Best Newcomer Bank Accounts In Canada: Complete Guide for Canada Immigrants (2026)

Quick Answer: The best newcomer bank accounts in Canada include offerings from RBC, TD, Scotiabank, CIBC, and BMO — most waive monthly fees for your first year. You have the legal right to open an account regardless of employment status, and many accounts require only your passport and immigration documents.

Opening a bank account is one of the first and most critical financial steps after arriving in Canada. Without one, you cannot receive a salary, pay rent, build a credit history, or access government benefits — all essential to settling successfully.

The good news: the Financial Consumer Agency of Canada (FCAC) mandates that banks offer accessible banking to all residents. Under FCAC’s no-cost account framework, newcomers in their first year in Canada are typically eligible for $0/month bank accounts — a meaningful saving as you establish your finances.

Critically, you have the legal right to open a personal bank account even without a job, without an initial deposit, or if you are unemployed. Banks cannot refuse you solely on those grounds — a protection many newcomers are unaware of.

What about identification? Most banks accept a valid foreign passport combined with your immigration documents (such as a Confirmation of Permanent Residence or study/work permit issued by Immigration, Refugees and Citizenship Canada). A Social Insurance Number (SIN) is required to work and access government services, but for non-interest-bearing accounts, you may decline to provide your SIN as identification.

Once your account is active, your banking relationship also has tax implications: newcomers generally become Canadian tax residents on their arrival date and may be required to file a return with the Canada Revenue Agency.

This guide breaks down the top newcomer bank accounts available in 2026 — comparing fees, welcome offers, multi-currency features, and ease of opening — so you can choose the right account from day one. If you are also settling in the United States, see our companion guide: Best ITIN-Friendly Bank Accounts for New Immigrants in the USA (2026).

1. Best Newcomer Bank Accounts In Canada for Canada Immigrants in 2026: Quick Overview

Arriving in Canada without an established credit history, a provincial ID, or a local address creates immediate financial friction — and the wrong bank account compounds that friction with monthly fees that erode settlement funds from day one. The accounts below were selected by analyzing publicly available fee schedules, newcomer package terms, digital access quality, and FCAC-published eligibility standards.

What Qualifies as a “Best” Newcomer Account

Three criteria distinguish genuinely useful newcomer accounts from standard chequing products rebranded with welcome language:

- Fee waiver duration —ideally minimum, structured around IRCC-defined newcomer status

- Minimal documentation requirements — acceptance of a passport, immigration documents (PR card, study/work permit), or IRCC confirmation letter in lieu of Canadian ID

- Credit-building pathways — access to secured credit cards or credit-builder products during or immediately after the waiver period

According to the Financial Consumer Agency of Canada (FCAC), newcomers in their first year are eligible for no-cost bank accounts under a formal commitment between FCAC and Canada’s major banks — meaning fee waivers are a regulatory baseline, not a marketing favour.

2026 Top Picks at a Glance

| Bank | Account | Fee Waiver Period | Key Newcomer Benefit |

|---|---|---|---|

| RBC | RBC Newcomer Advantage | varies by provider — confirm directly | Bundled credit card offer |

| CIBC | CIBC Smart™ for Newcomers | varies by provider — confirm directly | No minimum balance |

| BMO | BMO NewStart® Program | varies by provider — confirm directly | U.S. dollar sub-account option |

| Scotiabank | StartRight® Program | varies by provider — confirm directly | Scene+ rewards from month one |

| TD | TD New to Canada | varies by provider — confirm directly | Cross-border USD account access |

| Tangerine | New to Canada | varies by provider — confirm directly | No branch required; fully digital |

For example: a newcomer landing in September 2025 who opens a CIBC Smart™ for Newcomers account avoids in standard monthly fees over the waiver window —funds that remain available for rent deposits and settlement costs instead.

What This Guide Covers Next

Sections that follow examine each account in detail — fee structures post-waiver, transaction limits, international transfer compatibility, and how each bank’s newcomer package interacts with CRA obligations newcomers face upon establishing Canadian tax residency. According to the Canada Revenue Agency, tax residency begins on the date of arrival, making a properly structured account with clear transaction records relevant from day one — not just for spending, but for future tax filing.

