Quick Answer: Newcomers to Canada start with no Canadian credit history, but can build a strong score within 6–12 months by opening a bank account, applying for a secured credit card, and using credit responsibly. Your first steps: get your Social Insurance Number, open a Canadian bank account, and apply for a secured or newcomer credit card.

Arriving in Canada is exciting — but financially, you’re starting from scratch. No matter how strong your credit history was in your home country, Canadian lenders and the two major credit bureaus, Equifax and TransUnion, have no record of you. According to the Financial Consumer Agency of Canada (FCAC), a credit score in Canada ranges from 300 to 900, and building one requires a Canadian credit file — something most newcomers don’t have on arrival.

This gap creates real friction. Landlords run credit checks before approving leases. Employers in regulated industries may review your credit file. Cell phone providers, utility companies, and auto lenders all rely on your Canadian score. Newcomers consistently report being denied for basic financial products in their first weeks, simply because no file exists — not because they’re a credit risk.

The good news: Canada’s financial system includes specific pathways designed for immigrants, temporary residents, and permanent residents at exactly this stage. Major banks operate dedicated newcomer banking programs, and the FCAC provides free, bilingual guidance on navigating the Canadian credit system.

This guide walks you through every step — from opening your first account to understanding what actually moves your score — so you can build a solid credit foundation as efficiently as possible.

Before diving in, two resources will anchor your journey: our breakdown of the Best Bank Account for Newcomers to Canada and our detailed walkthrough on How to Build Credit in Canada as a Newcomer. Together, they cover the infrastructure you need before your first credit product.

Whether you arrived last week or are still preparing your move, the strategy is the same: start early, use the right products, and stay consistent. Credit in Canada rewards time and discipline above all else.

1. Quick Overview: Building Credit in Canada From Zero

Affiliate disclosure: We earn a commission at no cost to you.

No affiliate opportunities detected – add mentions of recommended services: Learn More

Very few affiliate blocks added – consider adding more service comparisons: Learn More

Categories not covered: [‘money_transfer’, ‘insurance’, ‘fintech’, ‘banking’] – consider adding content about these: Learn More

Canada’s credit system does not import your home-country credit history. Regardless of your score in India, the Philippines, Nigeria, or anywhere else, you arrive with a blank file — and a blank file is treated nearly identically to a poor score by lenders. The good news: with disciplined use of the right products, most newcomers reach a reportable credit score within three to six months and a competitive score above 660 within one to two years.

Why Starting From Zero Is Both a Problem and an Opportunity

Without a Canadian credit file, you will face higher deposits on apartments, rejection for most unsecured credit cards, and limited financing options for vehicles or businesses. According to the Financial Consumer Agency of Canada (FCAC), lenders use your credit report to assess risk on virtually every financial product — including some cell phone plans and rental applications. Starting clean means you control the narrative from day one, with no past delinquencies dragging your score down.

The Five Core Levers — At a Glance

Credit scoring in Canada (Equifax and TransUnion both operate here) weighs five factors. Understanding the weight distribution lets you prioritize effort:

| Factor | Approximate Weight |

|---|---|

| Payment history | 35% |

| Credit utilization | 30% |

| Length of credit history | 15% |

| Credit mix | 10% |

| New inquiries | 10% |

Payment history and utilization together control 65% of your score. Everything else is secondary. This means two actions dominate your early strategy: pay every balance on time, and keep utilization below 30% of your available limit (ideally below 10% for maximum impact).

