Best Car Insurance for Foreign Drivers and International Students: Complete Guide for USA Immigrants (2026)

Quick Answer: Foreign drivers and international students in the USA must carry state-mandated minimum liability insurance before operating any vehicle. Coverage options, license requirements, and costs vary significantly by state — but specialized insurers now accept foreign driving histories, foreign licenses, and even ITINs, making coverage more accessible than ever.

Navigating American car insurance as a newcomer is genuinely complex. Unlike many countries with centralized systems, auto insurance in the USA is regulated at the state level — meaning requirements in Texas differ materially from those in New York, California, or Florida. For immigrants, visa holders, and international students on F-1 or M-1 status, this fragmentation creates a layered challenge: you must simultaneously satisfy your state’s legal minimums, secure coverage without a US credit history, and in some cases obtain a valid state driver’s license before a policy will be issued.

The stakes are high. Driving uninsured is illegal in virtually every state, and a single at-fault accident without adequate coverage can trigger financial liability that exceeds tens of thousands of dollars. According to USA.gov’s motor vehicle services guidance, all drivers must comply with their state’s insurance laws — no exemptions exist for foreign nationals or visa holders.

For international students specifically, licensing eligibility adds another layer. F and M visa holders may drive on a foreign license initially, but obtaining a state-issued license is ultimately required — driving without one is illegal, and not all states recognize foreign licenses, as noted by USA.gov’s non-citizen driving resource.

This guide cuts through the complexity. We cover state-by-state minimum requirements, how to get insured without a US driving record, what documentation insurers require from immigrants and students, and which providers offer the most competitive terms for non-citizens. Whether you arrived last week or last year, you’ll find actionable, regulation-grounded guidance here.

