Best Credit Cards for New Immigrants No SSN: Complete Guide for USA Immigrants (2026)

Quick Answer

New immigrants can qualify for U.S. credit cards without a Social Security Number by using an ITIN (Individual Taxpayer Identification Number) or passport. Secured cards, credit-builder products, and ITIN-accepting issuers are the most accessible entry points. Building U.S. credit history early is essential for housing, employment, and financial stability.

Arriving in the United States without an established credit history is one of the most common financial barriers newcomers face. Whether you hold a visa, green card, work permit, or are on a path to permanent residency, the U.S. credit system treats you as a complete stranger — regardless of your financial track record abroad. A significant portion of U.S. adults remain credit invisible, and newly arrived immigrants are disproportionately represented in that group.

The challenge is compounded by a widespread assumption: that a Social Security Number (SSN) is required to apply for any credit product. That assumption is incorrect. The IRS issues ITINs specifically for individuals who are not eligible for an SSN but still need to interact with the U.S. tax and financial system — and a growing number of credit card issuers now accept ITINs as a valid form of identification during the application process.

Understanding how to navigate this landscape matters enormously. According to the Consumer Financial Protection Bureau (CFPB), credit cards — used responsibly — are among the most efficient tools for building a U.S. credit profile. Without one, immigrants often find themselves locked out of apartment rentals, auto financing, and competitive loan rates for years after arrival.

This guide cuts through the confusion. You’ll find a curated comparison of the best credit cards available to new immigrants without an SSN, eligibility requirements by visa and immigration status, step-by-step application strategies, and practical advice on avoiding costly missteps while your credit profile is still thin.

For a broader look at entry-level credit options across visa types, see our full resource: Best Credit Cards for Newcomers in USA 2026 | No SSN Needed.

Building credit as an immigrant is a process — but it starts with the right card, the right application approach, and accurate information. This guide provides all three.

1. Best Credit Cards for New Immigrants No SSN in 2026: Quick Overview

Securing a credit card without a Social Security Number remains one of the most common financial hurdles newcomers face in the United States. The good news: a growing number of issuers now accept passport numbers, visa documentation, or an ITIN at the application stage — and several evaluate applicants using alternative data entirely, bypassing traditional credit bureau files.

Who This Guide Is For

This overview targets immigrants, visa holders, international students, and foreign nationals who are legally present in the U.S. but lack an SSN. That includes H-1B, F-1, J-1, O-1, TN, and green card holders, as well as DACA recipients and those in the ITIN-filing pathway.

The Core Challenge: Being “Credit Invisible”

According to the CFPB, a significant share of U.S. adults are credit invisible — meaning they have no credit file at any of the three nationwide bureaus. Newcomers are disproportionately represented in this group, regardless of their financial sophistication or overseas credit history. U.S. credit bureaus do not import foreign credit records, so even a decade of responsible credit behavior abroad counts for nothing when a lender pulls a domestic file.

How Cards in This Guide Were Selected

The cards featured throughout this article were evaluated against five criteria drawn from published issuer terms and regulatory guidance:

- No SSN required at application — accepts passport, visa, or ITIN

- No or low credit history requirement — explicitly markets to thin-file or no-file applicants

- Transparent fee structure — annual fees, foreign transaction fees, and security deposit terms are clearly disclosed

- Reported to all three major bureaus — critical for building a U.S. credit file efficiently

- Regulatory standing — issued by FDIC-insured banks or NCUA-insured credit unions operating under federal consumer protection frameworks, including CFPB oversight

What to Expect From Each Card

For a newcomer without any U.S. credit history, the realistic starting options fall into three categories: secured cards, unsecured starter cards (higher APRs, modest credit limits), and ITIN-accepted cards from community banks or credit unions. A concrete example: a newcomer on an H-1B visa who arrived six months ago, holds an ITIN, and deposits as collateral could qualify for a secured card, begin reporting payment history immediately, and —based on CFPB guidance —start building a score where paying on time every time has the greatest single impact on that score.

Keeping utilization at or below 30% of the card’s limit, as CFPB advises, accelerates score growth. The detailed card-by-card breakdown, fees, deposit requirements, and application steps follow in the sections below.

2. What Is a “No-SSN Credit Card” and Why Do Immigrants Need It?

Defining the Product Category

A no-SSN credit card is any credit card that an issuer will underwrite using an alternative identifier — most commonly an Individual Taxpayer Identification Number (ITIN) — or through a passport and visa verification process, rather than requiring a Social Security Number at application. The category spans secured cards, student cards, and a handful of unsecured products from credit unions and fintech issuers.