Note also that for non-interest-bearing accounts, FCAC confirms you may decline to provide your SIN as identification — a practical detail that removes a common barrier for newcomers who have not yet received their SIN from Service Canada.

2. What Is a Newcomer Bank Account in Canada and Why Do Immigrants Need One?

A newcomer bank account is a specialized chequing or savings product that Canadian banks structure specifically for people arriving in Canada — permanent residents, temporary foreign workers, international students, and those on work or study permits. Unlike standard accounts, these products remove the typical barriers: no Canadian credit history required, no proof of employment, and no minimum opening deposit.

The Structural Problem Newcomers Face

Mainstream Canadian banking is built around credit history, domestic income verification, and established identity documentation. Immigrants arrive with none of these, yet they need banking immediately — to receive a first paycheque, pay rent, remit money abroad, and register for CRA and Service Canada benefits. Without a bank account, even basic financial participation stalls.

According to the Financial Consumer Agency of Canada (FCAC), newcomers have the right to open a personal account regardless of employment status or whether they deposit money immediately — though this eligibility point was covered earlier. What matters here is why banks created dedicated products rather than simply applying standard eligibility waivers: newcomer accounts bundle several concessions into one structured offer.

What These Accounts Actually Bundle

Beyond waived monthly fees (covered under products like StartRight and NewStart earlier), newcomer accounts typically include:

- Credit history bypass — approval based on immigration status documents (permanent resident card, study or work permit) rather than a Canadian credit bureau file

- Foreign currency utilities — multi-currency transfers, preferential USD exchange rates on chequing, or linked USD accounts

- Credit-building on-ramp — access to a secured credit card or credit card with low threshold, enabling newcomers to begin the credit file that the FCAC notes is essential for renting, financing, and future borrowing

- CRA-direct-deposit readiness — accounts are immediately eligible to receive CRA benefit payments (GST/HST credits, Canada Child Benefit) once filed, which requires a domestic account

A Concrete Illustration

For example, a newcomer arriving in Ontario with a PR card but no SIN yet can still open a non-interest-bearing account — according to FCAC banking rules, providing a SIN as identification for such accounts is optional. That account becomes the deposit vehicle for their first employer payroll, CRA benefit deposits, and FINTRAC-compliant international transfers — all within the first week of arrival.

Why Account Choice at Arrival Has Compounding Effects

The bank an immigrant chooses in month one often determines their credit card eligibility in month six, their mortgage pre-qualification in year three, and their registered account access (TFSA, RRSP, FHSA) throughout their financial life in Canada. Switching later is possible but involves re-establishing direct-deposit relationships, rebuilding credit product history, and potentially losing introductory fee-waiver windows. According to FCAC data, no-cost accounts are available to qualifying newcomers in their first year — making the initial decision both low-cost and high-stakes simultaneously.

3. Eligibility Requirements for Immigrants

Qualifying for a newcomer bank account is less restrictive than most immigrants expect — but specific documentation requirements and program boundaries vary by bank and immigration status.

Who Qualifies by Immigration Category

Canadian banks generally extend newcomer pricing to:

- Permanent residents – eligible from the date PR status is granted

- International students – eligible with a valid study permit; most banks accept students through programs like StartRight

- Temporary foreign workers – eligible with a valid work permit; some banks impose shorter fee-waiver windows than the standard period

- Convention refugees and protected persons – eligible under IRCC-recognized status; documentation requirements may differ from standard PR applicants

Notably, citizenship is not required. According to the Financial Consumer Agency of Canada, you have the right to open a personal account even without employment or an immediate deposit — and banks cannot refuse solely because you lack a Canadian credit history.

Accepted Identification Documents

Banks must comply with FINTRAC’s customer due diligence rules under the Proceeds of Crime (Money Laundering) and Terrorist Financing Act. In practice, one or two of the following typically suffice:

- Passport (most universally accepted)

- IRCC-issued PR card or Confirmation of Permanent Residence (COPR)

- Study or work permit

- Canadian driver’s licence (if obtained post-arrival)

- Foreign driver’s licence (accepted by select banks during early settlement)

For example, a newcomer who arrived with only a passport and a COPR document — before receiving a PR card — can open an account at most Big Six banks using those two documents alone.

SIN: Required or Optional?

