Best Mortgage For Newcomers To Canada: Complete Guide for Canada Immigrants (2026)

Quick Answer: Newcomers to Canada can qualify for a mortgage through newcomer-specific programs at major banks, credit unions, and monoline lenders. CMHC’s Newcomers mortgage loan insurance supports many of these applications by allowing foreign credit history and non-traditional income documentation, but individual lenders — not CMHC — decide eligibility. Permanent residents, temporary workers, and some international students may all qualify, with requirements varying by immigration status and lender.

Buying a home is one of the most significant financial decisions you will make after arriving in Canada — and for many newcomers, it feels out of reach. No Canadian credit history. Limited employment records. Unfamiliar documents. These barriers are real, but they are not insurmountable.

Canada’s mortgage market has evolved to serve immigrants and newcomers. Major federally regulated lenders, overseen by the Financial Consumer Agency of Canada (FCAC), now offer newcomer-specific mortgage programs. CMHC Newcomers is a real, named mortgage loan insurance product — but CMHC does not lend directly or approve individual applications. It insures eligible mortgages that lenders originate, which is what lets those lenders accept foreign credit history and non-traditional income in place of a conventional Canadian credit file. Each lender sets its own newcomer program rules within that insurance framework.

Your immigration status — permanent residency, work permit, or study permit — directly shapes which programs you can access, your down payment, and what documentation lenders require in place of a Canadian credit history. According to IRCC, Canada welcomes hundreds of thousands of new permanent residents each year, making this one of the most consequential financial topics for the immigrant community.

Before approaching a lender, two foundational steps matter: obtaining your Social Insurance Number and beginning to build a Canadian credit profile. As the FCAC notes, your credit history in your home country does not automatically transfer — many newcomers start from zero, which affects mortgage qualification.

This guide walks through eligibility by immigration status, how CMHC mortgage insurance supports newcomer applications, down payment requirements, documentation alternatives, lender comparisons, common mistakes, a step-by-step timeline, and the steps to take before you apply.

1. Best Mortgage For Newcomers To Canada: Quick Overview

Canada’s housing market presents a layered challenge for newcomers: lenders assess risk differently when you lack Canadian credit history, domestic employment records, or permanent residency documentation. Understanding which mortgage products are actually available to you — and which institutions actively compete for newcomer borrowers — is the fastest path to a realistic purchase timeline.

Who Qualifies as a “Newcomer Borrower”

Canadian lenders generally apply newcomer mortgage criteria — often supported by CMHC’s Newcomers mortgage insurance — to:

- Permanent residents, typically within their first several years after landing (the exact window is set by each lender’s own newcomer program, so confirm current eligibility directly)

- Non-permanent residents (work permit or study permit holders) with valid status

- Protected persons and convention refugees

Each category carries different down payment thresholds, insurer requirements, and income documentation rules. Lenders applying OSFI’s Guideline B-20 minimum qualifying rate stress-test all insured and uninsured applications, newcomers included — currently the greater of the contract rate plus 2%, or a 5.25% floor, reviewed by OSFI at least annually. Confirm the current figure before budgeting around it.

The Core Lender Landscape in 2026

Four institution types actively serve newcomer borrowers in Canada:

- Big Six banks (RBC, TD, Scotiabank, BMO, CIBC, National Bank) — each maintains a newcomer banking program that can bundle a mortgage product with credit-building accounts

- Credit unions — provincially regulated; often more flexible on international income documentation

- Monoline lenders — broker-distributed, competitive fixed rates, but typically require stronger Canadian credit indicators

- Alternative/B lenders — higher rates, useful for newcomers with irregular employment; regulated as mortgage investment entities under provincial securities law

Documentation Lenders Typically Require

Beyond standard proof of income and assets, newcomer-specific documentation commonly includes:

- Valid immigration document (PR card, work permit, study permit)

- Passport and, where applicable, the entry visa

- International credit bureau report (Equifax or Experian equivalents from your country of origin)

- Two years of foreign tax returns or employer letters (translated and notarized)

- Three to six months of Canadian bank statements showing settlement funds

Newcomers becoming Canadian residents for tax purposes on arrival — according to the CRA newcomers page — may need to show filing compliance even for a partial tax year, which some lenders treat as supplementary income verification.