The need exists because the conventional U.S. credit system creates a compounding barrier: you cannot build a credit file without a credit account, and most credit accounts historically required an SSN. According to the CFPB, a significant share of U.S. adults are “credit invisible,” meaning they have no scoreable credit history — and newly arrived immigrants represent a disproportionate segment of that group. Without a scoreable file, even immigrants who managed credit responsibly in their home country start from zero.

How Alternative Identifiers Change the Equation

When a lender accepts an ITIN instead of an SSN, it uses the same downstream credit bureau infrastructure — Equifax, Experian, TransUnion — to report your payment behavior. That reporting is what generates a credit file. According to the IRS, an ITIN is issued for federal tax purposes and does not authorize work or confer immigration status, yet many card issuers treat it as a functionally equivalent identifier for account opening.

For example, a newcomer who arrives on an F-1 student visa or a work visa with an ITIN can apply for a secured card from an ITIN-accepting issuer, deposit a security amount, and begin generating on-time payment history immediately. According to the CFPB, paying bills on time, every time has the greatest impact on a credit score — meaning every monthly statement paid in full during those early months carries maximum scoring weight.

Five Structural Reasons Immigrants Specifically Need This Product

- Rental applications — Most U.S. landlords run credit checks. A thin or absent file means higher deposits or outright denial.

- Utility accounts — Providers often check credit before waiving a security deposit.

- Auto financing — Lenders price loans using credit scores; no score typically means subprime rates or cash-only terms.

- Employment screening — Certain licensed industries conduct credit checks as part of background verification.

- Credit score composition — According to USA.gov, five factors shape a credit score: payment history, outstanding balances, length of credit history, new credit applications, and types of credit accounts. Length of history rewards those who open an account early; every month without an account is permanent lost time in that factor.

A hard inquiry from applying will temporarily affect your score — according to the CFPB, scoring models consider both recency and frequency of applications — so applying strategically to one well-matched card is more efficient than multiple simultaneous applications.

The cards covered in Section 1 directly address this sequence: they accept non-SSN identifiers, report to all three major bureaus, and are structured specifically for people entering the U.S. credit system without an existing domestic history.

3. Eligibility Requirements for Immigrants

Qualifying for a no-SSN credit card involves more moving parts than a standard application. Issuers evaluate immigration status, identification documents, and income sources through criteria that differ meaningfully from those applied to U.S. citizens.

Immigration Status and Visa Type

Most issuers accepting alternative identifiers — including the ITIN pathway covered in Section 2 — segment applicants by immigration category:

- Permanent residents (Green Card holders): Broadest access. Most secured and unsecured products are available; some issuers accept a Permanent Resident Card as standalone ID.

- Nonimmigrant visa holders (F-1, H-1B, L-1, O-1, TN): Eligible at most major issuers, though some require proof of visa validity extending beyond the application date.

- DACA recipients: Eligible for ITIN-based products where DACA status does not disqualify; access varies significantly by issuer.

- Asylum seekers and refugees: Eligible with an Employment Authorization Document (EAD) as a primary identifier; USCIS Form I-94 arrival records are commonly accepted as supplementary documentation.

- Undocumented immigrants with ITIN: Eligible specifically for ITIN-based products; issuer selection is narrower but genuine options exist (see Section 1 overview).

Acceptable Identification Documents

Beyond immigration status, issuers typically require at least two forms of identification. Commonly accepted combinations include:

| Document | Accepted by Most Issuers |

|---|---|

| ITIN + Foreign passport | Yes |

| ITIN + Consular ID (Matrícula Consular) | Select issuers |

| EAD + Foreign passport | Yes |

| Permanent Resident Card | Yes (standalone at some) |

| Foreign national ID + ITIN | Issuer-dependent |

A home-country driver’s license is generally not accepted as a primary ID, though it may satisfy secondary verification requirements.

Income and Financial Requirements

Issuers must verify an independent ability to repay — a requirement the CFPB reinforces in its credit card rules. For immigrants, acceptable income documentation typically includes:

- U.S.-based employer pay stubs or offer letters

- Bank statements showing regular deposits

- Remittances or overseas income (accepted by select issuers with documentation)

- Scholarship stipends for F-1 students

According to the CFPB, applicants under 21 must additionally demonstrate an independent ability to pay or secure a co-signer over 21 — a threshold that affects younger international students on F-1 visas who lack a U.S. income history.