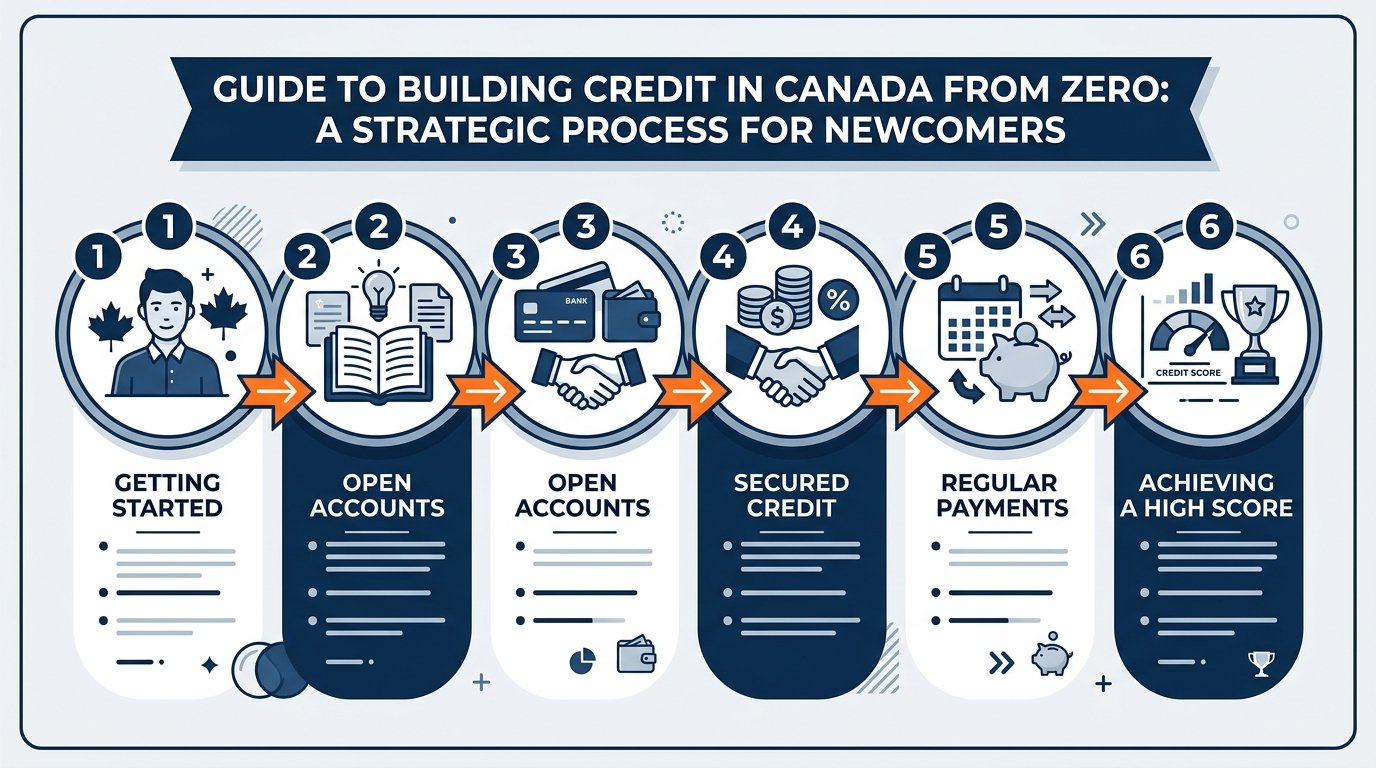

The Fastest Legal Path: Four Parallel Steps

- Open a newcomer bank account immediately — the Best Bank Account products from major banks (as covered above) often include a path to a secured or co-branded credit card within the same application flow. Keeping all products at one institution simplifies reporting and builds relationship history.

- Apply for a secured credit card — you deposit collateral (typically $200–$500) which becomes your credit limit. Scotiabank, Home Trust, and Capital One all offer secured cards accessible without a Canadian credit history. Use it for one recurring bill; pay the statement balance in full monthly.

- Become an authorized user — if a family member or trusted contact already holds a Canadian credit card in good standing, being added as an authorized user can accelerate file thickness. The primary cardholder’s positive history may reflect on your report within 30–60 days.

- Report rent payments — services such as Landlord Credit Bureau and FrontLobby report on-time rent to Equifax Canada. Since rent is typically your largest monthly expense, this converts a previously invisible payment into active credit-building data.

What the Timeline Realistically Looks Like

- Month 1–2: File opens; secured card and/or authorized user status established

- Month 3–4: First FICO/Beacon score generated (minimum two accounts reporting, or one account open longer than six months per Equifax methodology)

- Month 6: Score typically in the 580–640 range with clean history

- Month 12–18: Score reaches 660–720 with consistent utilization management — sufficient for most unsecured cards and competitive auto financing

Common Errors That Reset the Clock

- Applying for multiple credit products within 60 days (hard inquiries stack and signal desperation to lenders)

- Carrying a balance to “show activity” — this is a myth; you do not need to pay interest to build credit

- Closing the secured card too early; length of history matters, so keep the account open even after graduating to an unsecured card

The sections that follow cover each strategy in granular detail — specific products, eligibility rules, provincial considerations, and how programs like the IRCC newcomer pathways affect document requirements at application.