Fixed vs. Variable Rate Considerations for Newcomers

There is no universally correct choice between fixed and variable — it depends on income stability, risk tolerance, expected length of stay, and your view on rate direction. Fixed-rate mortgages typically carry larger early-break penalties (Interest Rate Differential); variable-rate mortgages generally cap break penalties at three months’ interest. Newcomers relocate domestically more often in their first years, according to IRCC settlement data — worth weighing, not a reason to default to either product. Discuss your circumstances with a licensed mortgage professional before deciding.

2. What Is a Mortgage for Newcomers to Canada and Why Do Immigrants Need It?

Canada’s housing market operates under a distinct legal and financial framework that differs substantially from most countries of origin. A newcomer mortgage is not a separate loan product in the conventional sense — it is a category of underwriting accommodation that allows lenders to assess creditworthiness using alternative evidence when a standard Canadian credit history does not yet exist.

Why Standard Mortgage Underwriting Fails New Arrivals

Canadian lenders rely on credit bureau data from Equifax or TransUnion Canada to evaluate repayment risk. Immigrants arriving with strong financial records from their home country — years of on-time payments, real estate ownership, or stable employment — start with a thin or empty Canadian credit file. According to the Financial Consumer Agency of Canada, credit history in Canada is tracked separately from any foreign record, meaning a new arrival is effectively invisible to automated mortgage adjudication regardless of their actual financial discipline. Without adapted underwriting criteria, this would systematically exclude otherwise creditworthy immigrants from homeownership simply due to recency of arrival — not financial risk.

The Economic Case for Homeownership Access

Newcomers become Canadian tax residents on arrival and, according to the CRA, begin accruing tax obligations immediately. Building equity through homeownership is a tax-efficient wealth-building tool in Canada — principal residence capital gains remain exempt from CRA taxation. Accessing a mortgage earlier can mean more years of equity accumulation, though this depends on local market conditions and is not a guarantee of appreciation; values can also decline, and the trade-off should be weighed against your own risk tolerance.

How CMHC’s Newcomers Insurance Bridges the Gap

The accommodation works by substituting Canadian credit history with verifiable proxies: foreign credit bureau reports, rental payment records, international banking statements, and employer letters, letting underwriters construct a behavioural credit picture despite the absence of domestic bureau data. CMHC Newcomers mortgage loan insurance formalizes this at the insurer level, signalling to lenders that alternative documentation meets CMHC’s threshold. The lender still makes the final underwriting decision; CMHC insures the loan, it does not originate it.

Tax Residency and Financial Identity

Alongside mortgage qualification, immigrants build a Canadian financial identity simultaneously across multiple systems — credit bureaus, CRA, and banking. According to FCAC, newcomers have the right to open a personal bank account without a job or an initial deposit, a practical first step toward the banking history mortgage lenders will later scrutinize.

Opening a bank account shortly after arrival and maintaining consistent account activity creates a paper trail that lenders treat as supplementary evidence of financial stability. See our guide to the best newcomer bank accounts in Canada for a full walkthrough.

3. Eligibility Requirements for Immigrants

Lender eligibility criteria for newcomer mortgages split across four dimensions: immigration status, income verification, credit standing, and down payment sourcing.

Immigration Status Tiers

Permanent Residents (PRs): Qualify for the full range of insured and conventional mortgage products on the same terms as citizens. A valid PR card or Confirmation of Permanent Residence is the primary status document lenders require.

Temporary Foreign Workers and International Students: Eligible under select lender-specific newcomer programs and, in some cases, CMHC-insured products, provided they hold a valid work or study permit with a remaining validity period that covers at least part of the mortgage term. Lenders typically require proof the permit is renewable or that PR sponsorship is underway.

