Best First-Time Home Buyer Mortgage For Newcomers: Complete Guide for USA Immigrants (2026)

Quick Answer: Immigrants and newcomers can qualify for U.S. mortgages — including FHA loans — using a valid visa, Individual Taxpayer Identification Number (ITIN), or green card. Minimum down payments, credit requirements, and eligible loan types vary by immigration status and lender. Start at HUD.gov for official guidance.

Buying your first home in the United States as a newcomer or immigrant is achievable — but the path looks different from what a U.S.-born citizen typically experiences. Whether you hold a work visa, permanent resident status, or are building credit from scratch, understanding which mortgage programs are available to you, and what regulators require, is the essential first step.

The U.S. mortgage market is overseen by multiple federal agencies. The Consumer Financial Protection Bureau (CFPB) regulates mortgage lenders and provides consumer protections under the Truth in Lending Act (TILA) and the Real Estate Settlement Procedures Act (RESPA). The Department of Housing and Urban Development (HUD) administers FHA loan programs specifically designed to help buyers who may not qualify for conventional financing — a category that frequently includes immigrants with limited U.S. credit history.

For many newcomers, the FHA loan is the most accessible entry point. It accepts lower credit scores and smaller down payments compared to conventional loans. Borrowers with a credit score of 580 or above may qualify for a down payment as low as 3.5% of the purchase price. Importantly, FHA eligibility is not restricted to U.S. citizens — lawful permanent residents and certain non-permanent resident visa holders may also qualify, provided they meet income, credit, and occupancy requirements.

Beyond FHA, conventional loans backed by Fannie Mae and Freddie Mac, ITIN loans from community lenders, and state-level first-time buyer assistance programs each serve different segments of the newcomer population. Navigating these options requires clarity on your immigration status, tax filing history, and credit profile.

The CFPB’s mortgage tools and USA.gov’s home-buying guide provide authoritative, free resources to help you compare loan types and understand your rights before speaking with any lender.

This guide covers every stage — from eligibility and documentation to loan comparison and closing — so you can make a fully informed decision in 2026.

1. Best First-Time Home Buyer Mortgage For Newcomers: Quick Overview

Navigating U.S. mortgage markets as a newcomer involves overlapping eligibility rules, immigration status considerations, and loan program nuances that standard homebuyer guides rarely address. This section maps the core landscape so you can evaluate each program with full context.

Who Qualifies as a “Newcomer Borrower”

Lenders and federal agencies recognize several newcomer profiles:

- Permanent residents (green card holders): Treated nearly identically to U.S. citizens across FHA, Fannie Mae, and Freddie Mac programs.

- Non-permanent residents with work authorization (H-1B, L-1, TN, O-1): Eligible for FHA-backed loans; Fannie Mae and Freddie Mac also allow non-permanent resident borrowers with valid work authorization.

- ITIN borrowers without Social Security numbers: A narrower but growing pool of lenders—primarily community development financial institutions (CDFIs) and credit unions—offer ITIN-based mortgage products, as noted above.

- Recent arrivals with thin credit files: Borrowers who have not yet established U.S. credit history face stricter underwriting; according to HUD, borrowers with non-traditional or insufficient credit history under FHA manual underwriting may not exceed 31/43 qualifying ratios (front-end/back-end debt-to-income).

Credit Score Thresholds That Matter Most

According to HUD, the minimum credit score for FHA’s standard down payment option is 580. Newcomers whose U.S. credit history is under two years often score below this threshold despite having strong financial histories abroad—a gap lenders can sometimes bridge with alternative credit documentation (rental payment records, foreign bank statements, international credit reports through services such as NOVA Credit).

For example, a newcomer on an H-1B visa who has been in the U.S. for may have a thin-file score below 580. Under FHA manual underwriting, that borrower must keep housing costs within the front-end ratio and total debt within —stricter than automated underwriting approvals.

Key Program Comparison at a Glance

| Factor | FHA | Fannie Mae HomeReady | Freddie Mac Home Possible |

|---|---|---|---|

| Min. credit score | 580 (standard) | 620 | 660 |

| Non-permanent residents | Eligible | Eligible | Eligible |

| ITIN borrowers | Case-by-case | Generally no | Generally no |

| Mortgage insurance | Lifetime (low down) | Cancellable PMI | Cancellable PMI |

| Income limits | None | Area median income limits apply | Area median income limits apply |

Independent Guidance Reduces Costly Mistakes

HUD-approved housing counselors provide independent advice on loan program suitability, often at little or no cost—a resource particularly valuable for newcomers unfamiliar with U.S. mortgage disclosure documents, including the Loan Estimate and Closing Disclosure governed by the regulations noted above. The CFPB’s loan options tool also lets borrowers compare program structures before approaching lenders.