For example, a newcomer on an H-1B with three months of U.S. pay stubs but no credit history would typically qualify for the secured products listed in Section 1, which weigh income evidence more heavily than credit file depth.

Credit History Considerations

Issuers cannot access foreign credit bureau data. Immigrants therefore start as “credit invisible” — a population the CFPB has documented as a structural barrier to mainstream financial access. Some issuers (notably Nova Credit partners) use credit passport programs to translate foreign bureau data into a U.S.-equivalent report, partially bridging this gap for applicants from supported countries including India, Mexico, the UK, Canada, and Australia.

Age Requirement

All applicants —regardless of immigration status —must be old under the Credit CARD Act. As noted above, the under-21 co-signer rule applies universally and is enforced by issuers irrespective of visa category.

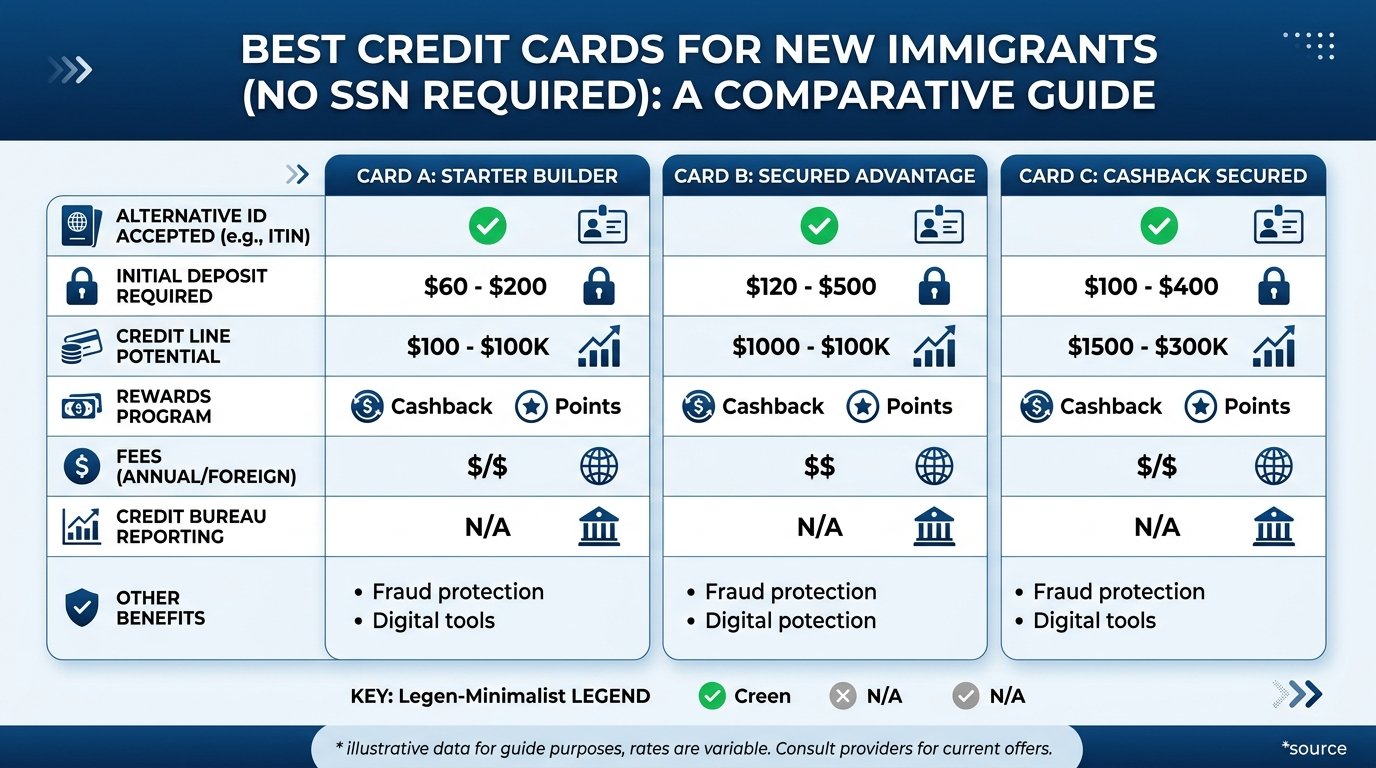

4. Side-by-Side Comparison: Best Credit Cards for New Immigrants (No SSN Required)

Choosing the right card depends on your immigration status, available identification, and how quickly you need to start building a U.S. credit file. The table below compares leading options across the dimensions that matter most to newcomers — accepted ID, deposit requirements, reporting behavior, and key costs. Note that terms change frequently; confirm current offers directly with each issuer before applying.