Foreign Nationals (non-residents): Subject to stricter underwriting — most institutional lenders require a conventional (uninsured) mortgage, a larger down payment, and additional stress-testing beyond the OSFI Guideline B-20 threshold described above.

Income and Employment Verification

- Salaried employees: A Canadian employment offer letter or pay stubs covering several months, plus a foreign employment reference letter, satisfy most Big Six lender requirements.

- Self-employed newcomers face the steepest documentation burden. Without two years of Canadian Notice of Assessment from the CRA, lenders typically require several years of foreign business financials and an accountant’s letter. Early CRA registration helps build that trail quickly.

- Foreign income: Many CMHC-insured programs accept foreign-sourced income converted at a recognized exchange rate and supported by two years of foreign tax returns — confirm acceptance with your lender, as practice varies.

Credit History Requirements

Lenders require either a Canadian credit file or acceptable substitute evidence — acceptance of foreign credit documentation varies by lender, with no industry-wide rule. Common alternatives: international credit bureau reports (Equifax Global, Nova Credit for select countries), proof of on-time rent/utility/foreign-loan payments, and a Canadian bank account open for several months showing consistent deposits. According to FCAC, Canadian credit files are maintained by Equifax and TransUnion Canada; newcomers should begin building one immediately, typically with a secured card — see our guide to the best credit cards for newcomers in Canada.

Down Payment Sourcing Rules

Down payment funds must be verifiable regardless of origin. Lenders require a paper trail for Canadian-held funds; for foreign-sourced funds, most require conversion records, wire transfer documentation, and confirmation that funds are not borrowed. If you’re moving savings from abroad, our guide to the cheapest ways to send money to and from Canada compares transfer options. Gift letters from immediate family are generally accepted but must state no repayment is required — a FINTRAC compliance requirement.

