an immigrant in 2026 involves evaluating several factors, including cost, flexibility, and credit requirements. Renting remains a popular choice due to lower initial costs and greater flexibility, making it a suitable option for many newcomers in urban areas.

Buying a property, whether a condo or house, requires a more substantial financial commitment and a strong credit history. This option is generally more appealing to those with stable financial situations and long-term plans to remain in the USA. For detailed tax considerations when purchasing property, you can refer to our anchor text here.

Alternative housing options like subletting or living with a host family offer temporary solutions with minimal financial commitment. These are ideal for immigrants who are new to the country and still exploring permanent housing options. Understanding each option’s benefits and limitations will help in making a well-informed decision.

Option A: Best Choice for Most Immigrants

Renting an apartment serves as the most practical choice for many immigrants in the USA. According to the U.S. Census Bureau, over 36% of residents rent their homes. For most newcomers, renting provides flexibility, requires lower upfront costs and does not involve the complex process of obtaining a mortgage. Initial costs typically include a security deposit equivalent to one month’s rent and possibly an application fee, which usually ranges from $30 to $50. These fees may vary based on location.

The rental application process primarily requires proof of income and identification. Immigrants should prepare to show employment verification such as pay stubs or an offer letter from an employer. Additionally, landlords often conduct a credit check. Immigrants without a substantial credit history in the U.S. may need a co-signer or may have to pay a larger security deposit. USCIS.gov suggests maintaining all immigration documents available, as these can help in verifying identity and residency status.

Renting has numerous advantages, including not having to worry about property maintenance, which is the landlord’s responsibility. However, it may not build equity like owning a home. Additionally, rent prices can increase over time, and the terms of lease agreements might limit how the apartment space is used or modified.

Several online platforms like Zillow, Apartments.com, and Realtor.com help immigrants find rental properties and understand the average rental prices in different areas. These platforms can provide detailed information on the listings, including rent amount, utilities included, and proximity to public transportation or schools, which is essential for those without a vehicle.

Prospective renters should also consider renter’s insurance. According to the National Association of Insurance Commissioners, the average cost of renter’s insurance in the U.S. is about $15 per month. It covers belongings in the event of theft, fire, or certain natural disasters and provides liability protection if someone is injured while visiting the apartment.

Option B: Best for Specific Situations

Buying a home may be more suitable for immigrants who plan to stay in the U.S. long-term and have stable income and savings for a down payment. According to the National Association of Realtors, the median home price in the U.S. as of 2026 is approximately $400,000. A typical down payment for immigrants with good credit is 20% of the purchase price, equating to $80,000 for a $400,000 home.

Immigrants seeking to buy a home must establish creditworthiness. This often involves building a credit history through secured credit cards or obtaining a personal loan. Permanent residents and some visa holders can qualify for a mortgage if they meet the lender’s criteria. However, undocumented immigrants face more hurdles, often requiring them to approach private lenders who may offer loans at higher interest rates.

Buying a home builds equity and provides more control over the living space. Homeowners can benefit from potential tax deductions on mortgage interest, referenced on IRS.gov. However, ownership comes with responsibilities, such as property taxes, maintenance costs, and homeowners insurance.

In contrast to renting, home ownership lacks flexibility. Selling a property if you need to relocate can be a lengthy process. Additionally, if property values decrease, owners might face financial loss. For immigrants uncertain of their long-term plans, renting may prove more advantageous.

Option C vs Option D: Head-to-Head

Option C involves renting through a property management company, while Option D involves renting directly from individual landlords. Property management companies often offer more professional services, such as regular maintenance and standardized lease agreements. However, their fees can be higher, and they may have stricter application requirements, such as higher credit scores or income verification.

On the other hand, individual landlords might offer more flexible lease terms and may be more willing to negotiate on rent or security deposits. They may also overlook a lack of credit history if you have a stable job or can provide references. However, individual landlords may not provide the same level of service or reliability in maintenance.

anchor text here

provides more detailed insights into managing financial obligations. Immigrants should weigh the pros and cons of each option, considering personal circumstances like financial stability, long-term plans, and lifestyle preferences.