2. How Building Credit From Zero Works in Canada (and Why It Matters)

The Credit Invisible Problem

When you arrive in Canada, your financial history from your home country doesn’t travel with you. Equifax Canada and TransUnion maintain separate national databases — a spotless 20-year credit record in India, the Philippines, or Nigeria registers as nothing here. You begin as what lenders call “credit invisible”: no file, no score, no risk signal either way.

This is structurally different from having bad credit. A consumer with bad credit has a file lenders can assess. A credit-invisible newcomer is simply unreadable — and most lenders default to denial when they can’t read you.

Why Your Canadian Credit File Matters Beyond Borrowing

Most newcomers associate credit with loans. The practical dependencies run much wider:

Rental housing. The majority of Canadian landlords pull a credit report before approving an application. Without a file, you compete only on the basis of a larger deposit or a guarantor — both difficult when you’ve just arrived.

Utilities and phone plans. Telecom providers (Bell, Rogers, Telus) routinely require a credit check for postpaid plans. No file typically means prepaid-only or a security deposit.

Employment. Certain regulated industries — financial services, security, some federal roles — include a credit check as part of background screening. IRCC settlement materials note that financial stability indicators affect multiple integration outcomes.

Insurance premiums. Auto and tenant insurers in most provinces use credit-based insurance scores as one rating factor. A thin file can translate into higher premiums for the first year or two.

Future mortgage eligibility. Canada Mortgage and Housing Corporation (CMHC) insured mortgage rules require a minimum two-year credit history with at least two active tradelines. Starting your file on Day 1 directly determines when you qualify.

How the Canadian Credit System Is Structured

Canada’s consumer credit system operates under federal oversight through the Financial Consumer Agency of Canada, which regulates how credit bureaus, lenders, and creditors report and handle your data. The two national bureaus — Equifax Canada and TransUnion Canada — receive data feeds from lenders, telecoms, utilities, and landlord-reporting services (such as Landlord Credit Bureau, referenced above).

Your file is built from tradelines: individual accounts that report your payment behaviour monthly. A tradeline must typically be active for six months before the bureau generates a score. That six-month threshold is the first milestone every newcomer is racing toward.

The Core Mechanism: What Actually Builds Your File

Three categories of activity open a tradeline for a credit-invisible person:

- Secured or newcomer credit cards — Home Trust and Capital One products (named above) report monthly to one or both bureaus, generating a tradeline from first statement.

- Rent reporting — Landlord Credit Bureau converts on-time rent payments into bureau-reportable tradelines, effective for newcomers who cannot yet access traditional credit.

- Credit-builder loans — Offered by several credit unions (Vancity, Desjardins), these products hold funds in a locked account while you make payments, reporting the loan tradeline monthly.

Each method creates a reporting relationship between your behaviour and your file. No reporting relationship = no file growth, regardless of how responsibly you manage cash.

The Immigrant-Specific Timing Constraint

Unlike a Canadian who builds credit gradually through adolescence, newcomers face a compressed urgency: rental markets don’t wait, phone contracts are needed immediately, and employment screening happens within weeks of arrival. According to Service Canada, obtaining your Social Insurance Number is the administrative prerequisite that unlocks most credit applications — making SIN registration a Day 1 financial priority, not a formality.

The sections that follow map the fastest compliant path from credit-invisible to scoreable file.

3. Eligibility Requirements for Immigrants

Canada’s credit system doesn’t require citizenship — but lenders and bureaus do impose specific documentation thresholds that catch many newcomers off guard.

Who Qualifies to Start Building Credit

Any individual with legal status in Canada can open a credit file. This includes:

- Permanent residents (PRs) — eligible immediately upon landing

- Temporary foreign workers with a valid work permit

- International students holding a valid study permit

- Refugees and protected persons — eligible once Immigration, Refugees and Citizenship Canada (IRCC) confirms status

- Newcomers on spousal or family reunification pathways

Undocumented individuals and visitor visa holders are generally excluded from obtaining credit products in Canada.

Mandatory Identification Documents

Lenders follow FINTRAC Know Your Customer (KYC) rules, which require identity verification before extending any credit. Practically, this means:

| Document | Purpose | Notes |

|---|---|---|

| Passport | Primary photo ID | Must be valid |

| Permanent Resident Card or IRCC Confirmation of PR | Proof of status | CoPR accepted at landing |

| Study or work permit | Status verification for temporary residents | Must show valid dates |

| SIN (as noted above) | Links credit activity to your file | Required for most credit applications |

| Proof of address | Residency confirmation | Utility bill, lease, bank statement |

Some financial institutions also accept a provincial photo ID card or a driver’s licence once obtained provincially, but this is secondary to status documents.