Your five credit score factors — payment history, balances, credit history length, new applications, and account mix — are all influenced by which card type you hold and how you use it (USA.gov). Keeping utilization well below the commonly cited threshold and paying on time each cycle (CFPB) will determine how fast your file matures, regardless of which card you choose. Each hard application inquiry can affect your score, with frequency and recency both considered (CFPB), so apply selectively.

| Card / Product | SSN Required? | Accepted Alternative ID | Security Deposit | varies by provider — confirm directly | Annual Fee | Best For |

|---|---|---|---|---|---|---|

| Deserve EDU Mastercard | No | Passport + visa; uses Nova Credit for foreign bureau data | None (unsecured) | Yes | None | International students on F-1/J-1 |

| Bank of America Customized Cash Secured | No (ITIN accepted) | ITIN + government-issued ID | Typically required; amount varies | Yes | None | Permanent residents, EAD holders building history |

| OpenSky Secured Visa | No | Government-issued photo ID; no credit check | Required; amount varies by applicant | Yes | Low annual fee (varies) | Undocumented immigrants, DACA recipients, thin-file applicants |

| FNBO Secured Visa | No (ITIN accepted) | ITIN + ID | Required | Yes | Varies | ITIN-only applicants seeking a traditional bank product |

| Self Visa Credit Card (credit-builder path) | No (ITIN accepted) | ITIN accepted | Funded via linked credit-builder account | Yes | Low annual fee (varies) | Applicants with no credit history; research suggests credit-builder products can establish scores (CFPB) |

| Petal 1 “No Annual Fee” Visa | No (ITIN accepted) | ITIN; uses cash-flow underwriting | None (unsecured for qualifying applicants) | Yes | None | Immigrants with verifiable income but no U.S. credit file |

| American Express (via Nova Credit) | No | Foreign credit passport from eligible countries | None (unsecured) | Yes | Varies by card | Newcomers from Nova Credit partner nations with established home-country credit |

Deposit note: Deposit amounts vary by issuer, applicant profile, and state — confirm directly. Negative marks on any card you open can remain on your report for typically up to seven years (CFPB), making responsible use from day one essential.

Illustrative Scenarios

The following are illustrative scenarios, not real testimonials or case studies of specific individuals.

Illustrative Scenario: Skilled Worker Visa Holder, Healthcare Support Role (Illinois)

A visa holder with valid work authorization but no SSN applies for a secured card using an ITIN, deposits a qualifying amount, and begins establishing a U.S. credit file from month one of employment.

Expert Recommendation

Choosing the right first credit card without an SSN is a high-stakes decision — a misstep can delay credit-building progress by months, while the right pick accelerates it. Based on regulatory compliance, accessibility for non-SSN applicants, and practical value for immigrants in their first year, here are our top two choices.

🥇 Top Pick: OpenSky® Secured Visa® Credit Card

OpenSky is the strongest option for most newcomers because it requires no SSN and no credit history, and — critically — it does not run a hard inquiry during the application process. This matters because scoring models weigh both the recency and frequency of credit applications, meaning every unnecessary hard pull chips away at a score you are still building from zero.

The card reports to all three major U.S. credit bureaus monthly. Since paying bills consistently on time carries the greatest weight in determining your credit score, a secured card that reports reliably gives you a direct mechanism to demonstrate exactly that behaviour.

OpenSky accepts an ITIN in place of an SSN, which makes it suitable for a broad range of visa holders and undocumented immigrants who have obtained tax identification through the IRS. Annual fee applies, but no bank account is required — a meaningful accessibility advantage for newly arrived immigrants who may not yet have a U.S. banking relationship.

Best for: Visa holders, ITIN holders, and newcomers with no prior U.S. credit footprint who need a guaranteed approval path.

🥈 Runner-Up: Deserve® EDU Mastercard (or Deserve Pro)

Deserve uses alternative underwriting — including cash flow analysis and educational background — rather than relying solely on a U.S. credit file. It accepts passport and visa documentation in lieu of an SSN and has partnered with Nova Credit to recognise international credit histories from select countries, giving immigrants with established foreign credit profiles a meaningful advantage.