According to the FCAC’s guidance on opening a bank account, a SIN is not mandatory to open a non-interest-bearing account; you may decline to provide it as identification. However, banks will request your SIN for interest-bearing accounts to fulfill CRA reporting obligations — this connects directly to your tax residency status, since the CRA treats newcomers as Canadian residents for tax purposes from their arrival date, affecting interest income reporting and benefit eligibility.

Applying for a SIN through Service Canada as early as possible removes this friction entirely and unlocks TFSA contribution room.

Program Eligibility Windows

Most newcomer programs —including NewStart and StartRight —impose an enrollment deadline, typically within 3 to of first arriving in Canada, after which standard account pricing applies. Immigrants who delay banking setup risk losing access to structured newcomer benefits, even if they arrived recently.

According to FCAC, no-cost bank accounts for newcomers are available during the first year under the FCAC commitment — a protection enforced at the regulatory level, not solely at each bank’s discretion.

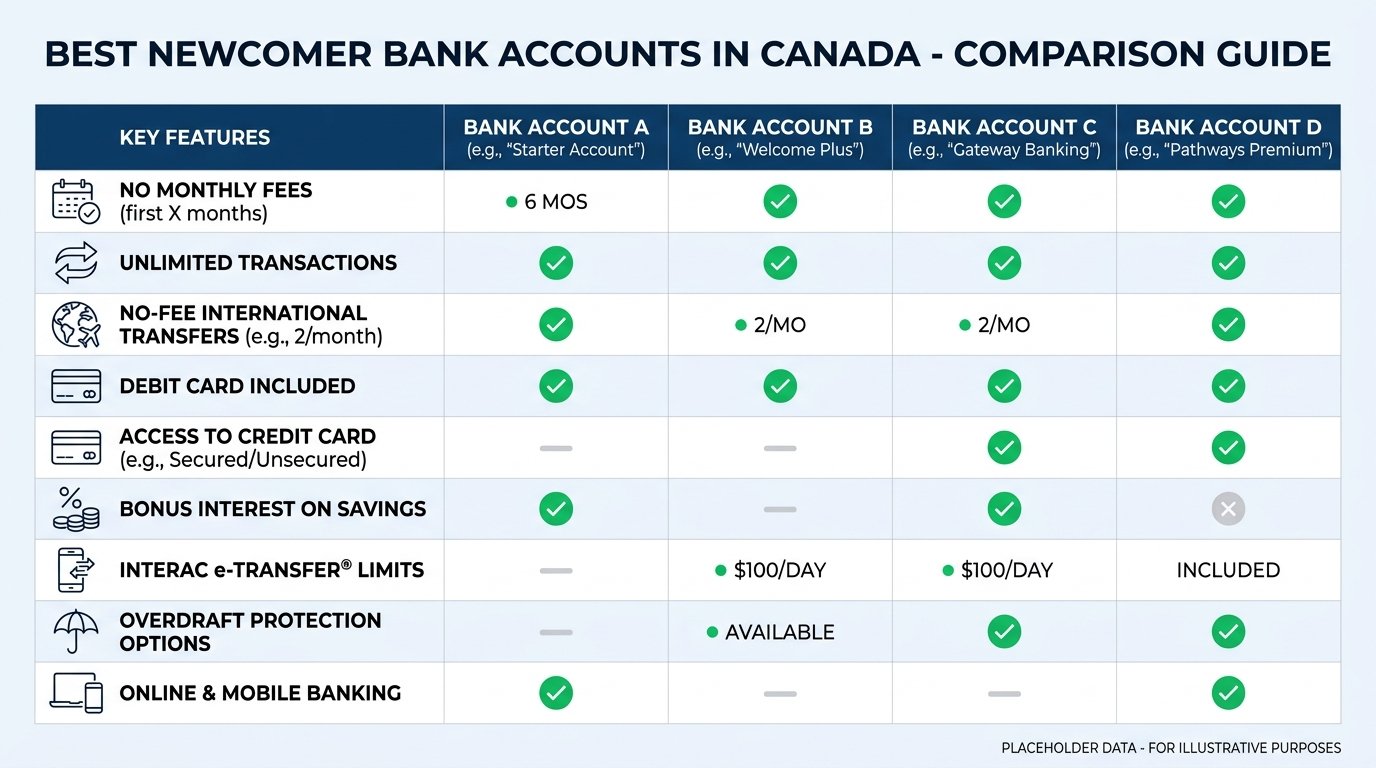

4. Comparing the Best Newcomer Bank Accounts in Canada: Side-by-Side Breakdown

Choosing the right account at arrival shapes your credit history, fee exposure, and access to banking tools for years ahead. The table below cuts through promotional language to compare the leading newcomer-specific accounts on the dimensions that matter most to immigrants: fee waivers, bundled services, international transfer capabilities, and credit-building pathways. All six institutions are federally regulated under OSFI oversight, and each participates in the FCAC’s no-cost/low-cost account framework, meaning eligible newcomers can access fee-free accounts during their qualifying period.

| Feature | RBC Newcomer Advantage | CIBC Smart for Newcomers | BMO NewStart Program | TD New to Canada | Scotiabank StartRight | National Bank |

|---|---|---|---|---|---|---|

| Monthly Fee Waiver Period | varies by provider — confirm directly | varies by provider — confirm directly | varies by provider — confirm directly | varies by provider — confirm directly | varies by provider — confirm directly | Varies by product |

| Eligible Immigration Categories | PR, Student, Worker permit | PR, Student, Worker permit | PR, Student, Refugee | PR, Student, Worker permit | PR, Student, Worker permit | PR, Newcomer residents |

| Free Transactions Included | Unlimited (during waiver) | Unlimited (during waiver) | Unlimited (during waiver) | Unlimited (during waiver) | Unlimited (during waiver) | Limited; varies |

| Bundled Credit Card | Yes, secured or unsecured option | Yes, with reduced requirements | Yes, with NewStart | Yes, with reduced credit history bar | Yes, with StartRight | Yes, varies |