Income and Employment Thresholds

Secured credit cards — the most accessible first product — typically carry no income requirement because your deposit covers the credit limit. Unsecured products impose variable bars:

- Entry-level unsecured cards (e.g., Capital One and Home Trust products, named above): minimum income requirements range from $12,000–$15,000 annually

- Retail store cards: often the most flexible, with approvals based on purchasing history rather than income history

- Newcomer-specific bank programs: several Schedule I banks (TD, RBC, Scotiabank, BMO, CIBC) offer “newcomer banking packages” that bundle accounts with a starter credit card — often waiving the standard income or credit-history requirement for the first 12–24 months after landing

Residency Duration Requirements

There is no minimum residency period to apply for a secured card. However:

- Unsecured cards with better terms typically require 3–6 months of Canadian address history

- Mortgage qualification under CMHC’s mortgage loan insurance rules generally requires at least 2 years of Canadian credit history

- Auto financing lenders commonly request 6–12 months of Canadian bureau history before approving without a co-signer

Credit Bureau Enrollment: No Application Required

A newcomer’s credit file opens automatically the moment a lender reports their first account to Equifax Canada or TransUnion Canada — there is nothing to “apply for” at the bureau level. The Financial Consumer Agency of Canada confirms that consumers have the right to request a free credit report once their file exists, which typically takes 30–45 days after the first account is opened and reported.

Special Pathway: International Credit History

A small but growing number of lenders participate in Nova Credit, a cross-border credit reporting platform that translates credit files from India, Mexico, the Philippines, South Korea, and several other countries into a Canadian-readable format. Newcomers from these countries may qualify for unsecured products immediately, bypassing the standard zero-history barrier entirely.

Age Requirement

The minimum age to enter into a credit contract in Canada is the age of majority in your province — 18 in Alberta, Manitoba, Ontario, Prince Edward Island, Quebec, and Saskatchewan; 19 in British Columbia, New Brunswick, Newfoundland and Labrador, Northwest Territories, Nova Scotia, Nunavut, and Yukon. A parent or guardian can add a minor as an authorized user, which begins building a thin file before the age of majority.

4. Top Credit-Building Options Reviewed

Four credit-building paths dominate the newcomer market. Each has a different speed, cost, and approval barrier — here’s how they compare in practice.

4.1 Secured Credit Cards

How they work: You deposit collateral (typically $300–$1,000) and receive a matching credit limit. The card reports monthly to Equifax Canada and TransUnion Canada, generating the payment history and utilization data that drive your score.

Best picks for newcomers:

- Home Trust Secured Visa — accepts applicants with no Canadian credit history; annual fee applies; widely available outside Quebec

- Capital One Secured Mastercard — no annual fee tier available; soft-pull pre-approval protects your file during early months when every hard inquiry counts

Key tactic: Keep utilization under 10% of the posted limit — not the deposit amount — because issuers report the limit figure, not the deposit. Paying the statement balance in full by the due date avoids interest and maximizes payment-history points, the heaviest scoring factor as noted above.

Timeline to measurable score: Most newcomers see a scoreable file within 3–4 months of first reporting; a functional prime score typically takes 9–11 months of clean history.

4.2 Newcomer Banking Packages With Credit Products

RBC, BMO, and CIBC each bundle a chequing account with a credit card pre-approved at account opening for newcomers holding a valid PR card or IRCC Confirmation. The credit limit is modest ($500–$1,500) but the approval is near-instant because the bank applies its own internal KYC assessment rather than relying on a Canadian bureau score.

Advantage: One branch visit opens both a deposit account and a revolving credit line simultaneously — two separate products, one session. A single revolving account is sufficient to start; opening multiple cards the same week generates multiple hard inquiries and suppresses early scores.

Watch: Promotional newcomer packages often revert to standard fee structures after the first year. Read the account agreement, not the brochure.

4.3 Credit-Builder Loans

A credit-builder loan reverses the usual structure: the lender holds the loan proceeds in a locked account while you make fixed monthly payments. Once the loan matures, you receive the accumulated balance. The payments are reported to both bureaus throughout.

Where to find them: Several credit unions and fintech lenders (e.g., KOHO’s credit-building feature, Refresh Financial) offer this product. Credit unions operating under provincial regulation — not federally chartered banks — tend to have more flexible approval criteria for newcomers without a credit file.