Identifying your immigration status category, current credit profile, and income documentation type is the essential first step—each combination narrows the field of viable loan programs before a single lender application is submitted.

2. What Is a First-Time Home Buyer Mortgage for Newcomers and Why Do Immigrants Need It?

A first-time home buyer mortgage for newcomers is a home loan product — or a set of underwriting guidelines — specifically designed to accommodate borrowers who lack a U.S. credit history, hold non-permanent immigration status, or earn income in ways that standard loan models struggle to verify. Standard conventional underwriting assumes years of U.S.-filed tax returns, a Social Security Number-linked credit file, and employer W-2s. Most recent immigrants have none of these, which is why purpose-built programs exist.

The Structural Gap Immigrants Face

The U.S. mortgage market defaults to Fannie Mae and Freddie Mac underwriting guidelines, which were built around the financial profile of a long-term U.S. resident. A newcomer arriving with strong foreign income, substantial savings, and a spotless repayment history in their home country is nonetheless treated as “credit invisible” under that framework.

According to the CFPB’s mortgage tools, lenders must evaluate a borrower’s ability to repay based on verified income, assets, and credit history — but the regulation does not specify where that history must originate, leaving room for lenders willing to accept foreign credit reports or ITIN-based files. The programs noted in Section 1 (FHA, HomeReady, Home Possible) exploit exactly that regulatory flexibility.

Why “First-Time” Status Opens Extra Doors

Under federal housing policy, a “first-time buyer” is defined broadly: anyone who has not owned a primary residence in the past three years qualifies — meaning a newcomer who owned property abroad can still access first-time buyer benefits upon arrival. According to HUD’s home-buying resources, these benefits typically include access to down payment assistance programs, reduced mortgage insurance structures, and mandatory housing counseling that helps borrowers understand loan terms.

That counseling matters. HUD-approved housing counselors provide independent guidance — often at little or no cost — on loan comparison, predatory lending risks, and affordability budgeting, which is particularly valuable when a newcomer is navigating an unfamiliar regulatory environment.

A Concrete Example

Consider a newcomer who has been in the U.S. for, holds a valid Employment Authorization Document, earns a documented salary, but has no U.S. credit score yet. A standard conventional lender declines the application. Under FHA guidelines, that same borrower may qualify through manual underwriting — provided their debt ratios do not exceed the 31/43 thresholds referenced in Section 1. The FHA path remains open; the standard path does not.

The Regulatory Reason This Matters

The Equal Credit Opportunity Act (ECOA), enforced by the CFPB, prohibits lenders from discriminating based on national origin. However, immigration status is not a protected class under ECOA, which is why lender policies on visa types vary significantly. Understanding which program accepts which status — rather than assuming any lender will accommodate — is the practical skill this guide builds across subsequent sections.

3. Eligibility Requirements for Immigrants

Eligibility for newcomer mortgage programs operates across three distinct layers: immigration status, credit profile, and property rules. Understanding each layer prevents wasted applications and lender rejections.

Immigration Status: Who Qualifies

FHA — the program most relevant to immigrants, as introduced earlier — accepts lawful permanent residents (green card holders) on equal terms with U.S. citizens. Beyond that, non-permanent residents with valid work authorization (EAD card, H-1B, L-1, O-1, TN, or E-2 visas) also qualify, provided their stay is likely to continue. Dreamers (DACA recipients) remain a contested category: FHA formally reinstated DACA eligibility in 2021, though individual lender overlays vary. ITIN-only borrowers have fewer FHA options but can access portfolio lenders and some state housing finance agency programs, as noted in the program overview above.

According to USA.gov’s home-buying guidance, immigration status documentation is a standard lender requirement — borrowers should expect to produce visa paperwork or EAD cards alongside income verification.

Credit Requirements by Program

Credit thresholds differ meaningfully across programs:

- FHA: According to HUD, a minimum decision credit score of 580 qualifies borrowers for the 3.5% down payment option.

- FHA: Eligible with down under manual underwriting. According to HUD, manually underwritten loans below 580 may not exceed 31/43 qualifying ratios.

- Fannie Mae HomeReady / Freddie Mac Home Possible: Both programs require a minimum 620 score — stricter than FHA, but PMI is cancellable once equity thresholds are met.