| International Wire Transfers | Yes, preferential rates | Yes, via CIBC Global Money Transfer | Yes, via BMO Global Transfer | Yes, via TD Global Transfer | Yes, with Scotiabank network | Yes, standard rates |

| Dedicated Newcomer Support | In-branch multilingual advisors | Multilingual phone and digital | In-branch newcomer specialists | In-branch and digital | In-branch and StartRight hub | Digital-first support |

| Credit-Building Pathway | Secured card + credit builder | Secured card option | Secured card + RRSP access | Secured card + TFSA | Secured card + Scene+ rewards | Secured card available |

| SIN Requirement at Opening | Optional for non-interest accounts | Optional for non-interest accounts | Optional for non-interest accounts | Optional for non-interest accounts | Optional for non-interest accounts | Optional for non-interest accounts |

Key takeaway: Fee waiver length and credit-building tools vary meaningfully across providers. Scotiabank’s StartRight program typically offers the longest published waiver window, while RBC and TD carry the broadest branch networks for in-person newcomer support. Newcomers who anticipate frequent international remittances should weight wire transfer costs and partnerships above branch count when making their selection.

Illustrative Scenarios

The following are illustrative scenarios, not real testimonials or case studies of specific individuals.

Illustrative Scenario: Skilled Worker Visa Holder, Relocating for Employment

A skilled worker arrives before their first paycheque clears. Using only their passport and immigration documents, they open a no-fee account — as permitted under FCAC guidelines — to receive their initial direct deposit and begin building a Canadian credit footprint from day one.

Expert Recommendation: Best Newcomer Bank Accounts in Canada

Top Pick: RBC Newcomer Advantage

RBC earns the top position for most arriving immigrants because it combines breadth of service with practical arrival-day utility. The bank’s newcomer program pairs fee-free chequing with immediate access to credit-building tools — a combination that addresses the two most pressing financial gaps newcomers typically face in their first months.

The fee waiver structure aligns with the broader FCAC commitment that makes no-cost monthly accounts available to eligible newcomers during their first year (FCAC low-cost/no-cost accounts), and RBC’s program extends competitive features well beyond that baseline window. For newcomers who arrive with employment already arranged, the account integrates smoothly with CRA tax obligations that begin from your first day of Canadian residency (CRA newcomers page) — making early account setup genuinely consequential, not just convenient.

Best suited for: Permanent residents, skilled workers, and international graduates settling in major urban centres who want a single institution to handle chequing, savings, credit, and cross-border transfers.