Best use case: Newcomers who cannot fund a secured card deposit but can commit to a fixed monthly payment of $50–$75. The installment account type also diversifies the credit mix beyond revolving, which FCAC confirms contributes to overall score calculation.

4.4 Rent Reporting via Landlord Credit Bureau

Rent payments are the largest recurring financial obligation most newcomers carry, yet they are invisible to bureaus by default. Landlord Credit Bureau (LCB) connects landlords and tenants to report on-time rent to Equifax Canada.

Practical steps:

- Ask your landlord to register with LCB (free for landlords)

- If the landlord declines, use a tenant-side reporting service (Chexy, FrontLobby) that processes rent through their platform and submits the data directly

- Retroactive reporting is available for some services — up to prior months of payments — accelerating file thickness faster than waiting for new months to accumulate

Limitation: Rent reporting creates a positive tradeline but it is not yet universally weighted by all lenders’ internal scorecards, even when it appears on the bureau file. It supplements — it does not replace — a revolving credit account.

Which Path First?

Open a secured card or a newcomer bank package credit card as the anchor product. Add rent reporting immediately at no cost. Consider a credit-builder loan only if your budget can absorb the payment without strain — forced default on a credit-builder loan damages the file it was designed to build.

Comparing Credit-Building Products for Newcomers in Canada

Choosing the right credit-building tool depends on your immigration status, income level, and how quickly you need an established credit file. According to Equifax Canada, a credit score of 660+ qualifies borrowers for most mainstream financial products — making your starting strategy critical.

The table below compares the most widely used credit-building instruments available to newcomers across Canadian financial institutions, ranked by accessibility and cost-effectiveness.

| Product | Minimum Deposit / Cost | Credit Bureau Reported | Approval Without Canadian History | Typical Timeline to Score | Best For |

|---|---|---|---|---|---|

| Secured Credit Card | $200–$500 deposit | Yes — Equifax & TransUnion | ✅ Yes | 3–6 months | Most newcomers, PR holders |

| Credit Builder Loan | $0 down; $25–$50/mo payments | Yes — both bureaus | ✅ Yes | 6–12 months | Those building savings simultaneously |

| Newcomer Credit Card (RBC, CIBC, Scotiabank) | No deposit required | Yes — both bureaus | ✅ Yes (passport + visa) | 3–6 months | Newcomers within first 2 years |

| Retail / Store Credit Card | No deposit | Yes — varies by issuer | ⚠️ Sometimes | 3–6 months | Secondary card only |

| Authorized User on Partner’s Card | No cost | Yes — primary holder’s bureau | ✅ Yes | Immediate reporting | Spouses of established cardholders |

| Rent Reporting Services (e.g., FrontLobby) | $0–$10/month | Yes — Equifax only | ✅ Yes | 1–3 months | Renters without card access |

Key regulatory note: All reporting institutions must comply with FCAC (Financial Consumer Agency of Canada) guidelines on credit disclosure. Newcomers on work permits, study permits, or as permanent residents are equally eligible under federal consumer protection rules — institutions cannot deny applications solely based on immigration status under the Canadian Human Rights Act.

Real-World Examples

Case Study 1: Amara’s 18-Month Credit Journey (Nigeria → Toronto)

Amara Okonkwo arrived in Toronto in March 2022 on a permanent resident visa with no Canadian credit history. Her first step was opening a chequing account at TD Bank within her first week, using her Nigerian passport and PR card. She then applied for a secured credit card (TD First Class Travel Secured, $500 deposit) immediately after.

Amara charged only groceries and transit — keeping her utilization below 20% monthly. By month six, her Equifax score reached 612. She then applied for a Rogers World Elite Mastercard (unsecured), which she was approved for at month nine.

Simultaneously, Amara joined a credit union RRSP loan program — borrowing $1,500 to contribute to an RRSP, then repaying it over 12 months. This installment mix accelerated her profile.

By month 18, her credit score reached 724, qualifying her for a car loan at 6.9% APR. Her strategy: two active tradelines, low utilization, zero missed payments — the exact formula lenders want to see.

Case Study 2: Rajiv’s Thin-File Breakthrough (India → Calgary)

Rajiv Sharma relocated to Calgary in January 2023 as a Temporary Foreign Worker (TFW) in the oil and gas sector. Because TFWs face stricter lending criteria, his first secured card application at RBC was declined — a common experience newcomers report during initial months.