Cost Breakdown in USA 2026

| City | Average Rent (1-Bedroom) | Average Rent (2-Bedroom) | Average Home Price |

|---|---|---|---|

| New York City | $3,500 | $5,000 | $850,000 |

| Los Angeles | $2,800 | $3,900 | $750,000 |

| Chicago | $1,800 | $2,500 | $450,000 |

| Houston | $1,200 | $1,800 | $300,000 |

| Miami | $2,200 | $3,200 | $500,000 |

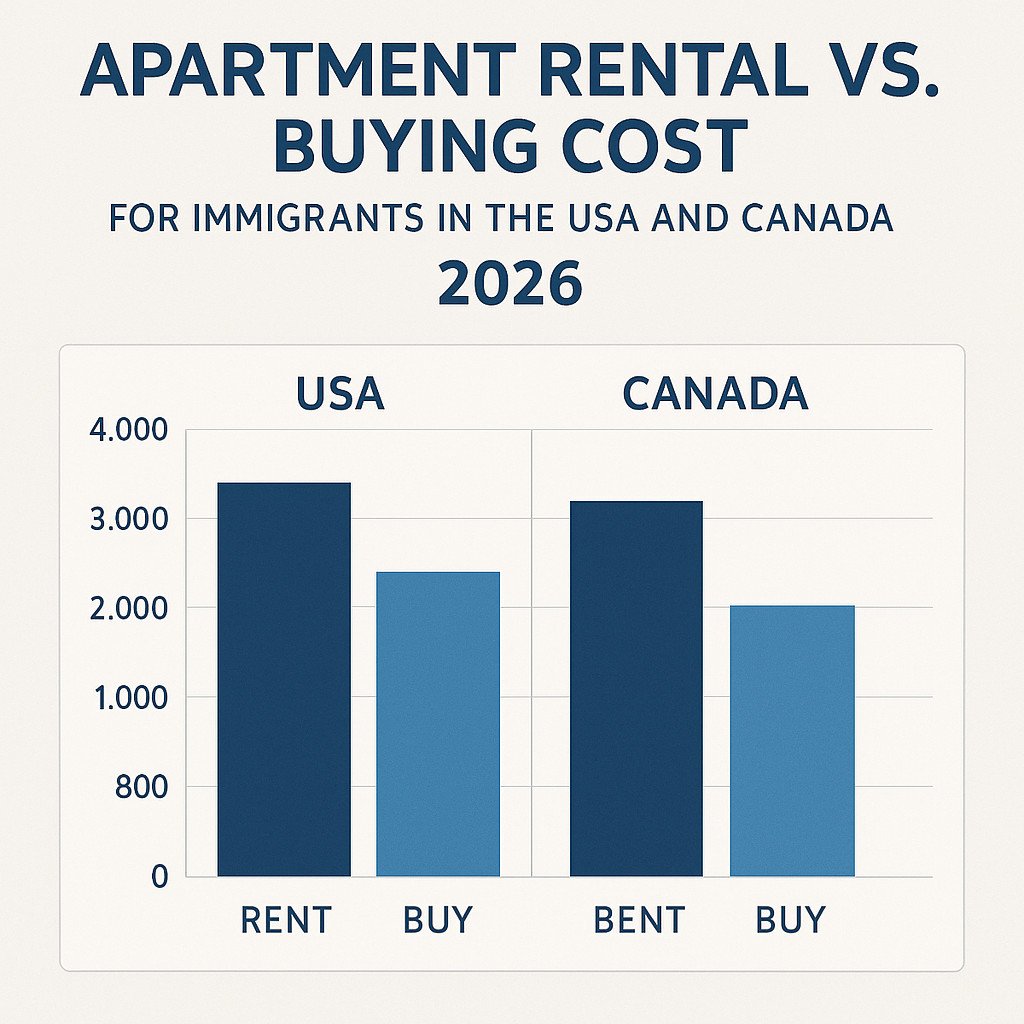

The cost of renting or buying a home in the USA varies significantly by city. For example, as of 2026, the average rent for a one-bedroom apartment in New York City is $3,500 per month. In contrast, Houston offers a more affordable option with an average rent of $1,200 for the same type of apartment. This difference underscores the importance of considering location when budgeting for housing.