- ITIN borrowers: Lenders using NOVA Credit or accepting foreign credit histories set their own thresholds; expect for competitive pricing.

For newcomers with no U.S. credit history, NOVA Credit’s international report conversion (mentioned earlier) is often the most efficient path to meeting these thresholds without a multi-year seasoning period.

Property and Occupancy Rules

Eligible properties must serve as the borrower’s primary residence — FHA and the GSE programs cited above do not finance investment purchases or vacation homes for first-time buyer program benefits. FHA also limits eligible property types: single-family homes, FHA-approved condominiums, 2–4 unit properties (where the borrower occupies one unit), and manufactured homes meeting HUD standards.

For example, a newcomer purchasing a two-unit property can use FHA financing and offset mortgage costs with rental income from the second unit — a structure HUD’s guidelines explicitly permit.

Income and Employment Documentation

Lenders require a two-year employment history, but FHA allows exceptions when a borrower moved to the U.S. for employment. A recent job offer letter with a documented start date can substitute for domestic employment history under FHA’s guidelines. Self-employed newcomers must show two years of U.S. tax returns, or alternatively, lenders may accept foreign tax records where the borrower operated a business abroad.

HUD-approved housing counselors can review a borrower’s specific documentation gaps and recommend the correct program path — often at no cost, according to HUD.