Runner-Up: CIBC Smart Account for Newcomers

CIBC earns the runner-up position for newcomers who prioritise flexibility over full-service bundling. Its Smart Account scales transaction limits as your Canadian financial footprint grows, which suits newcomers whose banking volume is initially modest but rises quickly once employment and regular transfers are established.

CIBC’s digital infrastructure is particularly strong — important context for newcomers managing finances across two countries simultaneously. If you are also evaluating U.S. banking options during a cross-border move or extended travel, our guide to opening a bank account as a newcomer in the USA walks through the parallel process in detail.

Best suited for: Newcomers on open work permits, those in temporary-to-permanent transitions, or anyone expecting to manage moderate monthly transaction volumes while building Canadian credit history.

Bottom Line

Both institutions are federally regulated under OSFI oversight and participate in the CDIC deposit protection framework. For most newcomers, the account-opening decision matters more than most initially assume — your first Canadian account shapes your credit file, tax residency documentation trail, and access to government benefit deposits from day one. Choose the institution whose branch network, language support, and product roadmap match where your settlement is actually headed.

Frequently Asked Questions: Newcomer Bank Accounts in Canada

Can I open a Canadian bank account before I arrive in Canada?

Several major banks — including RBC and CIBC — offer pre-arrival banking programs that let you initiate an account application from your home country before landing. Typically, you complete identity verification remotely and activate the account once you arrive with supporting documents. This means you can have account details ready for wire transfers, rent deposits, and payroll setup from day one. Check each bank’s international services page for country-specific availability, as supported regions vary.

Which documents do I actually need to open a newcomer bank account?

Most federally regulated banks accept two pieces of government-issued ID; common combinations include a passport plus your Confirmation of Permanent Residence (COPR), PR card, or study/work permit. Under FCAC rules, you have the right to open a personal account even without current employment, and without making an initial deposit — so lack of a Canadian credit history or income is not a valid reason for denial.

Do I need a Social Insurance Number to open a bank account?

Not necessarily upfront. For a non-interest-bearing chequing account, you may decline to provide a SIN, since banks collect it primarily for tax-reporting purposes on interest income, as clarified by FCAC. However, once your account starts earning interest — through a savings component or TFSA — the bank will typically request your SIN for CRA reporting. Apply for your SIN at Service Canada promptly after arrival regardless.

How long does the fee-waiver period on newcomer accounts last?

The free-banking window varies by institution, but most programs run for a defined introductory period — often structured around your first year or two in Canada. During that window, monthly fees are waived. After it expires, your account typically converts to a standard plan, which can carry meaningful monthly costs. Review the post-promotional pricing before you open, and set a calendar reminder to reassess or renegotiate your plan before the waiver lapses.

Are free newcomer bank accounts guaranteed by law, or are they optional bank offers?

They are a regulatory commitment, not purely voluntary marketing. Under the FCAC’s low-cost and no-cost account framework, banks that have signed onto the commitment must offer eligible newcomers access to no-monthly-fee accounts during their qualifying first year. FCAC — the Financial Consumer Agency of Canada — monitors compliance, so this is an enforceable commitment rather than a discretionary promotion.

Will opening a newcomer bank account help me build a Canadian credit history?

A deposit account alone does not build credit, since it doesn’t involve borrowing. However, it is the foundation: you need an active Canadian bank account to qualify for a secured credit card, which is typically the first step toward a credit file with Equifax or TransUnion Canada. Many newcomer banking bundles include a referral or direct application pathway to a secured card — making account selection consequential for your longer-term credit-building timeline.

How do my Canadian bank account and taxes connect?

Once you land, you generally become a Canadian tax resident and may be required to file an annual return with the CRA — details for newcomers are outlined on the CRA’s newcomers page. Your bank account is directly relevant: interest income is taxable, government benefits like GST/HST credits are deposited there, and the CRA uses your SIN to link your account activity to your tax record. Getting your banking and SIN sorted early simplifies your first tax filing.

Can international students and temporary workers use newcomer bank accounts?

Yes — eligibility typically extends beyond permanent residents. Most major banks include international students, temporary foreign workers, and holders of valid study or work permits within their newcomer banking programs. Required documentation varies slightly by status, so confirm with the specific institution. Temporary residents should also note that their fee-waiver eligibility and product access may differ from those on a permanent residence pathway.