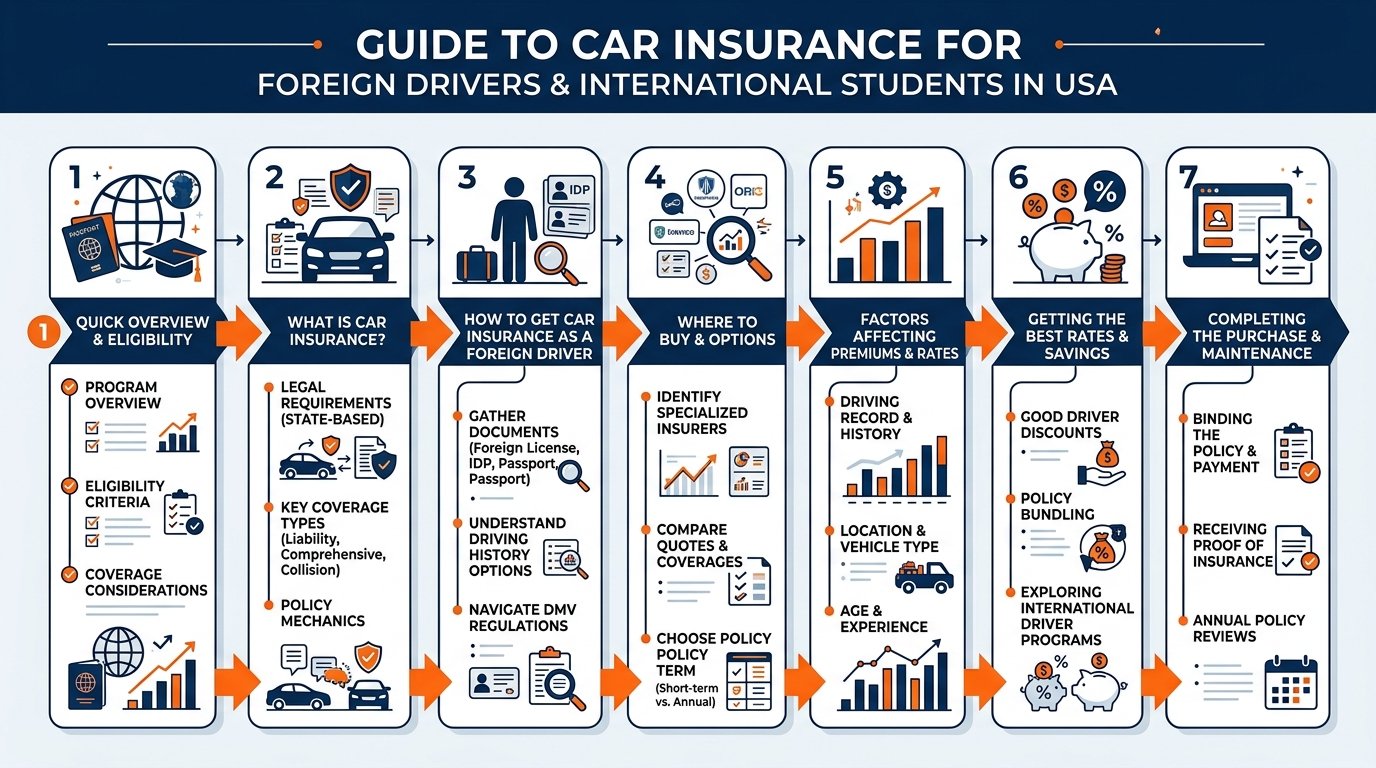

1. Best Car Insurance For Foreign Drivers And International Students for USA Immigrants in 2026: Quick Overview

Securing car insurance as a foreign driver or international student in the United States involves navigating state-specific minimum coverage mandates, licensing eligibility rules, and insurer underwriting criteria that often disadvantage applicants without a U.S. credit history or domestic driving record. Understanding the baseline requirements across key states is the fastest path to avoiding coverage gaps or legal penalties.

State Minimum Coverage at a Glance

Coverage floors vary significantly by state. According to the Texas Department of Insurance, Texas requires minimum liability of $30,000 bodily injury per person, $60,000 per accident, and $25,000 property damage (30/60/25). New York’s minimums — $25,000 per person, $50,000 per accident, and $10,000 property damage, with mandatory no-fault PIP — are detailed by the New York Department of Financial Services. Florida operates as a no-fault state requiring $10,000 PIP plus $10,000 property damage liability, with PIP covering 80% of medical expenses up to the policy limit, per the Florida FLHSMV. California’s minimums have shifted in recent years; current thresholds are published at the California Department of Insurance and should be confirmed before purchasing a policy.

For most foreign drivers, purchasing above minimum limits is advisable. A newcomer arriving with an international license and no U.S. claims history is typically rated as a higher-risk driver, meaning minimum-only coverage leaves significant personal liability exposure in at-fault states like Texas or California.

Licensing Eligibility for F and M Visa Holders

Before shopping for insurance, F and M visa holders must confirm they can legally obtain a state license. According to Study in the States (DHS), students must wait until their I-94 has been updated and their SEVIS record shows Active status — typically requiring at least two government business days after SEVIS activation — before applying at a state DMV. Applying prematurely risks rejection and delays the insurance application.

As noted by USA.gov, driving on a foreign license is not universally permitted, and operating a vehicle without a valid state license where one is required is illegal. Insurers also require a valid license to issue a policy, so this sequencing — SEVIS active, then DMV, then insurer — is non-negotiable.

What This Guide Covers

The sections that follow compare specific insurers willing to underwrite foreign-licensed drivers, evaluate which companies accept international driving records in lieu of a U.S. history, break down non-owner policies for students who rent or borrow vehicles, and outline documentation requirements by visa category. Each insurer comparison is grounded in published underwriting criteria and publicly available rate data, not promotional materials.

2. What Is Car Insurance For Foreign Drivers And International Students — And Why Do Immigrants Need It?

Car insurance in the United States functions as a legal contract between a driver and an insurer: the insurer absorbs defined financial losses in exchange for premiums. Every state except New Hampshire mandates minimum liability coverage before a vehicle can be legally operated on public roads. For foreign nationals — whether on an F-1 student visa, J-1 exchange visa, work visa, or a green card — this obligation applies immediately upon driving, regardless of immigration status.

Why the Standard Market Creates Barriers

U.S. insurers price risk using actuarial data that includes domestic credit history, a U.S. driving record, and often a Social Security Number (SSN). Newcomers possess none of these. According to the Consumer Financial Protection Bureau (CFPB), credit-based insurance scoring is legal in most states and directly affects premium calculation — meaning a recent arrival is statistically invisible to standard underwriting models. The practical result: many major carriers either decline coverage outright or quote rates two to four times higher than for comparable domestic drivers.

The License-First Requirement

Before any insurer will bind a policy, a driver must hold a valid license. According to Study in the States (DHS), F and M visa holders must allow their SEVIS record to reach Active status before applying at the DMV — a process that requires a minimum waiting period after U.S. arrival. Some states accept a foreign license temporarily; according to USA.gov, not all states do, and driving without a valid in-state license is illegal regardless of what a home-country license permits.