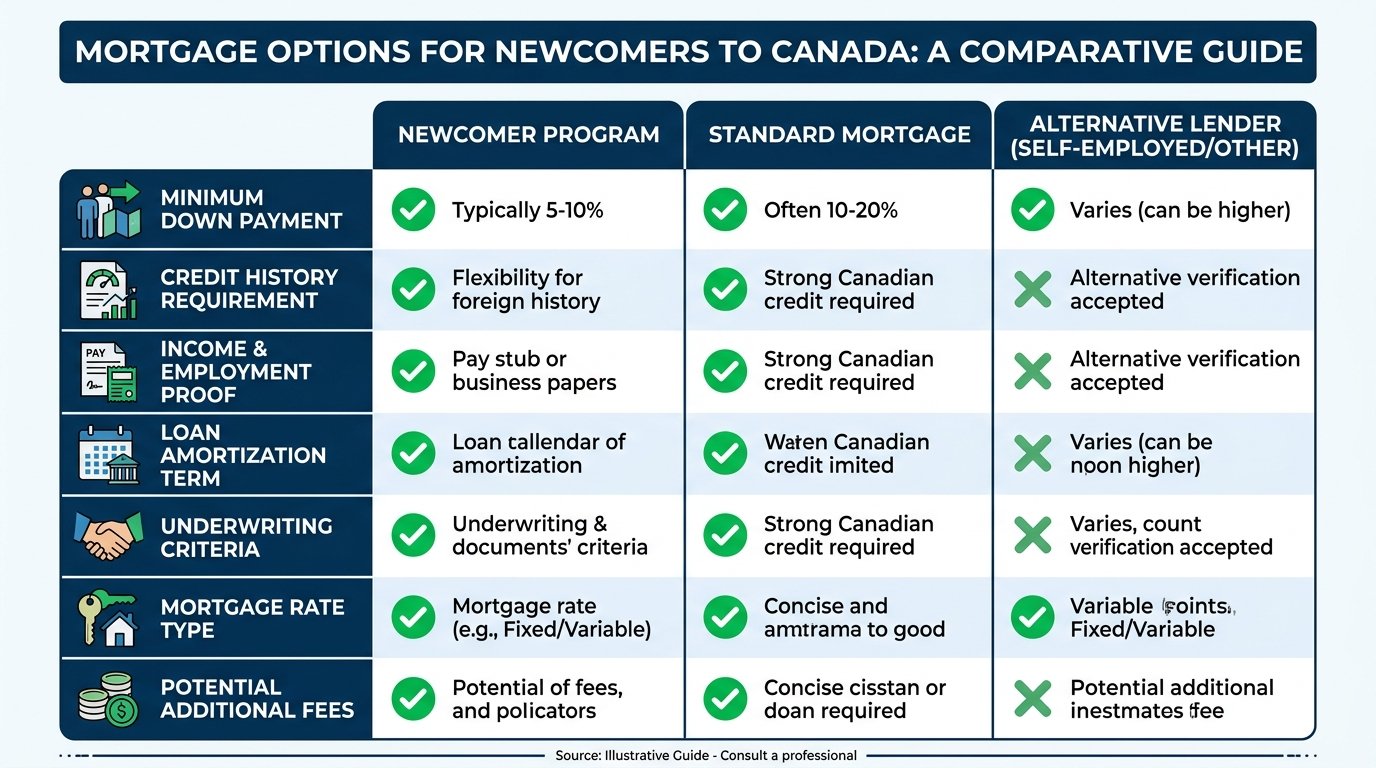

Comparing Newcomer Mortgage Programs in Canada

Choosing the right path hinges on your immigration status, time in Canada, and available documentation. Underwriting criteria shift by institution, so treat the figures below as directional, not guarantees.

| Program / Feature | CMHC-Insured (via a participating lender) | Big-Six Bank Newcomer Program | Credit Union / Monoline Lender | Private / Alternative Lender |

|---|---|---|---|---|

| Primary eligibility | Permanent Residents; some Temporary Residents, per CMHC Newcomers criteria | Typically PR; select programs for work-permit holders | Varies by province; often more flexible on status | Most immigration statuses accepted |

| Minimum down payment | Set by CMHC’s insurance rules; varies by residency duration | Varies by internal policy and status tier | Often competitive with bank offerings | Generally higher than insured programs |

| Newcomer-specific flexibility | Foreign credit/income accepted per CMHC’s documented criteria | Varies by bank; often includes dedicated newcomer advisors | Varies by institution | Broadest flexibility, higher cost of capital |

| Foreign income accepted | Yes, subject to CMHC documentation rules | Sometimes, confirm with the specific bank | Often, especially at credit unions | Usually, with more documentation discretion |

| Online pre-approval | Depends on the originating lender’s own platform | Varies by bank; several offer digital tools | Varies | Less commonly available online |

| Multilingual support | Not applicable (CMHC insures; does not advise borrowers directly) | Varies by branch and market; larger urban branches more likely to offer it | Varies by institution | Varies, often broker-mediated |

| Credit history requirement | Canadian credit or documented foreign equivalent, per CMHC rules | Usually requires established or alternative Canadian credit | May accept international credit references | Minimal credit history often acceptable |

| Mortgage insurance required | Yes — this is the CMHC-insured category | Yes, if below the conventional down payment threshold | Depends on loan-to-value ratio | Usually not CMHC-insured; lender bears the risk |

| Tax residency consideration | Newcomers become Canadian tax residents on arrival — CRA guidance applies | Same CRA obligations apply to all borrowers | Same | Same |

Common Mistakes Newcomers Make

Newcomer mortgage files fail or stall for predictable, avoidable reasons, based on the lender documentation and OSFI underwriting rules described throughout this guide:

- Applying too early, before you have Canadian bank or employment history — this can leave a hard credit inquiry on a file with little else to show.