Rather than reapplying immediately, Rajiv opened a Capital One Guaranteed Secured Mastercard ($75 annual fee, $200 deposit), which does not require a credit check. He also enrolled in a credit builder loan through a local Alberta credit union — $1,000 held in trust, repaid at $90/month over 12 months.

After six months of consistent payments, Equifax assigned him an initial score of 591. Rajiv then added himself as an authorized user on his employer’s corporate credit card, further diversifying his credit mix without additional liability.

By month 14, his score reached 689, enabling him to secure a rental apartment without a co-signer — saving approximately $2,400 in guarantor fees his property manager originally requested. His critical lesson: a declined application is not permanent; it is a redirection toward the right product.

Expert Recommendation

Top Pick: Secured Credit Card (Neo Financial or Scotiabank Scene+ Visa)

For most newcomers arriving in Canada with no credit file, a secured credit card is the single most effective first move. You deposit collateral—typically $300–$500—which becomes your credit limit, and every on-time payment is reported to Equifax and TransUnion, actively building your bureau profile from month one.

Neo Financial’s secured card earns our top recommendation for 2024. It carries no annual fee, reports to both major bureaus, and offers a straightforward upgrade path to unsecured credit once your score crosses approximately 660–680. Scotiabank’s Scene+ Secured Visa is the preferred alternative for newcomers who want a Big Six bank relationship from day one—particularly valuable when applying for mortgages or large loans later.

What to do in the first 30 days:

- Apply immediately upon receiving your SIN (Social Insurance Number)

- Use the card for one recurring fixed expense only (transit pass, streaming subscription)

- Set up pre-authorized full-balance payment to eliminate interest risk

- Confirm the issuer reports to both Equifax and TransUnion before applying

Keep utilization below 30% of your limit at all times—FCAC guidance confirms high utilization is among the top factors suppressing newcomer credit scores.

Runner-Up: Credit Builder Loan (KOHO or a Credit Union)

If you prefer not to put down a security deposit, a credit builder loan through KOHO’s credit-building feature or a provincial credit union achieves the same bureau-reporting goal. You make fixed monthly payments into a secured account; the lender reports each payment as positive credit history. Upon completion, you receive the accumulated funds.

This approach pairs exceptionally well with building your broader financial foundation in Canada. As you establish credit, ensure your other newcomer priorities are addressed concurrently—including securing appropriate health insurance for newcomers in Canada, since provincial coverage gaps during waiting periods can create unexpected debt that undermines your credit-building progress.

Bottom line: Start with a secured card for speed and simplicity. Add a credit builder product in month three to diversify your credit mix—a factor TransUnion and Equifax both weight positively. Newcomers who follow this two-product approach consistently reach a 660+ score within 12–18 months, qualifying for unsecured cards, auto financing, and eventually mortgage pre-approval under standard OSFI-regulated B-20 stress test guidelines.

Frequently Asked Questions: Building Credit in Canada as a Newcomer

What is a credit score and why does it matter in Canada?

A credit score in Canada is a three-digit number ranging from 300 to 900, calculated by credit bureaus Equifax and TransUnion. It measures your creditworthiness based on payment history, credit utilization, account age, credit mix, and new inquiries. According to Equifax Canada, scores above 660 are generally considered “good.” Lenders, landlords, employers, and even utility providers use this score to assess risk. Without a Canadian credit history, newcomers face barriers securing apartments, phone contracts, and financing — making early credit-building a critical financial priority upon arrival.

Does my credit history from my home country transfer to Canada?

Generally, no. Canadian credit bureaus — Equifax and TransUnion — operate independently from international credit reporting agencies. Your credit history from India, the Philippines, Nigeria, or any other country does not automatically transfer. However, American Express offers a Global Transfer Program that allows cardholders from select countries to leverage existing history. Some major banks, including RBC through its RBC Newcomer Advantage program, may consider international banking relationships during application reviews. Regardless, expect to rebuild your credit profile from scratch after arriving in Canada.

What documents do newcomers need to start building credit in Canada?

To open a Canadian credit account, most financial institutions require:

- Government-issued photo ID (passport, PR card, or IRCC-issued documents)

- Social Insurance Number (SIN) — obtained from Service Canada

- Proof of Canadian address (utility bill, lease agreement, bank statement)

- Immigration status documentation (study permit, work permit, COPR, or PR card)

Some banks, including TD and Scotiabank, offer dedicated newcomer banking packages with reduced documentation requirements. Temporary residents on valid permits are eligible to apply. IRCC-recognized status documents are accepted across federally regulated financial institutions under OSFI oversight.

