Best Credit Cards For Newcomers In Canada: Complete Guide for Canada Immigrants (2026)

Quick Answer: The best credit cards for newcomers in Canada are secured cards and newcomer-specific unsecured cards that don’t require a Canadian credit history. Top picks include the Scotiabank Scene+ Visa, BMO CashBack Mastercard for newcomers, and the TD Cash Back Visa. Apply with your passport, SIN, and proof of status.

Moving to Canada means rebuilding your financial life from scratch — and your credit history doesn’t cross borders. Whether you arrived as a permanent resident, international student, or foreign worker under Immigration, Refugees and Citizenship Canada programs, Canadian lenders have no visibility into your overseas credit profile. That means most standard credit cards are immediately out of reach.

The good news: Canada’s major banks have responded with dedicated newcomer credit card programs that waive the Canadian credit history requirement entirely. These products let you start building a Canadian credit report and score from day one — which matters for everything from renting an apartment to qualifying for a mortgage later.

Before applying for any card, you’ll need foundational documents. A Social Insurance Number (SIN) is required to work and access government benefits in Canada, and most banks will ask for it during a credit card application. You’ll also benefit from having a Canadian bank account already open — and under FCAC banking rights, you are entitled to open a personal bank account regardless of employment status, making that a straightforward first step.

This guide covers the top credit cards available to newcomers in 2026, what documents you need, how secured versus unsecured newcomer cards compare, and the fastest strategy to build credit so you qualify for premium cards within.

1. Best Credit Cards For Newcomers In Canada

Canada’s major banks have built dedicated newcomer credit card programs specifically because international credit histories don’t transfer across borders. Without a Canadian credit file, even a high earner arriving from abroad starts from scratch — which is why these products waive the standard credit history requirement during an eligibility window (typically the first two years after landing, as noted above).

Why a Newcomer Card Matters First

A Canadian credit card does two jobs simultaneously: it lets you transact without carrying cash and it begins building the credit score you’ll need for a lease, car loan, or mortgage. According to the Financial Consumer Agency of Canada (FCAC), your Canadian credit report is separate from any foreign bureau file — lenders here can only see activity reported to Equifax Canada or TransUnion Canada. Starting with a newcomer card means your first months of on-time payments go directly onto that report.

For example, a newcomer who activates a secured or unsecured newcomer card within their first month and pays the full balance monthly can accumulate of positive payment history before most standard card applications even become viable —a meaningful head start on qualifying for premium travel or cashback products.

The Core Newcomer Card Lineup

The three most widely available programs are:

- Scotiabank Scene+ Visa — rewards on groceries and streaming; no annual fee in the newcomer tier; approval without Canadian credit history

- BMO CashBack Mastercard — flat cashback structure; suits newcomers who want simple, predictable rewards on everyday spending

- TD Cash Back Visa — tiered cashback; integrates cleanly with TD’s newcomer banking bundle

When weighed against each other, the Scotiabank and BMO options carry no annual fee, while the TD product offers a higher cashback rate on groceries, making it more valuable for larger households. All three report monthly to Canada’s major credit bureaus, which is the essential function at this stage.

Secured vs. Unsecured Newcomer Cards

Most newcomer programs above are unsecured — no deposit required. A secured card (where you deposit collateral equal to the credit limit) is a fallback if you arrive outside a bank’s newcomer eligibility window or hold a non-IRCC status that doesn’t qualify. Secured cards carry the same credit-building benefit but tie up cash; compare the opportunity cost before committing.

What to Watch

- Foreign transaction fees matter if you’re still sending money abroad or traveling internationally

- Credit limit at approval is often low; keep utilization of that limit to maximize score gains, per standard credit-scoring methodology

- Annual income reporting — according to CRA guidance for newcomers, you become a Canadian tax resident on arrival, so income declared to the card issuer should align with your actual Canadian income from landing date onward

2. What Are the Best Credit Cards for Newcomers in Canada and Why Do Immigrants Need Them?

The Credit History Gap — and Why It Costs Real Money

Canada’s credit system treats you as a financial stranger the moment you arrive, regardless of a spotless credit record abroad. Most lenders rely on Equifax Canada and TransUnion Canada bureaus (introduced earlier), and those bureaus hold no data on foreign histories. Without a Canadian file, landlords may demand larger deposits, cell providers may require prepaid plans, and lenders will price risk conservatively — meaning higher interest rates on any credit eventually granted.