What Coverage Actually Does for an Immigrant Driver

Liability coverage — the universal minimum — pays third-party bodily injury and property damage claims when the insured driver is at fault. Without it, the at-fault driver is personally liable for all damages, a financial exposure that can reach six figures in a serious collision. For international students on an F-1 budget, or a newcomer without U.S. savings history, an uninsured accident can generate wage garnishment or civil judgment — legal consequences that may also complicate future immigration filings.

For example, a newcomer driving uninsured in a state like Texas — where minimum liability requirements are defined by state law and enforced by the Texas Department of Insurance — faces fines, license suspension, and potential vehicle impoundment on top of civil liability.

The Regulatory Framework Immigrants Must Navigate

State insurance departments (California DOI, Texas DOI, New York DFS, Florida OIR) license and regulate all auto insurers operating within their jurisdiction. Insurers must file rates with these regulators and cannot arbitrarily refuse coverage based on national origin — though they can legitimately use license type, years of driving history, and credit score as rating factors. Understanding this distinction helps newcomers identify unfair treatment versus legally permissible underwriting.

The core takeaway: car insurance for foreign drivers is not optional, not one-size-fits-all, and not freely available through standard channels without deliberate navigation of underwriting barriers.

3. Eligibility Requirements for Immigrants

Qualifying for car insurance as a foreign driver involves satisfying both licensing and documentation thresholds that vary by visa category, state, and insurer. Meeting these requirements determines not just whether you can buy a policy, but which carriers will quote you competitively.

Visa Category and Licensing Authority

Your visa classification directly shapes what documentation your DMV and insurer will accept:

F-1 and M-1 students must fulfill the I-94/SEVIS sequencing before applying for a state license. According to Study in the States (DHS), applicants must wait at least 10 days after U.S. arrival and at least two government business days after SEVIS confirms Active status — whichever comes later. For example, a student who arrives September 1st but whose SEVIS record activates September 8th cannot apply until September 10th at the earliest, not September 11th as the arrival-clock alone might suggest.

Work visa holders (H-1B, L-1, O-1): Most states treat these applicants similarly to permanent residents. Insurers generally require a valid state license, passport, and visa stamp. Employment Authorization Documents (EADs) are accepted as secondary ID by most major carriers.

DACA recipients: Approximately 27 states plus Washington D.C. issue standard driver’s licenses to DACA holders. Insurance eligibility follows licensure — if the state issues a license, insurers operating in that state must provide coverage under standard market rules.

Undocumented immigrants: Eleven states — including California, Illinois, and New York — issue driver’s licenses regardless of immigration status. The California DMV issues AB 60 licenses, which are valid for driving purposes and accepted by California-licensed insurers.

Documentation Insurers Typically Require

| Document | F/M Visa Students | Work Visa Holders | DACA / AB 60 Holders |

|---|---|---|---|

| Valid state driver’s license | Required | Required | Required |

| Passport + visa stamp | Required | Required | Passport only |

| I-20 or DS-2019 | Required | Not needed | Not needed |

| SSN or ITIN | Helpful, not always mandatory | Usually required | ITIN accepted by many carriers |

| Prior insurance records | Foreign records accepted by some carriers | Same | Same |

A Social Security Number is not legally required to purchase insurance in any state, but carriers use it for credit-based insurance scoring. Immigrants without an SSN often receive higher initial premiums; providing an ITIN or requesting a non-credit underwriting path can partially offset this.

Foreign Driving History

No federal database connects international driving records to U.S. insurers. However, several carriers — including GEICO and Travelers — accept certified driving record translations from select countries (notably Canada, Germany, Japan, and the UK) to reduce the “no U.S. history” surcharge. According to USA.gov, foreign licenses do not substitute for a state license once a driver establishes residency, reinforcing the urgency of converting your license early.

State-Specific Eligibility Nuances

Each state insurance department enforces its own rules on non-citizen eligibility. The Texas DOI confirms insurers cannot deny coverage solely based on national origin. California’s Department of Insurance similarly prohibits nationality-based denials. These protections mean carriers must underwrite based on driving record, vehicle, and location — not immigration status.

Comparing Car Insurance Options for Foreign Drivers and International Students

Choosing the right policy depends on your visa status, how long you plan to drive in the U.S., and which state you’ll be licensed in. The table below maps the most relevant coverage options against the criteria that matter most to newcomers — from documentation flexibility to cost drivers — so you can identify which policy type fits your situation before you contact a provider.