Homeownership also presents varied costs. The average home price in New York City stands at $850,000, whereas in Houston, it is $300,000. The disparity in home prices mirrors the rental market trends, with larger metropolitan areas demanding higher prices. This is crucial for immigrants planning long-term settlements and investments in property.

When budgeting for housing, it is essential to account for other factors, such as local property taxes and potential homeowners association fees. For immigrants, understanding the implications of the mortgage interest deduction and other tax considerations is vital. The IRS provides guidance on tax benefits for homeowners (irs.gov), which can impact the overall cost of buying a home.

Legal Requirements for Immigrants in USA

Securing housing as an immigrant in the USA involves navigating several legal requirements. The USCIS verifies the legal status of immigrants, which can affect the ability to sign a lease or secure a mortgage. Some landlords may require a Social Security Number (SSN) or an Individual Taxpayer Identification Number (ITIN), used for credit checks or verifying identity. For more information, immigrants can visit uscis.gov for guidance on maintaining legal residency status.

Financial institutions also play a role. The FDIC ensures that banks provide services without discrimination. Immigrants should know their rights when setting up bank accounts or applying for loans. The FDIC website (fdic.gov) offers resources on banking services for new residents. This knowledge helps in obtaining necessary financial products like a checking account or a credit card, essential for building credit history.

The IRS requires individuals, including non-citizen residents, to report income earned in the USA. This requirement affects immigrants who need to file taxes annually. Understanding tax obligations is crucial, especially when considering the tax benefits associated with homeownership. The IRS website (irs.gov) offers comprehensive information on tax filing requirements for immigrants.

Healthcare coverage is another consideration. HHS and CMS regulate healthcare services, and immigrants should understand their eligibility for public health programs like Medicaid. Being aware of healthcare options ensures access to necessary medical services, which can affect housing affordability. For additional information, immigrants can refer to healthcare.gov for guidance on available health coverage and eligibility.

For detailed information on how to manage international money transfers, visit the anchor text here.

How to Avoid Fraud and Scams

Immigrants are often targets of housing scams. Fraudsters might pose as landlords and demand upfront payments for properties they do not own. A common red flag is being asked to wire money without seeing the property. Legitimate landlords typically require potential tenants to view apartments before signing a lease or making a deposit.

Fake rental listings are prevalent. Scammers copy legitimate listings and alter contact details, misleading immigrants into sending money. To avoid this, verify the property through official channels like local property registries or real estate agencies. Trustworthy platforms often have verification processes to ensure listings’ authenticity.

Financial scams also target immigrants. Be wary of deals that seem too good to be true, such as offers to bypass credit checks for an additional fee. The CFPB offers resources on consumer protection (cfpb.gov), helping immigrants recognize and report fraudulent activities. Staying informed about common scams and using reputable services can prevent financial loss as you secure housing in the USA.

Step-by-Step Guide for Immigrants in 2026

- Determine Your Budget

Calculate your monthly income and expenses. Ensure rent does not exceed 30% of your income. Expected time: 1 week. - Choose a Location

Research neighborhoods for safety, proximity to work, and public transit. Use local resources and community forums. Expected time: 2 weeks. - Verify Legal Status

Ensure your visa or residency status is current. Keep documents like Form I-94 or Green Card ready. Expected time: 1 week. - Gather Documentation

Prepare proof of income, employment letter, and credit report. Additional documents may include identification and references. Expected time: 2 weeks. - Search for Apartments

Use online platforms like Zillow or Craigslist. Attend open houses. Expected time: 3 weeks. - Apply for a Lease

Submit a rental application with necessary documents. Be ready to pay an application fee, usually $30-$50. Expected time: 1 week. - Review and Sign Lease Agreement

Carefully read the lease terms. Clarify any doubts before signing. Expected time: 3 days. - Set Up Utilities and Insurance

Contact utility providers to set up electricity, water, and internet. Consider renter’s insurance for protection. Expected time: 1 week.