Newcomer-specific cards exist precisely to break this cycle early. They accept applications with minimal or no Canadian credit history, report monthly to both bureaus, and begin generating the file that every subsequent lender will check.

Why the Card Type Chosen Now Has Long-Term Consequences

The card a newcomer opens first sets the foundation of their Canadian bureau file. According to the Financial Consumer Agency of Canada, your credit report includes the age of your oldest account — meaning the card opened in month one will still be improving your score years later. Opening the wrong product (or delaying) compresses that timeline permanently.

For example, a newcomer who opens BMO CashBack Mastercard or Scotiabank Scene in their first month will have of payment history on file before a peer who waited. When both later apply for a mortgage or car loan, that head start translates directly into qualification and rate differences.

Tax Residency Intersects With Credit Decisions

Newcomers become Canadian tax residents on the date of arrival, which means CRA obligations begin immediately. According to the Canada Revenue Agency’s newcomers page, filing a return — even for a partial year — can unlock credits and benefits like the GST/HST credit and Canada Child Benefit. Those benefits are deposited to a Canadian bank account, which in turn supports the banking relationship that most newcomer credit cards require for approval.

This connection is practical, not theoretical: card issuers such as BMO and TD verify a primary chequing relationship before approving unsecured newcomer products under their newcomer programs.

No-Cost Banking as the On-Ramp

According to the FCAC, newcomers in their first year are eligible for $0/month bank accounts under the FCAC commitment — removing the cost barrier to establishing the chequing relationship that most newcomer card programs require. Pairing a no-cost account with a no-fee newcomer card means a new arrival can begin building credit with zero recurring fixed costs in year one.

What Immigrants Actually Need From These Products

Beyond credit building, newcomer cards serve four practical functions simultaneously:

- Daily spending access without carrying cash in an unfamiliar country

- Purchase protection and fraud liability limits governed by the card network (Visa/Mastercard zero-liability policies)

- Proof of financial activity useful when renting or signing service contracts

- Rewards accumulation — products like Scotiabank Scene and TD Cash Back Visa generate value on routine grocery and transit spending from day one

The combination of bureau reporting, network protections, and immediate usability makes a newcomer credit card the highest-leverage financial tool available during the settlement period — ahead even of investment or savings products that require an established credit identity to access competitively.

3. Eligibility Requirements for Immigrants

Qualifying for a newcomer credit card in Canada is more straightforward than most immigrants expect — but the exact requirements differ meaningfully by product tier and immigration status.

Immigration Status and Document Requirements

Canadian banks generally accept the following as proof of status when applying for a newcomer credit card:

- Permanent Residents (PRs): Confirmation of Permanent Residence (COPR) or PR card

- Temporary Residents: Valid study or work permit (typically with at least six months remaining validity)

- Convention Refugees: Refugee Protection Claimant Document or Notice of Decision

- International students: Valid study permit plus proof of enrollment

Visitor visa holders are generally excluded from newcomer-specific programs. Applicants on an open work permit under the International Mobility Program qualify at most major banks, though product availability may vary by province.

Identity Verification: What Banks Actually Accept

According to the Financial Consumer Agency of Canada, banks are permitted to ask for two pieces of identification, and a SIN — as noted above — can be declined as ID for non-interest-bearing products. For credit card applications (which are interest-bearing), however, most lenders will require your SIN for credit bureau access.

Accepted primary ID typically includes:

- Canadian passport or foreign passport with valid immigration document

- Provincial photo ID or driver’s licence (once obtained)

- Government-issued immigration documents (COPR, study/work permit)

Residency for Tax Purposes Intersects With Approval

Immigrants become Canadian tax residents on arrival, according to the CRA. While banks do not require a filed tax return to approve a newcomer card, your tax residency status affects whether you’ll be issued a T4 or receive benefits like the GST/HST credit — and lenders may factor declared income and benefit income into credit limit decisions.

For example, a newcomer who receives the GST/HST credit (as noted above) can legitimately include that as declared income on a credit application, which may modestly increase the approved credit limit on an entry-level card.