- Underestimating the down payment. Newcomer and non-resident categories can require more than a standard insured mortgage; confirm the actual minimum for your status before house-hunting.

- Ignoring closing costs. Land transfer tax, legal fees, title insurance, and appraisal costs are separate from the down payment and frequently underbudgeted.

- Assuming foreign credit history transfers automatically. According to FCAC, Canadian credit files are built independently of any foreign record.

- Consulting only one lender. Newcomer program terms vary meaningfully by institution; comparing several — or using a broker who can — helps you find the program that fits.

- Skipping pre-approval, which makes it hard to know your realistic price range before making an offer.

Expert Tips

These recommendations reflect patterns in how lenders evaluate newcomer files, drawn from the underwriting rules and documentation standards described throughout this guide.

- Get pre-approved before you shop — a pre-approval typically holds your quoted rate for a fixed window; confirm the exact period with your lender.

- Start Canadian credit-building immediately. A secured card used consistently for a few months gives lenders a genuine Canadian data point that can change which lender tier you qualify with.

- Prepare foreign documentation in advance. Certified translations and notarization can take time to arrange — starting early avoids delays at underwriting.

- Compare the full cost, not just the headline rate. Where mortgage insurance applies, the premium is added to the loan or paid upfront; factor it into your lender comparison.

- Self-employed newcomers should start the documentation trail early. Two years of Notice of Assessment (or the foreign equivalent plus an accountant’s letter) is the single largest source of delay.

- Work with a broker who documents newcomer-file experience specifically, not general mortgage experience — the underwriting nuances are a distinct skill set.

Step-by-Step Timeline

There is no fixed timeline that applies to every newcomer, since it depends on your immigration status, income situation, and how quickly you assemble documentation. The sequence below reflects the order most lenders expect, not a guaranteed schedule.

- Before arrival: Gather foreign credit bureau reports, employer reference letters, and tax records; research which lenders and newcomer programs serve your intended province.

- Week 1: Apply for your Social Insurance Number and open a Canadian bank account to start your deposit and transaction history.

- Month 1: Open a secured credit card if available to you, and set up a first meeting with a bank advisor or licensed mortgage broker experienced with newcomer files.

- Month 3: Continue building Canadian bank statement history; assemble foreign income and credit documentation with certified translations if needed; discuss pre-approval eligibility.

- Month 6: With several months of Canadian employment and banking history in place, many newcomers are positioned to seek pre-approval, depending on lender-specific requirements.

- Year 1: Canadian credit history is more established; CRA tax filing history (if applicable) supports income verification; this is when many newcomer-program applications move from pre-approval to a completed purchase, though individual timelines vary widely.

Documents Checklist

| Situation | Required Documents | Supporting Materials | Helpful Notes |

|---|---|---|---|

| All applicants | Valid immigration document (PR card, work/study permit), passport | Entry visa where applicable | Confirm your document’s remaining validity covers at least part of the mortgage term |

| Salaried employees | Canadian employment offer letter or recent pay stubs | Foreign employment reference letter | A few months of Canadian pay history strengthens most applications |

| Self-employed | Foreign business financials, accountant’s letter | Two years of Canadian Notice of Assessment once available | Start assembling this documentation well before applying — it is the slowest piece to gather |

| Foreign income | Two years of foreign tax returns or bank statements | Currency conversion documentation | Confirm with your lender whether foreign income is accepted — this varies |

| Credit history | International credit bureau report (Equifax Global, Nova Credit where available) | Proof of on-time rent, utility, or foreign loan payments | A Canadian secured card with a short track record can supplement a thin foreign-credit file |

| Down payment | Proof of funds (Canadian or foreign, with a documented paper trail) | Wire transfer records; gift letter if applicable (must state no repayment required) | FINTRAC anti-money-laundering rules apply to all down payment sourcing |

| Tax residency | CRA registration/filing once resident for tax purposes | Notice of Assessment once filed | Some lenders request this as supplementary income verification |

Illustrative Scenarios

The following are illustrative scenarios, not real testimonials or case studies of specific individuals.