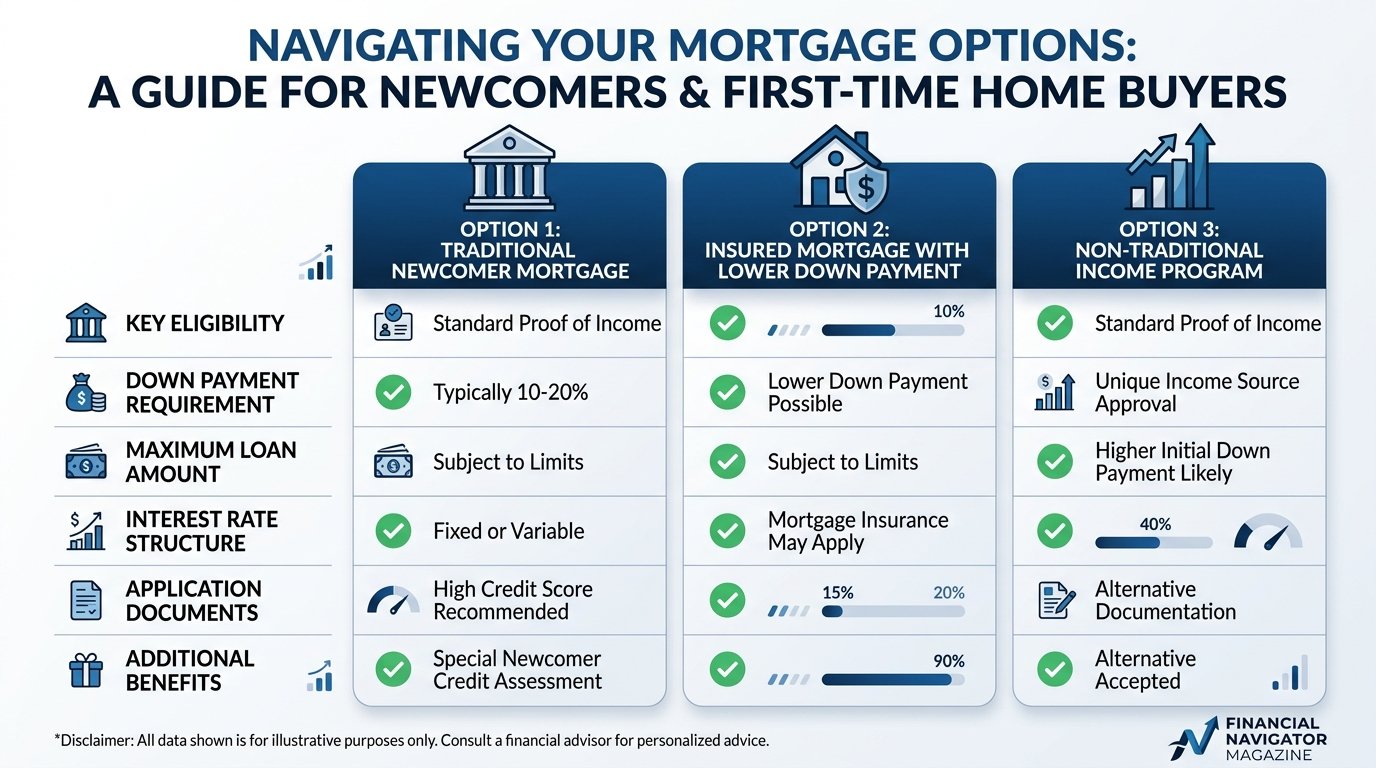

4. Program Comparison: First-Time Home Buyer Mortgages for Newcomers (USA)

Choosing the right mortgage program hinges on your immigration status, credit profile, and available down payment. The table below distills the key variables across the four programs most relevant to newcomer borrowers. Down payment figures reference HUD’s published minimums; all other figures are qualitative or sourced inline.

| Feature | FHA Loan | Fannie Mae HomeReady | Freddie Mac Home Possible | ITIN Loan (Portfolio Lenders) |

|---|---|---|---|---|

| Minimum Down Payment | As low as 3.5% for qualifying borrowers (HUD) | Typically low (varies by lender) | Typically low (varies by lender) | Often higher; varies by lender |

| Minimum Credit Score | varies by provider — confirm directly | Varies by lender; generally moderate | Varies by lender; generally moderate | Often flexible; non-traditional credit accepted |

| ITIN Accepted (No SSN) | Yes, with eligible status | Select lenders only | Select lenders only | Yes — primary design use case |

| Non-Traditional Credit | Accepted under manual underwriting (HUD) | Lender-dependent | Lender-dependent | Commonly accepted |

| Mortgage Insurance | Required; duration depends on loan terms | PMI cancellable once sufficient equity reached | PMI cancellable once sufficient equity reached | Varies significantly by lender |

| Income Limit | None | Area median income limits apply | Area median income limits apply | None typically |

| HUD Counseling Access | Strongly recommended; independent advisors often available at little or no cost (HUD Locator) | Recommended | Recommended | Advisable given limited consumer protections |

| Best For | Newcomers with limited credit history and lawful status | Income-qualified borrowers with SSN | Income-qualified borrowers with SSN | Undocumented or ITIN-only borrowers |

How to read this table: No single program dominates. FHA’s federally backed structure offers the most transparent floor — a published minimum credit score and a published minimum down payment — making it the most predictable option for newcomers navigating an unfamiliar system. HomeReady and Home Possible may deliver lower long-term costs once PMI cancels, but income caps and SSN requirements limit access. Portfolio ITIN loans fill a genuine gap but carry terms that vary widely and warrant independent review; a HUD-approved housing counselor (find one here) can help you compare Loan Estimates across these program types before you commit.

Illustrative Scenarios

The following are illustrative scenarios, not real testimonials or case studies of specific individuals.

Illustrative Scenario: Temporary Work Visa Holder, Tech Sector Relocation

A visa holder with an established foreign credit history and ITIN uses an FHA-backed loan — requiring a qualifying credit score of 580 or above for the lower down payment option (HUD) — to purchase a first home within months of arriving.

Expert Recommendation

Top Pick: FHA Loan

For most newcomers purchasing their first U.S. home, an FHA loan remains the strongest starting point. The program accepts a down payment as low as 3.5% and is accessible to borrowers with a credit score of 580 or above — a threshold many immigrants can reach within their first year or two of building U.S. credit history. Critically, FHA lenders may accept an ITIN in place of a Social Security Number and can consider non-traditional credit references such as utility and rental payment records, making it genuinely accessible before a deep U.S. credit file exists.

The trade-off is mortgage insurance that stays in place for the life of the loan on most FHA terms. Borrowers who anticipate building stronger credit and equity within a few years may eventually refinance into a conventional product — but for the entry point, FHA’s flexibility on credit and documentation typically outweighs the insurance cost.

Best for: Newcomers with limited U.S. credit history, ITIN borrowers, buyers with modest down payment savings.

Runner-Up: Fannie Mae HomeReady

Once a newcomer has established a Social Security Number and a somewhat thicker credit profile, Fannie Mae HomeReady offers a compelling upgrade. PMI under HomeReady is cancellable once sufficient equity is reached — an advantage over standard FHA terms. HomeReady also allows income from non-borrower household members to support qualification, which suits many multigenerational immigrant households. The eligibility bar is somewhat higher than FHA on documentation, but the long-term cost structure is often lower.

Best for: Newcomers with an SSN, moderate credit history, and household income from multiple earners.