Minimum Income and Credit Score Thresholds

This is where newcomer-specific products differ from standard cards: most programs waive the minimum credit score requirement entirely for eligible newcomers within a defined arrival window. Income requirements are also reduced or eliminated at the secured and entry-level unsecured tiers. Premium rewards cards —those not marketed specifically to newcomers —typically require a minimum personal income and an established Canadian credit file, neither of which most recent arrivals possess.

Provincial Variations Worth Knowing

Quebec residents face minor differences: provincial consumer protection legislation under the Consumer Protection Act (administered by the Office de la protection du consommateur) requires French-language disclosures on all credit agreements. This does not restrict eligibility but means application documents and cardholder agreements must be requested in French if preferred.

Arrival Window Matters

Most newcomer programs — including those from Scotiabank Scene+ and BMO CashBack Mastercard referenced above — define eligibility by time since landing, typically the first two to five years. Applicants who have been in Canada longer and still lack a credit file may need to start with a secured card rather than a newcomer-specific unsecured product.

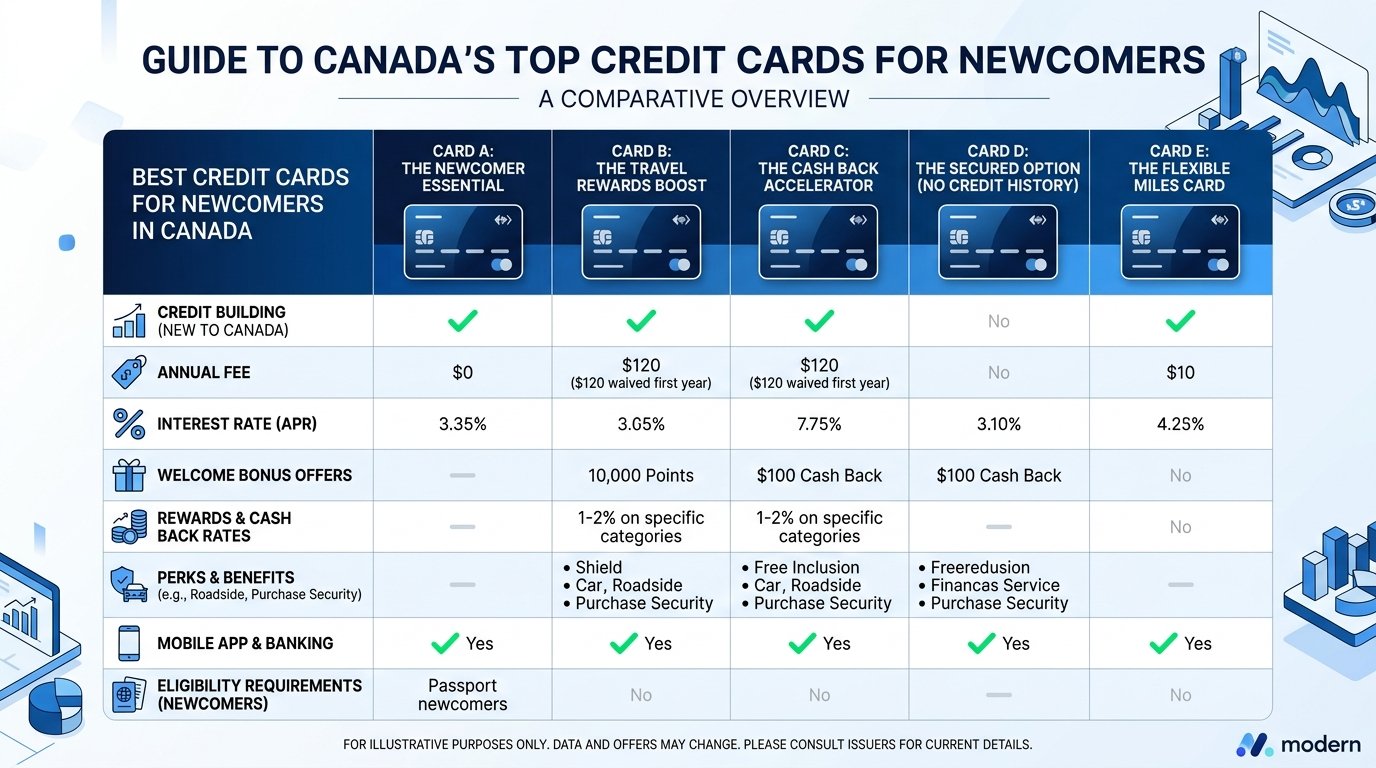

Comparing the Best Credit Cards for Newcomers in Canada

Choosing a first Canadian credit card means weighing annual fees, rewards rates, and whether the issuer waives the standard credit history requirement for newcomers. The table below covers the primary options available to immigrants and newcomers across major Canadian financial institutions. Annual fees and rewards structures vary by provider and are subject to change; confirm current terms directly with each issuer before applying.

| Card | Annual Fee | Rewards / Cash Back | Newcomer Program | Security Deposit Required |

|---|---|---|---|---|

| Scotiabank Scene+ Visa | varies by provider — confirm directly | Scene+ points on everyday purchases | Yes — waives foreign credit history requirement | No |

| BMO CashBack Mastercard | varies by provider — confirm directly | Cash back on groceries and recurring bills | Yes — newcomer-specific application stream | No |

| TD Cash Back Visa | varies by provider — confirm directly | Cash back on groceries and gas | Yes — available to eligible newcomers | No |

| CIBC Aventura Visa | varies by provider — confirm directly | Aventura travel points | Available to qualifying newcomers | No |

| Home Trust Secured Visa | varies by provider — confirm directly | None | Accepts applicants without Canadian credit history | Yes — refundable deposit |

| Capital One Guaranteed Mastercard | Varies | Limited rewards | Available regardless of credit history | Yes — refundable deposit |