State minimum requirements vary significantly: New York mandates both liability and no-fault PIP (NYDFS), while Florida requires PIP plus property damage liability (FLHSMV). Texas sets its own liability thresholds (TDI), and California’s minimums are subject to change — check current figures at the California DOI. F and M visa holders must also satisfy the DHS SEVIS licensing timeline before a state will issue a driver’s license — a prerequisite most standard insurers require before binding a policy.

| Factor | Standard Personal Auto Policy | Non-Owner / Named-Operator Policy | International Student Specialty Policy | Rental / Short-Term Coverage |

|---|---|---|---|---|

| Best suited for | Permanent residents, long-term visa holders with SSN | Foreign drivers without a registered vehicle | F-1/M-1 students, new arrivals building credit history | Visitors, short-stay foreign nationals |

| SSN requirement | Usually required; ITIN sometimes accepted | Varies by insurer; ITIN often accepted | Often waived or ITIN-eligible | Typically not required |

| Foreign license accepted | Rarely; most states require a U.S. license (usa.gov) | Rarely; state DL strongly preferred | Sometimes accepted during grace window | Generally accepted for short stays |

| Credit history impact on premium | High — thin or no U.S. credit raises rates significantly | Moderate — less tied to vehicle ownership profile | Lower — some specialty providers use home-country driving record | Minimal — flat-rate daily pricing |

| Minimum coverage available | State-mandated liability floors (varies by state) | Liability only; no comprehensive or collision | Liability + options for comprehensive/collision | Liability typically bundled; limits vary |

| Policy duration | varies by provider — confirm directly | varies by provider — confirm directly | varies by provider — confirm directly | Daily, weekly, or monthly |

| Documentation flexibility | Low — passport, visa, U.S. DL, SSN typically all required | Moderate | High — designed for newcomer documentation gaps | High — passport usually sufficient |

Illustrative Scenarios

The following are illustrative scenarios, not real testimonials or case studies of specific individuals.

Illustrative Scenario: International Student, Engineering Program (Texas)

An F-1 student arriving in Texas waits the required period after entry — allowing both the I-94 record and SEVIS status to update (DHS) — before visiting the DMV, then secures liability coverage meeting Texas minimums (TDI) prior to driving on campus.

Expert Recommendation

Top Pick: GEICO — Best Overall for Foreign Drivers and International Students

GEICO consistently ranks as the strongest starting point for newcomers, largely because it accepts foreign driving history during the quoting process and operates nationwide, eliminating the need to shop a different carrier each time you relocate between states. For F and M visa holders who have already cleared the DHS licensing timeline and hold a valid state driver’s license, GEICO’s online quote system accommodates applicants without a U.S. credit history or SSN in many states — a practical advantage that several regional carriers do not offer.

GEICO is regulated at the state level through each jurisdiction’s insurance commissioner, meaning your policy carries the same statutory consumer protections as any domestic driver’s coverage. Claims handling, rate disputes, and policy disclosures all fall under the oversight of regulators such as the California Department of Insurance, the Texas Department of Insurance, and equivalent bodies in other states.

Best suited for: F-1 and M-1 students, work visa holders (H-1B, L-1, O-1), and permanent residents who need broad multi-state portability and a carrier familiar with non-standard documentation.

Runner-Up: Progressive — Best for High-Risk Profiles and SR-22 Needs

Progressive is the recommended alternative for foreign drivers who face elevated premiums due to a limited U.S. driving record, a recent at-fault incident, or a gap in continuous coverage — situations common among recent immigrants. Progressive’s tiered underwriting accepts a wider risk spectrum than many carriers, and it is one of the more accessible national insurers for SR-22 filings, which certain states require following license or insurance violations.

Progressive is licensed and regulated in all 50 states, with rate filings reviewed by each state’s insurance regulator, providing the same statutory oversight as the top pick.

Best suited for: Drivers rebuilding a U.S. insurance history, those who held a foreign license for several years before arrival, and anyone requiring SR-22 documentation.

Key Decision Factor

The single most important variable is your state of residence, since mandatory minimum coverage thresholds, no-fault rules, and acceptable documentation differ materially by jurisdiction. Confirm your state’s current minimums with its insurance regulator before finalizing any quote.

Frequently Asked Questions

Can I get car insurance in the USA without a US driver’s license?

Yes, though your options are limited. Some insurers will bind a policy using a valid foreign license, an International Driving Permit (IDP), or a passport as interim identification. However, most standard carriers require a state-issued license before issuing a full policy. Surplus-lines and non-standard insurers often accommodate foreign-licensed drivers at higher premiums. Check with your state’s insurance regulator for licensed providers in your area. Driving without the coverage your state mandates is illegal regardless of license status.