What is a secured credit card and how does it help newcomers?

A secured credit card requires a refundable cash deposit — typically $200–$500 — which becomes your credit limit. It functions identically to a regular credit card for purchases and, critically, reports payment activity to Equifax and TransUnion, building your credit file. Products like the Home Trust Secured Visa and Refresh Financial Secured Card are specifically accessible without existing Canadian credit history. Financial advisors recommend charging small recurring expenses (subscriptions, groceries) and paying the full balance monthly. After 12–18 months of responsible use, most issuers upgrade cardholders to unsecured products.

How long does it take to build a credit score in Canada from zero?

According to TransUnion Canada, a scoreable credit file typically requires at least one account open for six months and one account reporting within the past six months. Most newcomers receive their first credit score within 3–6 months of opening their first credit product. Achieving a “good” score (660+) generally takes 12–24 months with consistent, responsible behavior. Reaching “excellent” territory (750+) typically requires 2–3 years of diverse, well-managed accounts. The timeline accelerates with multiple credit products reporting simultaneously.

Should newcomers apply for a credit card or a credit-builder loan first?

Both instruments build credit effectively, but secured credit cards offer more flexibility and faster reporting cycles. A credit-builder loan — offered through institutions like Refresh Financial and certain credit unions — locks your payments into a savings account, returning funds at loan completion while reporting monthly to credit bureaus. Licensed financial planners often recommend a combined approach: open a secured card immediately, then add a credit-builder loan after 3–6 months to diversify your credit mix. Credit mix accounts for approximately 10% of your Equifax credit score calculation, rewarding multiple account types.

Can newcomers on a study or work permit build credit in Canada?

Yes. Temporary residents — including international students on study permits and workers on LMIA-approved or open work permits — are eligible to build Canadian credit. Banks including CIBC, BMO, and Scotiabank offer student and newcomer credit products accessible to non-permanent residents. IRCC-issued permits serve as valid identification for financial applications under FINTRAC’s client identification requirements. Newcomers report that starting immediately upon arrival — rather than waiting for PR status — provides a meaningful credit history advantage when eventually applying for mortgages or auto financing.

What credit mistakes should newcomers avoid?

Common credit-damaging behaviors include:

- Missing or late payments — the single most damaging factor (35% of score)

- High credit utilization — keeping balances above 30% of your limit signals risk

- Applying for multiple credit products simultaneously — each hard inquiry temporarily reduces your score

- Closing old accounts — reduces average account age and available credit

- Ignoring credit bureau errors — inaccuracies affect approximately 1 in 5 Canadian credit reports according to the Financial Consumer Agency of Canada (FCAC)

FCAC recommends reviewing your free annual credit reports at Equifax.ca and TransUnion.ca to monitor for errors immediately after opening your first account.

How does a Canadian credit score affect renting an apartment?

Landlords in most Canadian provinces are legally permitted to request credit checks as part of rental applications. Without a credit history, newcomers frequently face rejection or demands for larger deposits — sometimes equivalent to 2–3 months’ rent. The Residential Tenancies Act governs landlord-tenant relationships provincially, but credit screening practices are widespread. Newcomers report success by providing reference letters from international employers, proof of employment or enrollment, and prepaid rent offers to offset the absence of Canadian credit history. Building even a thin credit file within your first 6 months substantially improves rental application outcomes.

Does a Canadian bank account help build credit?

A bank account alone does not build credit because chequing and savings accounts are not reported to Equifax or TransUnion. However, maintaining a bank account is foundational: it demonstrates financial stability to lenders, enables automatic bill payments that prevent missed payments, and is required to access most credit products. Some fintech platforms, including Koho with its credit-building subscription feature, link spending accounts to credit-reporting mechanisms — a hybrid approach useful for newcomers avoiding traditional credit products. Opening a bank account should be your first financial step in Canada, followed immediately by a credit-building product.

Can newcomers use a co-signer to access credit faster in Canada?

Yes. A Canadian resident with established credit can co-sign on a credit card or loan application, effectively lending their creditworthiness to the newcomer applicant. Both parties’ credit files are affected by the account’s payment history. Federally regulated lenders under OSFI oversight accept co-signers for most retail credit products. This strategy is common among newcomers with family members already established in Canada. Financial advisors caution that co-signers assume full liability for missed payments, making open communication and a clear repayment agreement essential before proceeding.