Secured cards from providers like Home Trust accept newcomers without any established Canadian credit history, making them a practical fallback when unsecured applications are declined. Under the FCAC’s no-cost account framework, eligible newcomers within their first year can access $0/month banking — pairing a no-fee account with a no-fee newcomer credit card keeps initial costs minimal while building a local credit profile recognized by Equifax Canada and TransUnion Canada.

Illustrative Scenarios

The following are illustrative scenarios, not real testimonials or case studies of specific individuals.

Illustrative Scenario: Convention Refugee Claimant, Early Settlement Period

A convention refugee claimant, newly arrived and without established Canadian credit history, applies for a secured newcomer card. Without a Canadian credit file, unsecured options typically remain unavailable — illustrating why newcomer-specific products exist.

Expert Recommendation

Top Pick: Scotiabank Scene+ Visa for Newcomers

For most newcomers arriving in Canada, the Scotiabank Scene+ Visa stands out as the strongest starting point. Scotiabank’s dedicated newcomer program removes the Canadian credit history requirement that typically blocks immigrants from accessing unsecured cards — a meaningful structural advantage when you are building your financial profile from scratch.

The card earns Scene+ points on everyday purchases, carries no annual fee in its entry tier, and feeds directly into a credit bureau report with both Equifax Canada and TransUnion Canada from the first billing cycle. That early reporting matters: the length and consistency of your credit file compounds over time, and a card opened in month one of your arrival will anchor your history years before a delayed application would.

From a regulatory standpoint, Scotiabank operates under OSFI oversight and its newcomer products are marketed in compliance with FCAC guidelines — the same federal body that maintains no-cost and low-cost account commitments for new arrivals. Pairing the Scene+ card with one of those no-fee accounts gives newcomers a coordinated, low-cost entry into Canada’s credit system.

Best suited for: Permanent residents, Convention Refugees, and eligible temporary residents who want an unsecured card with rewards from day one.

Runner-Up: BMO CashBack Mastercard for Newcomers

The BMO CashBack Mastercard earns its runner-up position through a straightforward cash-back structure that many newcomers find easier to track than points programs. BMO’s newcomer stream similarly waives the standard Canadian credit history requirement, and cash back credited directly to your statement is immediately tangible — no points conversion required.

Where the BMO card edges ahead for some profiles is flexibility: cash returned to your account offsets any purchase category, which suits newcomers whose spending patterns shift significantly in the first year as they settle housing, transportation, and employment arrangements.