Keeping credit utilisation comfortably below the commonly recommended threshold of 30% is straightforward with Deserve’s transparent credit limit structure, which helps newcomers practise responsible usage from day one.

Best for: International students, skilled-worker visa holders, and immigrants whose home country is supported by Nova Credit’s international bureau network.

Which Should You Choose?

If approval certainty is your priority — and you have an ITIN — go with OpenSky. If you have verifiable income or an international credit history and want an unsecured product, Deserve is the stronger long-term play.

📌 Planning to move between the U.S. and Canada, or comparing options across borders? Our Best Credit Cards for Newcomers in Canada (2026 Complete Guide) covers the parallel landscape for Canadian arrivals, including products that accept equivalent alternative identification — useful if your immigration journey spans both countries.

Frequently Asked Questions: Best Credit Cards for New Immigrants No SSN (USA)

Can I apply for a U.S. credit card without a Social Security Number?

Yes. Several issuers — including Bank of America, Citi, and credit unions — accept an ITIN or passport in place of an SSN. Nova Credit also allows some newcomers to port foreign credit history, bypassing the SSN requirement entirely. Eligibility varies by issuer and immigration status, so contact the bank directly before applying. Keep in mind that each application triggers a hard inquiry, and scoring models weigh how recently and frequently you apply, so space out applications strategically.

What documents do I typically need instead of an SSN?

Most issuers accepting non-SSN applicants will ask for a government-issued photo ID (passport, consular ID), proof of U.S. address, and either an ITIN issued by the IRS or a foreign tax identification number. Some institutions also request an Employment Authorization Document or Permanent Resident Card. Requirements vary by lender, so confirm the exact document list with your target issuer before submitting — applying with incomplete documentation can result in a denial that still generates a hard inquiry on your file.

Does applying for a credit card hurt my credit score if I have no U.S. credit history yet?

A hard inquiry does affect your score as soon as it appears; lenders consider both the timing and frequency of credit applications. If you are newly arrived with no U.S. credit file, the immediate damage is minimal simply because there is little score to lose — but building a thin file carefully matters more than any short-term dip. Apply selectively, prioritize issuers known to accept your documentation, and avoid submitting multiple applications within a short window.

What is the fastest way to build U.S. credit after I get my first card?

Consistent, on-time payment is the single most influential habit you can develop: paying every bill on time carries the greatest weight in how your credit score is calculated. Beyond that, keep balances well below your limit — financial experts generally recommend staying under 30% utilization. Supplement your secured or no-SSN card with a credit-builder loan; CFPB research indicates these products can meaningfully accelerate score growth, particularly for people starting without existing debt.

How long do mistakes — like a missed payment — stay on my U.S. credit report?

Most negative entries, including late payments and collections, remain visible for seven years from the date of first delinquency. A bankruptcy is more damaging: it can appear on your report for up to a decade. For newcomers building a file from scratch, this underscores why starting cautiously with a secured card or low-limit product — and never missing a payment — is far better than overextending early and carrying a derogatory mark for years.

What factors actually determine my U.S. credit score?

According to the U.S. government, five elements derived from your credit report shape your score: payment history, amounts owed, length of credit history, new credit applications, and the mix of account types. No single factor is officially weighted with a published percentage in government guidance. For immigrants, length of history and account mix are typically weak at first — which is why on-time payments and responsible utilization on even one account can move the needle noticeably within the first several months.

Can I check my U.S. credit report for free once I have a file established?

Yes. Once a U.S. credit file exists in your name, you can access a free report from each of the three nationwide bureaus — Equifax, Experian, and TransUnion — every week through AnnualCreditReport.com, a program now made permanent. Reviewing all three reports is worthwhile because information does not always appear identically across bureaus. Monitoring regularly helps you catch errors early and understand how your file is growing — critical for newcomers who may have thin files susceptible to reporting mistakes.

What should I do if I find an error on my U.S. credit report?

File a dispute directly with the bureau reporting the inaccurate information. Under federal law, the bureau must complete its investigation within 30 days of receiving your dispute, though this window can extend to 45 days under specific circumstances. Submit your dispute in writing with supporting documentation — a copy of your ID, the report showing the error, and any evidence contradicting the entry. Errors are especially common for credit-invisible newcomers whose files may contain mixed or misattributed data from similarly named individuals.