Which states have the strictest minimum liability requirements for new drivers?

Requirements vary considerably by state. New York, for example, requires specific minimums including mandatory no-fault PIP coverage, while Texas sets its own distinct bodily-injury and property-damage thresholds. Florida operates under a no-fault framework requiring personal injury protection plus property damage liability. California’s minimums have been subject to legislative revision and should be confirmed directly. Always verify current requirements with the relevant state regulator before purchasing.

How soon after arriving in the USA can an international student apply for a driver’s license?

F and M visa holders must allow their I-94 record to update and their SEVIS status to reflect “Active” before visiting a DMV. DHS guidance specifies waiting until at least two government business days after SEVIS activation, in addition to a post-arrival waiting period. Applying too early typically results in rejection because state DMVs verify both records electronically. Plan ahead — processing times at busy DMV offices can add further delays.

Can international students drive on their home-country license while waiting for a US license?

Federal guidance permits non-citizens to drive on a foreign license in many states, but some states do not recognize them, and driving without a valid state license where required is illegal. An International Driving Permit alongside your foreign license improves recognition but does not override state law. Check your specific state DMV rules promptly after arrival. Insurers may also refuse to underwrite a policy — or charge significantly more — if you hold only a foreign-issued document.

Will my car insurance premium be higher as a foreign driver or international student?

Almost certainly, yes — at least initially. Insurers price risk using driving history, and a foreign record typically cannot be verified through US databases. Without a domestic history, underwriters treat you similarly to a brand-new driver. Premiums typically decrease once you accumulate US-based driving history and establish a local credit profile. Some carriers work with services that import foreign driving records, which can modestly reduce initial quotes.

Do I need a Social Security Number to buy car insurance in the USA?

No SSN is strictly required by law to purchase auto insurance. Many carriers accept an Individual Taxpayer Identification Number (ITIN), passport number, or visa documentation as alternative identifiers. However, insurers that use credit-based insurance scoring will be unable to factor in a credit history if no SSN or established US credit file exists, which can result in higher quoted premiums. Ask each insurer explicitly which identification documents they accept before starting an application.

What happens to my car insurance if my visa status changes?

Notify your insurer promptly of any status change. A lapse into unlawful presence can affect your eligibility, and some carriers include visa validity as a material fact on the application. If your visa is extended, renewed, or changed to a different category, update your policy documentation accordingly. Misrepresentation — even unintentional — can void a claim. DACA recipients and Employment Authorization Document (EAD) holders should confirm their specific eligibility with the insurer, as policies vary by carrier and state.

Is it possible to transfer my no-claims bonus from my home country?

A limited number of US insurers — particularly those with international partnerships — will consider a letter from your foreign insurer confirming your claims-free years. There is no universal system for transferring no-claims history across borders, so acceptance is entirely at the underwriter’s discretion. Providing an official letter on insurer letterhead, translated if necessary, gives you the strongest chance. Even when accepted, the discount offered is typically smaller than what a comparable US history would generate.

Are there car insurance options specifically designed for international students?

Some non-standard and specialty insurers have developed products targeting student visa holders, often bundled through university affiliation programs or international student services offices. These programs may offer shorter policy terms aligned with academic semesters and accept foreign licenses as interim documentation. Premiums remain higher than the standard market, but the underwriting criteria are more accessible. Your university’s international student office is a practical starting point for identifying vetted providers.

What documentation should I bring when applying for car insurance as a foreign driver?

Gather the following before contacting insurers: valid passport, current visa or I-94 print-out, any existing foreign driver’s license and IDP, SEVIS confirmation (for F/M students), ITIN or SSN if available, vehicle title or registration, and a letter of driving experience from a prior insurer if you have one. Some carriers also request proof of address (a utility bill or lease agreement). Having complete documentation at the outset prevents delays and reduces the risk of a policy being issued on incorrect details.