One practical note: As you accumulate CRA filing obligations — newcomers establish Canadian tax residency on arrival, as outlined on the CRA newcomers page — having a credit card that generates a clear dollar-amount return simplifies year-end personal finance tracking.

Best suited for: Newcomers who prefer straightforward cash value over travel or retail rewards, and those managing variable early-settlement expenses.

Bottom Line

Both cards are legitimate, FCAC-supervised instruments for building Canadian credit without prior history. Choose Scene+ if you value rewards accumulation; choose BMO CashBack if simplicity and direct cash return matter more. Either decision made promptly after arrival will serve your long-term credit profile better than waiting.

FAQ: Best Credit Cards for Newcomers in Canada

Can I get a credit card in Canada if I just arrived and have no Canadian credit history?

Yes. Several major banks offer newcomer-specific programs that waive the Canadian credit history requirement entirely. Scotiabank, BMO, TD, and RBC each maintain dedicated newcomer banking streams. Eligibility windows and documentation vary by institution, but most accept your Confirmation of Permanent Residence, a valid passport, and government-issued photo ID. Approval is typically possible within days of arrival. These programs exist precisely because lenders recognize that an absence of Canadian credit history does not reflect creditworthiness — it reflects geography.

Which documents do I need to apply for a newcomer credit card?

Requirements vary by lender, but commonly accepted documents include a valid passport, Confirmation of Permanent Residence (COPR) or work permit, proof of Canadian address, and a Social Insurance Number. For non-interest-bearing accounts, you may decline to provide your SIN as identification, though most credit card applications will request it for credit bureau reporting purposes. Refugee claimants may present a Refugee Protection Claimant Document in lieu of permanent residence documentation.

Should I choose a secured or unsecured newcomer credit card?

If a bank’s newcomer program offers an unsecured card, take it — it avoids tying up a cash deposit. Secured cards (which require a refundable deposit as collateral) are a strong fallback if you fall outside a newcomer program’s eligibility window or arrive on a permit type not covered. Both product types report to Equifax Canada and TransUnion Canada, so both build Canadian credit history. The key metric is whether the card reports monthly, not whether it is secured.

How quickly will I build a credit score after getting my first Canadian credit card?

Credit scoring agencies generally require several months of payment history before generating an initial score. Paying your statement balance in full each month, keeping utilization low, and avoiding missed payments are the fastest levers available. Opening additional credit products too quickly can temporarily lower your score. Consistent, on-time payment behaviour over time is what lenders weight most heavily — there is no shortcut that bypasses the passage of time.

Do newcomer credit cards charge foreign transaction fees?

Most standard newcomer cards do charge a foreign transaction fee — typically around a small percentage per transaction in a non-Canadian currency. If you frequently send money abroad or shop in USD or other currencies, look specifically for no-foreign-transaction-fee cards, which are available in Canada but are less common among entry-level newcomer products. Compare this fee explicitly before applying if cross-border spending is a regular part of your financial life.

Will my Canadian credit card affect my taxes as a newcomer?

The card itself does not trigger tax obligations, but your broader financial situation does. Newcomers become Canadian tax residents from their date of arrival, which means worldwide income may be reportable to the Canada Revenue Agency from that point forward. Credit card cashback and rewards are generally not considered taxable income in Canada. Consulting a licensed tax professional familiar with newcomer tax residency rules is advisable in your first year.

Are there no-cost banking options I should open alongside my credit card?

Yes — and doing so is strongly recommended. Under a commitment overseen by the Financial Consumer Agency of Canada, newcomers in their first year qualify for no-monthly-fee bank accounts at participating institutions. Pairing a no-fee chequing account with a newcomer credit card gives you a functional two-product credit profile from day one, which lenders view more favourably than a credit card held in isolation.

What credit limit can I realistically expect on a first newcomer card?

Initial credit limits on newcomer unsecured cards are typically modest — lenders are extending credit without Canadian repayment history to reference. Limits on secured cards are usually equal to the deposit provided. After demonstrating consistent repayment behaviour over several months, most issuers allow credit limit increase requests, and some conduct automatic reviews. Avoid requesting increases before you have established a clear payment record, as multiple hard inquiries can reduce your score.