Illustrative Scenario: Temporary Foreign Worker, Employer-Sponsored Work Permit

A temporary foreign worker with a valid employer-sponsored permit approaches a federally regulated lender. Without established Canadian credit history, the lender requests foreign bureau records and a larger down payment, demonstrating how immigration status tier directly shapes the underwriting path applied.

Expert Recommendation

The picks below are our own editorial assessment, not an official ranking. We weighed newcomer-specific flexibility, branch/advisor network reach, multilingual support, and integration with everyday banking — not a comprehensive market survey of every lender’s rates.

🏆 Editorial Pick: RBC

In our assessment, RBC’s newcomer-focused banking and mortgage services are among the more accessible entry points for recent arrivals — generally structured to accept international credit references and non-traditional income documentation such as employer letters and foreign pay stubs. Confirm current details directly with RBC, as offerings change. Multilingual support is more available at major urban branches, and an established banking relationship — even a short one — is something lenders generally view favourably. Under FCAC’s commitments, eligible newcomers within their first year can access no-fee personal accounts at participating institutions.

🥈 Runner-Up: TD New to Canada Banking Package

TD’s New to Canada Banking Package is a real, named offering — publicly advertised at up to $1,790 in combined value for permanent residents, international students, and temporary residents. TD’s published mortgage guidance shows down payment minimums varying by status: roughly 35% for PRs within about five years of landing, 20% for work-permit holders, or as low as 5% on purchases under $1.5 million under a more flexible option. Confirm current figures directly with TD, as these are set internally and can change. TD is a strong alternative for newcomers with an existing relationship through its international banking partnerships, and its mortgage advisors have documented experience with IRCC status documentation.

Bottom Line

RBC’s newcomer banking ecosystem and TD’s documented New to Canada package are both reasonable starting points — neither is a universal fit. Your immigration status, income documentation, and down payment capacity determine which lender’s rules actually work for your file. A licensed mortgage broker who specialises in newcomer files can also access monoline lenders whose credit policies may suit your circumstances more precisely.

Frequently Asked Questions: Mortgage for Newcomers to Canada

Can I get a mortgage in Canada without permanent residency?

Yes. Temporary residents — work permit holders, international students, and certain visa categories — may qualify under lender-specific newcomer programs, though conditions are stricter: a valid permit with meaningful remaining validity, active Canadian income, and a larger down payment are typically required. Speak with a licensed mortgage broker who specialises in newcomer files before applying.

Do I need a Canadian credit history to qualify?

Not necessarily. Several major lenders accept alternative documentation — foreign credit bureau reports, international bank reference letters, or proof of consistent rent and utility payments — though acceptance varies by lender with no single industry-wide standard. Building even a short Canadian credit history through a secured card before applying can improve your approval odds.

Which government program specifically supports newcomer mortgages?

CMHC Newcomers is the primary federal instrument. It is mortgage loan insurance, not a direct loan: it lets participating lenders offer financing with a smaller down payment to eligible newcomers. CMHC sets documentation standards; lenders decide whether to approve a given application within those rules. Provincial programs may layer on top — check with your provincial housing authority.

What documents should I gather before approaching a lender?

Proof of immigration status, passport, employment letter, recent pay stubs, foreign bank statements, and a record of assets or liabilities. If your employer is outside Canada, a letter from the foreign company is often required. See the Documents Checklist above for a fuller breakdown.

Does opening a Canadian bank account help my mortgage application?

It can — and it costs nothing at participating institutions under the FCAC’s no-cost account commitment for newcomers in their first year. Establishing this history early is something lenders generally view favourably alongside your other documentation.

How does my down payment size affect mortgage eligibility as a newcomer?

A larger down payment reduces lender risk, offsets a thin credit profile, and may move you into conventional territory (avoiding mortgage insurance). Temporary residents and foreign nationals typically face higher minimums than permanent residents — the exact threshold varies by lender and status, so confirm current figures directly.