Comparison Table: Key Coverage Options for Foreign Drivers and International Students

| Feature | Non-Standard / Surplus-Lines Insurer | Standard Carrier (Major Insurer) | University-Affiliated Program |

|---|---|---|---|

| Accepts foreign license only | Often yes | Rarely | Sometimes |

| SSN required | Usually no | Often yes | Usually no |

| Foreign driving history considered | Sometimes (letter accepted) | Rarely | Sometimes |

| Premium level vs. standard market | Higher | Standard (if eligible) | Moderate–High |

| Short-term / semester policies | Sometimes | No | Often yes |

| State minimum coverage available | Yes | Yes | Yes |

| Credit check used for pricing | Sometimes | Usually yes | Rarely |

| DACA / EAD holders accepted | Varies by carrier and state | Varies | Varies |

Coverage availability and pricing vary by state and individual underwriter. Confirm current terms directly with each provider.

Expert Recommendation

Foreign drivers and international students should prioritize obtaining a state driver’s license at the earliest lawful opportunity — this single step unlocks significantly broader insurer choice and lower premiums. While waiting, use a non-standard or surplus-lines carrier that accepts foreign documentation rather than driving uninsured.

Request quotes from at least three providers, including any program offered through your university’s international student office. Always ask each insurer explicitly whether they accept your visa category, what identification they require, and whether they can factor in a foreign driving history letter. Confirm that your chosen coverage meets your state’s current mandatory minimums — requirements differ materially across states and are subject to legislative change. Review your policy whenever your visa status, address, or vehicle changes.

Conclusion

Securing car insurance as a foreign driver or international student in the United States requires navigating a layered system—one that combines state-level regulatory requirements, insurer-specific eligibility rules, and immigration documentation standards that most newcomers encounter for the first time.

The core takeaway: your visa category, licensing status, and state of residence collectively determine which insurers will quote you, what documentation you must present, and how much you can expect to pay. F and M visa holders should confirm their SEVIS record is active and allow sufficient time after US arrival before visiting a DMV, as DHS guidance makes clear. Work visa holders, DACA recipients, and permanent residents each face a distinct set of requirements outlined throughout this guide.

Coverage minimums vary meaningfully by state—from no-fault PIP structures to traditional liability frameworks—so comparing your home state’s floor against your actual risk exposure is essential before selecting a policy. Minimum coverage is rarely sufficient for urban drivers, newer vehicles, or anyone without a robust financial safety net.

Practically speaking, newcomers benefit most from:

- Gathering all immigration and identity documents before contacting insurers

- Requesting quotes from multiple carriers, including non-standard market providers experienced with foreign-licensed drivers

- Reviewing policy terms for any foreign-license exclusions or grace-period clauses

This guide will be updated as state regulations and carrier policies evolve in 2026. For personalised advice, consult a licensed independent insurance agent familiar with immigrant client profiles.

Disclaimer

For informational purposes only. The content on MoneyAbroadGuide.com, including this article, is intended to provide general financial and regulatory information for immigrants, international students, and foreign drivers in the United States. It does not constitute legal, insurance, or financial advice. Individual circumstances—including visa status, state of residence, and driving history—vary significantly. Always consult a licensed insurance professional or legal advisor before making coverage decisions.

Regulatory accuracy. We reference official government and regulatory sources including state departments of insurance, DHS Study in the States, and USA.gov. Regulations change; verify current requirements directly with your state’s department of insurance or motor vehicles.

Affiliate disclosure. This article may contain links to insurance providers or comparison platforms. MoneyAbroadGuide.com may receive compensation if you click through and purchase a product. This does not influence our editorial assessments. We do not accept payment for positive reviews or rankings. Our recommendations are based on independent research and publicly available regulatory data.

No guarantee of coverage. Inclusion of any insurer or product in this guide does not guarantee that you will qualify for coverage. Eligibility determinations rest solely with the insurer.

About the Author

Talal Eddaouahiri is the founder of MoneyAbroadGuide.com, an independent financial information platform for immigrants and newcomers in the United States and Canada. Originally from Morocco, he settled in the U.S. in 2015 and built his own credit history and banking relationships from scratch in both countries. His background is in retail banking and customer relations, and he draws on that firsthand experience to write independent, source-based guides — citing regulators including the FCAC, FINTRAC, OSFI, CRA, IRS, and CDIC — to help newcomers navigate financial systems with confidence.

Learn more about our Fact-Checking Process and our How We Test when researching this guide.

Last Updated: July 2026

About Talal Eddaouahiri

Founder & Editor of MoneyAbroadGuide.com. A Moroccan immigrant who settled in the United States in 2015, Talal opened bank accounts and built credit from zero in both the US and Canada. His background is in retail banking and customer relations, and he writes independent, source-based guides (FCAC, FINTRAC, OSFI, CRA, IRS, CDIC) to help newcomers navigate their first financial steps. Read his full profile →