Can temporary residents, not just permanent residents, qualify for newcomer credit cards?

Yes, though program terms differ. Many banks extend newcomer credit products to holders of open work permits under the International Mobility Program and to some study permit holders. Refugee claimants and Convention Refugees are also accommodated by certain institutions. The eligibility window — the period after arrival during which the newcomer program applies — varies by lender and immigration status, so confirm your specific permit category with the bank before applying.

What mistakes do newcomers most commonly make with their first Canadian credit card?

The most consequential errors are carrying a balance month-to-month (triggering interest charges that erode any rewards earned), missing a payment deadline, and applying for multiple cards simultaneously. Each application typically triggers a hard credit inquiry. A single card, used regularly for everyday purchases and paid in full each statement cycle, builds credit efficiently without unnecessary cost or risk. Newcomers who treat the first card as a credit-building tool — rather than a spending vehicle — consistently report stronger credit profiles within their first few years in Canada.

Conclusion

Choosing the right credit card as a newcomer to Canada is one of the most consequential early financial decisions you will make. The card you open in your first months shapes the credit profile that will follow you through future applications for apartments, auto loans, and eventually a mortgage.

The key takeaway: start with a product explicitly designed for newcomers — one that waives the Canadian credit history requirement — then build from there. As covered earlier, major banks including Scotiabank, BMO, and TD offer dedicated newcomer programs with no annual fee options and graduated credit limits. Once your credit profile has seasoned, you can move to premium rewards products that reflect your actual spending needs.

Keep three principles in mind as you move forward. First, banking and credit are separate foundations — a no-cost newcomer bank account builds transactional history while your credit card builds your credit file; both matter. Second, as your income and tax residency situation stabilizes with the CRA, your eligibility for income-gated premium cards will expand. Third, regulated providers operating under FCAC oversight offer meaningful consumer protections — favour them.

Canada’s credit system rewards consistency, low utilization, and time. The newcomer cards reviewed in this guide are the appropriate starting point. Use them deliberately, pay balances in full, and upgrade strategically. Your future financial self will benefit from the groundwork you lay today.

Disclaimer

Editorial Independence: MoneyAbroadGuide.com is an independent financial information platform. The content in this guide is produced for informational purposes only and does not constitute financial, legal, or tax advice. Readers should consult a licensed financial advisor, regulated credit counsellor, or qualified tax professional before making financial decisions.

Affiliate Disclosure: This article may contain affiliate links to financial products. If you apply for a credit card or other product through a link on this page, MoneyAbroadGuide.com may receive compensation from the issuing institution. This compensation does not influence editorial rankings, card selections, or the information presented. Our editorial process remains independent of commercial relationships.

Accuracy & Currency: Financial products, interest rates, fees, eligibility criteria, and promotional offers change frequently. All details — including card benefits and program terms — should be independently verified directly with the issuing bank before applying. MoneyAbroadGuide.com makes no representations regarding the completeness or ongoing accuracy of third-party product information.

Regulatory Note: Credit products in Canada are subject to oversight by the Financial Consumer Agency of Canada (FCAC) and applicable provincial consumer protection legislation. Your rights as a consumer are protected under these frameworks.

Last reviewed for accuracy: 2026.

About the Author

Talal Eddaouahiri is the founder of MoneyAbroadGuide.com, an independent financial information platform for immigrants and newcomers in the United States and Canada. Originally from Morocco, he settled in the U.S. in 2015 and built his own credit history and banking relationships from scratch in both countries. His background is in retail banking and customer relations, and he draws on that firsthand experience to write independent, source-based guides — citing regulators including the FCAC, FINTRAC, OSFI, CRA, IRS, and CDIC — to help newcomers navigate financial systems with confidence.

Last Updated: July 2026

About Talal Eddaouahiri

Founder & Editor of MoneyAbroadGuide.com. A Moroccan immigrant who settled in the United States in 2015, Talal opened bank accounts and built credit from zero in both the US and Canada. His background is in retail banking and customer relations, and he writes independent, source-based guides (FCAC, FINTRAC, OSFI, CRA, IRS, CDIC) to help newcomers navigate their first financial steps. Read his full profile →