What government or nonprofit resources exist to help newcomers understand credit in Canada?

Several regulated and government-backed resources support newcomer financial literacy:

- Financial Consumer Agency of Canada (FCAC) — free bilingual credit education tools at Canada.ca/fcac

- Credit Counselling Canada — nonprofit member agencies offering free counseling nationally

- Prosper Canada — financial empowerment programs targeting low-income newcomers

- Settlement.Org (Ontario) — plain-language credit guides for immigrants

- IRCC-funded settlement agencies — organizations like ACCES Employment and CultureLink provide financial orientation sessions

FCAC’s “Your Financial Toolkit” is specifically designed for newcomers and covers credit fundamentals, consumer rights under the Bank Act, and dispute resolution processes.

Conclusion

Building credit in Canada from zero is achievable — but it requires a deliberate, informed strategy rather than passive waiting.

Newcomers who start immediately with the right tools consistently reach a functional credit score (660+) within 6–12 months. The proven path combines a secured credit card or newcomer credit card with on-time payments, low utilization (under 30%), and at least one installment product like a credit-builder loan. Adding Equifax and TransUnion rent-reporting programs accelerates this timeline significantly.

Regulatory protections matter. Under the Financial Consumer Agency of Canada Act, federally regulated banks must offer fair access to financial products. Knowing your rights — and choosing FCAC-supervised institutions — protects you from predatory terms that target credit-invisible newcomers.

Key actions to take this week:

- Apply for a newcomer banking package (RBC, TD, Scotiabank, CIBC, or BMO all offer dedicated programs)

- Request your free credit report from Equifax Canada and TransUnion Canada

- Set up automatic minimum payments to eliminate missed-payment risk

- Track your score monthly through free tools like Borrowell or Credit Karma Canada

Avoid common mistakes: closing old accounts, co-signing too early, and applying for multiple credit products within 30 days.

Your Canadian credit history cannot be transferred from your home country — but it can be built faster than most newcomers expect. Start today, stay consistent, and your credit score will reflect the financial reliability you already possess.

Disclaimer

The information published on MoneyAbroadGuide.com is provided for general educational and informational purposes only. It does not constitute financial, legal, investment, or immigration advice. MoneyAbroadGuide.com is not a licensed financial advisor, mortgage broker, credit counsellor, or immigration consultant under any provincial or federal Canadian regulatory framework, including those governed by OSFI, FCAC, or provincial securities commissions.

Credit products, interest rates, eligibility requirements, and promotional offers referenced in this article are subject to change without notice. Always verify current terms directly with the financial institution or regulated provider before applying.

Affiliate Disclosure: This article may contain affiliate links or sponsored references to financial products. MoneyAbroadGuide.com may receive compensation if you apply for or obtain a product through links on this page. This compensation does not influence our editorial assessments, product rankings, or recommendations. We maintain strict editorial independence in accordance with our content integrity policy.

For personalized financial guidance, consult a licensed financial advisor or credit counsellor registered with a recognized Canadian regulatory body. For immigration-related financial obligations, consult a Regulated Canadian Immigration Consultant (RCIC) or licensed Canadian attorney.

About the Author

Talal Eddaouahiri is the founder of MoneyAbroadGuide.com, a financial information platform built specifically for newcomers, immigrants, and expats navigating the Canadian and American financial systems.

Drawing on firsthand experience as an immigrant and years of research into cross-border personal finance, Talal created MoneyAbroadGuide.com to fill a critical information gap: practical, regulation-aware financial guidance written for people starting from zero in a new country.

His work covers credit building, international money transfers, newcomer banking, tax compliance for newcomers (CRA), and immigrant-specific insurance — always with a focus on regulatory accuracy, FCAC and FINTRAC compliance context, and actionable guidance.

MoneyAbroadGuide.com is committed to editorial independence, factual accuracy, and the financial empowerment of Canada’s immigrant communities.

Last Updated: June 2026 | Tier: STANDARD | NEXUS-14 V5.0

About Talal Eddaouahiri

Founder & Editor of MoneyAbroadGuide.com. A Moroccan immigrant who settled in the United States in 2015, Talal opened bank accounts and built credit from zero in both the US and Canada. His background is in retail banking and customer relations, and he writes independent, source-based guides (FCAC, FINTRAC, OSFI, CRA, IRS, CDIC) to help newcomers navigate their first financial steps. Read his full profile →