Will my foreign income be considered by Canadian lenders?

It depends on the lender — there is no universal rule. Some Big Six banks and monoline lenders will consider foreign employment income verifiable through official payslips or tax documents; foreign self-employment income is harder to verify and often discounted. Working with a broker experienced in cross-border income is advisable.

How does becoming a tax resident affect my mortgage application?

Establishing residential ties in Canada generally makes you a CRA tax resident from that date. Lenders may eventually request a Notice of Assessment as income verification — filing accurately and on time builds the documented trail that supports future renewals.

Can a co-signer improve my chances of mortgage approval?

Yes, in many cases. A creditworthy Canadian co-signer can strengthen an application with an established credit profile and additional income — but shares full legal liability for the debt. Both parties should review this with independent legal advice before proceeding.

What happens to my mortgage if my immigration status changes?

Your mortgage contract remains in force regardless; lenders do not typically monitor immigration status after funding. If your status affects your right to work, your income could be disrupted. If you transition to permanent residency, notify your lender, as improved status can open access to better rates.

Conclusion

Securing a mortgage as a newcomer to Canada is achievable in 2026 for many applicants, provided you understand how lenders assess non-traditional files and which programs fit your situation. Your immigration status, employment stability, and down payment size collectively determine which lending tier you can access — permanent residents generally face fewer barriers, while temporary workers and international students benefit most from CMHC-insured newcomer programs.

Building your financial foundation early matters: a no-cost bank account, a secured credit card, and early CRA registration compound over time. Our newcomer bank account guide and newcomer credit card guide cover these first steps. Work with a licensed mortgage broker who has documented newcomer-file experience, avoid the common mistakes outlined above, and treat your first Canadian mortgage as a long-term commitment rather than a rushed purchase.

Disclaimer

For Informational Purposes Only

The content published on MoneyAbroadGuide.com, including this guide, is intended solely for general informational and educational purposes. It does not constitute financial, legal, tax, or mortgage advice, and should not be relied upon as a substitute for consultation with a licensed mortgage professional, regulated financial advisor, or qualified legal counsel in your province or territory.

Mortgage products, interest rates, lender eligibility criteria, and regulatory requirements — including those governed by OSFI, CMHC, FCAC, and the CRA — change frequently. We do not guarantee the accuracy, completeness, or timeliness of any information presented. Always verify details directly with your lender, a licensed mortgage broker, or official sources such as Canada.ca, CMHC, or OSFI before making financial decisions.

Affiliate Disclosure: MoneyAbroadGuide.com may receive compensation from financial institutions or mortgage providers featured or linked within this article. This may influence which products are highlighted, but does not influence our editorial assessments. Our editorial team operates independently of commercial relationships.

Immigration and tax residency circumstances vary by individual. Newcomers are encouraged to review their specific obligations with a CRA-registered tax professional and a licensed immigration consultant registered with the CICC.

About the Author

Talal Eddaouahiri is the founder of MoneyAbroadGuide.com, an independent financial information platform for immigrants and newcomers in the United States and Canada. Originally from Morocco, he settled in the U.S. in 2015 and built his own credit history and banking relationships from scratch in both countries. His background is in retail banking and customer relations, and he draws on that firsthand experience to write independent, source-based guides — citing regulators including the FCAC, FINTRAC, OSFI, CRA, IRS, and CDIC — to help newcomers navigate financial systems with confidence.

Last Updated: July 2026

About Talal Eddaouahiri

Founder & Editor of MoneyAbroadGuide.com. A Moroccan immigrant who settled in the United States in 2015, Talal opened bank accounts and built credit from zero in both the US and Canada. His background is in retail banking and customer relations, and he writes independent, source-based guides (FCAC, FINTRAC, OSFI, CRA, IRS, CDIC) to help newcomers navigate their first financial steps. Read his full profile →