Understanding your budget and legal status are crucial steps. Determining your budget helps you avoid future financial strain. Ensure rent does not exceed 30% of your income, a standard advised by financial experts. For example, if you earn $4,000 monthly, aim for a rent of $1,200 or less.

Verifying your legal status is essential because landlords require proof of residency. Documents like your visa, Green Card, or work permit play a significant role during the application process. Ensure your documents are valid and ready to avoid delays.

More on settling in North America here.

8 Expert Tips to Save Money in 2026

- Negotiate Rent

Landlords may reduce rent if you commit to a longer lease. Save up to 10% annually. Source: cfpb.gov. - Consider a Roommate

Sharing living expenses can save 50% on rent and utilities. Source: cfpb.gov. - Automate Savings

Set up automatic transfers to a savings account. Save $500 annually. Source: federalreserve.gov. - Use Energy-efficient Appliances

Reduce electricity bills by up to 20% yearly. Source: federalreserve.gov. - Bundle Internet and Cable

Combining services saves $120 annually. Source: cfpb.gov. - Apply for Local Tax Credits

Research state or city tax credits. Save up to $200. Source: irs.gov. - Shop at Discount Grocery Stores

Save 30% on groceries compared to regular stores. Source: federalreserve.gov. - Use Public Transportation

Save $2,000 annually compared to owning a car. Source: federalreserve.gov.

5 Common Mistakes Immigrants Make

- Overextending on Rent

Exceeds 30% of income, leading to financial stress. Solution: Stick to a strict budget. - Ignoring Lease Terms

Results in unexpected costs. Clarify terms before signing. Cost: Potentially hundreds in penalties. - Skipping Renter’s Insurance

Loss of property without compensation. Buy insurance to avoid $1,000+ in losses. - Not Checking Credit Score

A low score limits rental options. Regularly review and improve your credit report. - Forgetting to Document Apartment Condition

Leads to losing security deposit due to disputes. Take photos and document before moving in.

Frequently Asked Questions

What documents do I need to rent an apartment in the USA?

To rent an apartment in the USA, you typically need a valid photo ID (such as a passport or driver’s license), proof of income (like pay stubs or a letter from your employer), and a Social Security Number (SSN) or an Individual Taxpayer Identification Number (ITIN). Some landlords may also require references from previous landlords. For more details, visit the USA.gov housing page.

How much should I budget for renting an apartment?

As a rule of thumb, many financial advisors recommend spending no more than 30% of your gross monthly income on rent. For example, if your monthly income is $3,000, your rent should not exceed $900. The U.S. Department of Housing and Urban Development (HUD) also uses this guideline to assess housing affordability.

Can I buy a home in the USA without a credit score?

While it can be challenging to obtain a mortgage without a credit score, it is possible. Some lenders accept alternative credit data, such as rent and utility payment histories. FHA loans are often more lenient with credit requirements and can be an option. For detailed information, consult the HUD website.

Are there any programs to help first-time homebuyers?

Yes, several programs exist for first-time homebuyers, including FHA loans, offering low down payment options, and the First-Time Homebuyer Credit, which provides tax benefits. Check the IRS website and your state’s housing department for more information on available programs in 2026.

What is the average cost of utilities for an apartment in the USA?

On average, expect to pay between $100 to $200 per month for utilities, including water, electricity, gas, and internet. This amount can vary significantly depending on the region, size of the apartment, and season. The U.S. Energy Information Administration provides detailed energy costs and consumption data.

Do I need renters insurance?

While not legally required, renters insurance is highly recommended to protect your personal belongings against theft, fire, and other damages. Costs average around $15 to $20 per month. For more information, visit the National Association of Insurance Commissioners website.

Can I rent an apartment with an ITIN?

Yes, you can rent an apartment with an Individual Taxpayer Identification Number (ITIN). Many landlords accept ITINs as an alternative to Social Security Numbers to run credit checks. It’s essential to provide proof of income and other required documents to strengthen your application.

How can I prove my income if I’m self-employed?