Before You Apply: One Step Worth Taking

Regardless of which program fits your profile, consulting a HUD-approved housing counselor before submitting any application is strongly advisable. These counselors provide independent, lender-neutral guidance on program fit, affordability, and documentation — typically at little or no cost. For newcomers navigating an unfamiliar system, that independent review can prevent expensive missteps at the program-selection stage.

FAQ: First-Time Home Buyer Mortgage for Newcomers (USA)

Can I get a mortgage in the USA without a Social Security Number?

Yes. FHA loans accept borrowers who use an Individual Taxpayer Identification Number (ITIN) instead of an SSN. Some conventional lenders also offer ITIN-based mortgage products, though underwriting standards vary widely. Your ITIN establishes your tax identity with the IRS and serves as a credit-building anchor. Lenders will still evaluate income stability, employment history, and assets. If you have no U.S. credit history, some lenders accept international credit records through services such as NOVA Credit. Eligibility criteria differ by lender, so compare at least three offers before committing.

What credit score do I need to qualify for the lowest FHA down payment?

A minimum decision credit score of 580 qualifies you for FHA’s lowest down payment option. Scores below that threshold don’t automatically disqualify you, but you will face stricter underwriting conditions, including debt-to-income ratio caps applied under manual underwriting. Building your U.S. credit profile before applying — through secured cards, credit-builder loans, or authorized user status — can move your score above the 580 threshold and meaningfully improve your loan terms.

How much do I need to save for a down payment as a newcomer?

The amount depends on the loan program you qualify for. FHA allows a down payment as low as 3.5% of the purchase price for borrowers meeting the credit score requirement. Conventional programs such as Fannie Mae HomeReady and Freddie Mac Home Possible target low-to-moderate income buyers and may require a comparably modest down payment, though exact figures vary by lender and borrower profile. Beyond the down payment, budget for closing costs, which typically add several thousand dollars and vary by state, loan size, and lender fees.

Does my immigration status affect my mortgage eligibility?

Lenders may ask for documentation of lawful residency, but federal fair lending rules prohibit discrimination based on national origin. Permanent residents, refugees, and certain visa holders commonly qualify for FHA and conventional loans. Undocumented immigrants are generally limited to ITIN-based products offered by portfolio lenders. Your specific visa category, remaining authorized stay, and employment authorization status all influence how underwriters assess repayment likelihood and risk. Consulting a HUD-approved housing counselor can help you understand which programs align with your current immigration status.

What documents do newcomers typically need to apply for a mortgage?

Expect to provide government-issued photo ID, proof of lawful presence or visa status, tax returns or IRS transcripts for at least the past two years, recent pay stubs or self-employment income records, bank statements covering recent months, and documentation of any foreign assets. If you lack U.S. credit history, international credit reports or reference letters from foreign financial institutions may substitute, depending on the lender. Some lenders accept non-traditional credit references such as rent payment records and utility bills. Organizing these documents before approaching lenders significantly shortens the application timeline.

Are there down payment assistance programs available for immigrant first-time buyers?

Many state Housing Finance Agencies (HFAs) and nonprofit organizations offer down payment assistance grants or forgivable second loans specifically accessible to first-time buyers regardless of national origin, provided borrowers meet income and property limits. Program availability, benefit amounts, and residency requirements vary considerably by state. The CFPB’s homebuying resources and your state’s HFA website are reliable starting points for locating current programs. A HUD-approved counselor can also identify local assistance you may not find through general internet searches.

How does a HUD-approved housing counselor help newcomer buyers?

HUD-approved housing counselors provide independent, impartial guidance on budgeting, loan comparison, and homeownership readiness — often at little or no cost to the borrower. For newcomers specifically, counselors can explain U.S. mortgage terminology, review your Loan Estimate and Closing Disclosure line by line, and flag predatory terms before you sign. They are not affiliated with any lender, which protects you from conflicts of interest. Some agencies also offer services in multiple languages, making them particularly valuable for buyers still navigating English-language financial documents.

Can I use income earned abroad or remittances to qualify for a U.S. mortgage?

Foreign income may be considered by some lenders if it is documented, consistent, and likely to continue. Lenders typically require official tax records, employer letters, and bank statements showing regular deposits. Remittances received from abroad generally do not count as qualifying income because they don’t represent the borrower’s own earned income. Currency conversion, tax treaty implications, and wire transfer records can complicate underwriting. Working with a lender experienced in non-traditional income verification — and ideally one accredited through a recognized mortgage industry body — reduces the risk of late-stage application problems.