Is my money protected if a Canadian bank fails?

Deposits at federally regulated banks are protected by the Canada Deposit Insurance Corporation (CDIC), a federal Crown corporation. Coverage applies per depositor, per insured category, up to defined limits — meaning your chequing and savings balances qualify, subject to those thresholds. All the major banks featured in this guide are CDIC members. Credit unions are provincially regulated and covered by provincial deposit insurance schemes, which vary by province.

Should I keep my home-country bank account after opening a Canadian one?

For most newcomers, maintaining both — at least initially — is practical. International transfers for family support, residual income, or asset liquidation are easier with an active account in your origin country. Some banks charge foreign transaction fees on overseas withdrawals, so a parallel account reduces those costs during transition. Over time, as your financial life consolidates in Canada, you can evaluate whether maintaining the overseas account remains cost-effective relative to annual fees or minimum balance requirements abroad.

Conclusion

Choosing the right bank account in your first weeks in Canada shapes your financial trajectory far more than most newcomers anticipate. As this guide has shown, the major chartered banks — RBC, CIBC, BMO, TD, and others — each bundle specific newcomer benefits into their StartRight, NewStart, and equivalent programs, but those bundles differ meaningfully in fee-waiver duration, included services, cross-border transfer access, and the speed at which you can establish credit history.

A few principles should anchor your final decision:

Match the account to your actual transaction pattern. If you send money internationally every month, prioritize institutions with lower wire fees or preferred exchange rates for newcomers. If you expect to stay in Canada long-term and build toward homeownership, the TFSA and credit-building features matter more than short-term fee waivers.

Know your rights before you walk in. Canadian law guarantees your right to open a personal account even without employment or an immediate deposit, per FCAC guidance — no bank can turn you away solely because you just arrived. Separately, qualified newcomers are eligible for no-monthly-fee accounts during their first year under the FCAC’s low-cost and no-cost account framework.

Start your tax record early. The CRA’s newcomer tax page confirms that Canadian tax residency typically begins on arrival — your bank account is the foundation for filing correctly.

The best account is the one you open immediately, use actively, and upgrade deliberately as your Canadian financial life matures.

Disclaimer

For informational purposes only. MoneyAbroadGuide.com is an independent financial information platform. Nothing published on this site constitutes personalized financial, legal, immigration, or tax advice. Readers should consult a licensed financial advisor, regulated immigration consultant, or qualified tax professional before making decisions based on information presented here.

Affiliate and commercial relationships. This article may contain affiliate links to financial products and institutions. MoneyAbroadGuide.com may receive compensation when readers apply for or open accounts through links on this page. This compensation may influence which products are featured or their placement; it does not influence our editorial assessments. We do not review every available product in the Canadian market.

Accuracy and currency. Bank account terms, fee structures, promotional offers, and eligibility criteria change frequently. All product details — including fee-waiver periods, bundled features, and newcomer program availability — should be verified directly with the institution before applying. Regulatory information is drawn from official sources including FCAC, IRCC, and CRA; readers should consult those sources for the most current guidance.

Last reviewed: January 2026.

About the Author

Talal Eddaouahiri is the founder of MoneyAbroadGuide.com, an independent financial information platform for immigrants and newcomers in the United States and Canada. Originally from Morocco, he settled in the U.S. in 2015 and built his own credit history and banking relationships from scratch in both countries. His background is in retail banking and customer relations, and he draws on that firsthand experience to write independent, source-based guides — citing regulators including the FCAC, FINTRAC, OSFI, CRA, IRS, and CDIC — to help newcomers navigate financial systems with confidence.

Learn more about our Fact-Checking Process and our How We Test when researching this guide.

Last Updated: July 2026

About Talal Eddaouahiri

Founder & Editor of MoneyAbroadGuide.com. A Moroccan immigrant who settled in the United States in 2015, Talal opened bank accounts and built credit from zero in both the US and Canada. His background is in retail banking and customer relations, and he writes independent, source-based guides (FCAC, FINTRAC, OSFI, CRA, IRS, CDIC) to help newcomers navigate their first financial steps. Read his full profile →