Are there age restrictions I should know about when applying for a credit card as an immigrant?

Yes. If you are under 21, U.S. law requires you to demonstrate an independent ability to repay the debt or have a co-signer aged 21 or older. This rule — established under federal credit card legislation — applies regardless of immigration status. If you are a younger newcomer without a co-signer, a secured card funded with your own deposit is often the most accessible path, since the deposit functions as collateral and issuers face less underwriting risk.

If I have no U.S. credit history at all, am I completely out of options?

Not at all. A meaningful segment of U.S. adults remains credit invisible — meaning credit bureaus hold little or no file on them — and financial products exist specifically for this population. Secured credit cards, ITIN-based accounts, and credit unions serving immigrant communities are practical starting points. Your credit score reflects five distinct factors, so opening even one responsibly managed account begins populating your file across multiple dimensions simultaneously — accelerating your path to mainstream credit access faster than most newcomers expect.

Conclusion

Building credit in the United States without a Social Security Number is genuinely achievable — but it requires choosing the right starting point. Throughout this guide, you have seen that secured cards, ITIN-accepting products, and alternative-data underwriting tools exist specifically to serve immigrants and newcomers navigating an unfamiliar financial system.

Your immediate priority should be selecting a card that accepts your current identification — whether that is an ITIN, passport, or visa documentation — and using it consistently. Remember that paying every bill on time carries the greatest weight on your credit score, according to the CFPB, and that five distinct factors — including payment history, outstanding balances, and length of credit history — collectively shape where your score lands under U.S. federal guidance. Keeping utilization well below the commonly recommended ceiling and avoiding unnecessary hard inquiries will also protect early progress.

Many immigrants start with no U.S. credit file at all — a situation that affects a meaningful share of U.S. adults who remain credit invisible through no fault of their own. The cards and strategies in this guide exist to close that gap.

Monitor your file weekly using the free reports available at AnnualCreditReport.com from each of the three nationwide bureaus. If errors appear, bureaus are legally required to complete investigations within 30 days in most cases — up to 45 in limited circumstances.

Stay consistent, keep balances low, and revisit unsecured card options as your history grows.

Disclaimer

For Informational Purposes Only. The content published on MoneyAbroadGuide.com is intended solely as general financial education for immigrants, newcomers, and expats in the United States. Nothing in this article constitutes personalized financial, legal, immigration, or tax advice. Readers should consult a licensed financial advisor, qualified immigration attorney, or certified public accountant before making decisions that affect their credit, immigration status, or tax situation.

Accuracy and Currency. Credit card terms, eligibility criteria, fees, and issuer policies change frequently. While we strive to maintain accuracy, we cannot guarantee that every detail reflects current issuer offerings. Always verify terms directly with the card issuer before applying.

Affiliate Disclosure. MoneyAbroadGuide.com may receive compensation when readers click links to partner products or apply for financial products featured in this guide. This compensation may influence which products are highlighted or their placement order, but does not affect our editorial assessments or recommendations. We only feature products we believe offer genuine value to our immigrant audience.

Regulatory Context. Credit reporting rights referenced in this guide are governed by the Fair Credit Reporting Act (FCRA) and enforced by the Consumer Financial Protection Bureau (CFPB) and the Federal Trade Commission (FTC). Readers are encouraged to consult those official sources directly for authoritative guidance.

About the Author

Talal Eddaouahiri is the founder of MoneyAbroadGuide.com, an independent financial information platform for immigrants and newcomers in the United States and Canada. Originally from Morocco, he settled in the U.S. in 2015 and built his own credit history and banking relationships from scratch in both countries. His background is in retail banking and customer relations, and he draws on that firsthand experience to write independent, source-based guides — citing regulators including the FCAC, FINTRAC, OSFI, CRA, IRS, and CDIC — to help newcomers navigate financial systems with confidence.

Learn more about our Fact-Checking Process and our How We Test when researching this guide.

Last Updated: July 2026

About Talal Eddaouahiri

Founder & Editor of MoneyAbroadGuide.com. A Moroccan immigrant who settled in the United States in 2015, Talal opened bank accounts and built credit from zero in both the US and Canada. His background is in retail banking and customer relations, and he writes independent, source-based guides (FCAC, FINTRAC, OSFI, CRA, IRS, CDIC) to help newcomers navigate their first financial steps. Read his full profile →