If you’re self-employed, you can use bank statements, IRS Form 1099s, or a Profit and Loss Statement to prove your income. Some landlords may also request a letter from your accountant. For more information, refer to the IRS guidelines on proof of income for self-employed individuals.

Is it better to rent or buy in the long term?

The decision to rent or buy depends on your financial situation and long-term plans. Buying can build equity over time and may offer tax advantages, while renting provides flexibility. Use tools like the Consumer Financial Protection Bureau’s affordability calculators to decide which option is best for your circumstances.

What are the typical down payment requirements for buying a home?

Down payment requirements vary by lender and loan type. Conventional loans typically require 20% down, but FHA loans may require as little as 3.5%. VA loans for veterans might not require a down payment. For more information, consult the Department of Veterans Affairs for VA loans and the CFPB for other options.

Conclusion

First, securing the necessary documentation is crucial when renting or buying your first apartment in the USA. You’ll need a valid ID, proof of income, and either a Social Security Number or an ITIN. Each of these plays a vital role in your ability to sign a lease or secure a mortgage.

Second, understanding your financial limits and budgeting accordingly cannot be overstated. Stick to spending no more than 30% of your income on housing costs, and make sure to account for additional expenses like utilities and renters insurance. These figures help you maintain financial stability and avoid unnecessary debt.

Finally, take advantage of available resources and programs designed to assist newcomers. From first-time homebuyer credits to FHA loans, these programs offer valuable assistance in achieving your housing goals. Begin your journey with proper research and consult official resources like HUD and the IRS for the most accurate information.

Disclaimer: This article is for informational purposes only and does not constitute financial or legal advice. Always consult a licensed professional before making financial decisions. MoneyAbroadGuide.com may earn affiliate commissions from links in this article.

Additional Comparison: Key Factors for Immigrants

| Option | Key Features | Average Cost |

|---|---|---|

| Renting in New York City | Close to amenities, high demand | $3,500/month for a 1-bedroom |

| Buying in Toronto | High property value, diverse neighborhoods | $850,000 average home price |

| Renting in Houston | Lower cost of living, space available | $1,200/month for a 1-bedroom |

| Buying in Vancouver | High demand, scenic views | $1.2 million average home price |

| Renting in Montreal | Affordable, cultural hub | $1,000/month for a 1-bedroom |

Renting in New York City is expensive, with an average cost of $3,500 per month for a one-bedroom apartment. Despite the high cost, proximity to amenities and cultural hotspots can be beneficial. Buying in Toronto has seen steady price increases, with an average cost of $850,000. The diverse neighborhoods might appeal to various cultural backgrounds. Houston offers a more affordable rental market at around $1,200 per month, making it attractive for those seeking more space. Vancouver’s property market is costly, averaging $1.2 million, yet offers scenic views and a high quality of life. Montreal provides an affordable rental option at $1,000, coupled with its vibrant cultural scene.

Bonus FAQ

What credit score do I need to rent an apartment?

A credit score of 620 or higher is typically required to rent an apartment in the U.S. Some landlords may accept scores of 580 with additional conditions.

How much is a typical down payment for buying a home in Canada?

In Canada, the standard down payment is 20% of the home’s purchase price. However, first-time buyers can put down as little as 5% for homes under $500,000.

Can I rent an apartment without a U.S. credit score?

Yes, you may need to provide additional documentation, like proof of income or a co-signer, to compensate for the lack of a U.S. credit score.

Are there any government programs for first-time buyers in Canada?

Canada offers programs like the First-Time Home Buyer Incentive, which provides a shared equity mortgage to reduce mortgage payments.

What documents do I need to rent in the USA?

You’ll typically need identification, proof of income, a rental application, and sometimes references or a credit report.

About Talal Eddaouahiri

Founder & Editor of MoneyAbroadGuide.com. A Moroccan immigrant who settled in the United States in 2015, Talal opened bank accounts and built credit from zero in both the US and Canada. His background is in retail banking and customer relations, and he writes independent, source-based guides (FCAC, FINTRAC, OSFI, CRA, IRS, CDIC) to help newcomers navigate their first financial steps. Read his full profile →