What is mortgage insurance and will I have to pay it as an FHA borrower?

FHA loans require both an upfront mortgage insurance premium paid at closing and an annual premium spread across monthly payments. This insurance protects the lender, not the borrower, against default. It remains in place for the life of the loan in most cases, unlike private mortgage insurance (PMI) on conventional loans, which can be cancelled once sufficient equity is reached. The cost increases your effective monthly payment and total loan cost, so factor it into your affordability calculations. Refinancing into a conventional loan once you have built adequate equity is a common strategy for eliminating ongoing insurance costs.

How long does the mortgage application process typically take for newcomers?

Timelines vary based on documentation complexity, lender workload, and whether additional verification of foreign income or credit is required. Standard purchases commonly close in roughly one to two months from application, but newcomer files with non-traditional credit or foreign income documentation can take longer. Delays most often arise from missing documents or lender requests for additional verification. Responding quickly to underwriter requests and having all documents pre-organized shortens the process considerably. Getting a pre-approval letter before house hunting also prevents surprises late in the transaction.

Conclusion

Buying your first home in the United States as an immigrant is genuinely achievable — but the path requires matching the right program to your specific credit profile, residency status, and documentation.

As earlier sections of this guide detail, FHA remains the most accessible entry point for many newcomers, accepting credit scores of 580 and above for a down payment as low as 3.5% (HUD). Conventional alternatives such as Fannie Mae HomeReady and Freddie Mac Home Possible extend options to borrowers with stronger credit histories who want cancellable PMI. For immigrants without a Social Security Number, ITIN-based lending and international credit-passport services like NOVA Credit widen access further.

Three practical steps to carry forward:

- Audit your credit file early. Both U.S. bureau history and any transferable foreign credit records affect your program eligibility.

- Compare Loan Estimates across at least three lenders. TILA and RESPA protections — explained in Section 3 — require lenders to deliver standardized disclosures, so direct cost comparisons are straightforward.

- Book a HUD-approved housing counselor. Independent counselors provide personalized guidance on your specific situation, typically at little or no cost (HUD counselor locator).

The regulatory framework in the United States explicitly prohibits discrimination based on national origin, meaning every lender you approach must evaluate you on financial merit alone. Use that protection, prepare your documentation thoroughly, and the path from newcomer to homeowner is shorter than most immigrants expect.

Disclaimer

For Informational Purposes Only. The content published on MoneyAbroadGuide.com, including this guide, is intended solely for general educational purposes. It does not constitute mortgage advice, legal advice, or financial planning services. Mortgage eligibility, program terms, interest rates, and regulatory requirements change frequently; always verify current details directly with lenders, the U.S. Department of Housing and Urban Development (HUD), the Consumer Financial Protection Bureau (CFPB), or a licensed mortgage professional before making any financial decision.

Affiliate Disclosure. MoneyAbroadGuide.com may receive compensation from lenders, mortgage brokers, or financial service providers referenced or linked within this article. This compensation may influence which products are featured but does not influence our editorial assessments. We are committed to editorial independence in compliance with applicable advertising disclosure standards.

No Guarantee of Outcomes. Individual results vary based on credit history, income, residency status, property location, and lender criteria. Neither MoneyAbroadGuide.com nor its contributors are licensed mortgage brokers, attorneys, or registered financial advisors in any U.S. jurisdiction. Consult a licensed professional for advice tailored to your circumstances.

About the Author

Talal Eddaouahiri is the founder of MoneyAbroadGuide.com, an independent financial information platform for immigrants and newcomers in the United States and Canada. Originally from Morocco, he settled in the U.S. in 2015 and built his own credit history and banking relationships from scratch in both countries. His background is in retail banking and customer relations, and he draws on that firsthand experience to write independent, source-based guides — citing regulators including the FCAC, FINTRAC, OSFI, CRA, IRS, and CDIC — to help newcomers navigate financial systems with confidence.

Learn more about our Fact-Checking Process and our How We Test when researching this guide.

Last Updated: July 2026

About Talal Eddaouahiri

Founder & Editor of MoneyAbroadGuide.com. A Moroccan immigrant who settled in the United States in 2015, Talal opened bank accounts and built credit from zero in both the US and Canada. His background is in retail banking and customer relations, and he writes independent, source-based guides (FCAC, FINTRAC, OSFI, CRA, IRS, CDIC) to help newcomers navigate their first financial steps. Read his full profile →